Buying a second home is an exciting milestone, whether it’s a holiday retreat by the coast, a rental investment, or a countryside escape. However, protecting your additional property requires more than your standard home insurance policy. Understanding the basics of coverage for a second property will help you make informed decisions and avoid potential pitfalls.

Now let’s dive in and explore what you need to know before securing coverage for your new investment.

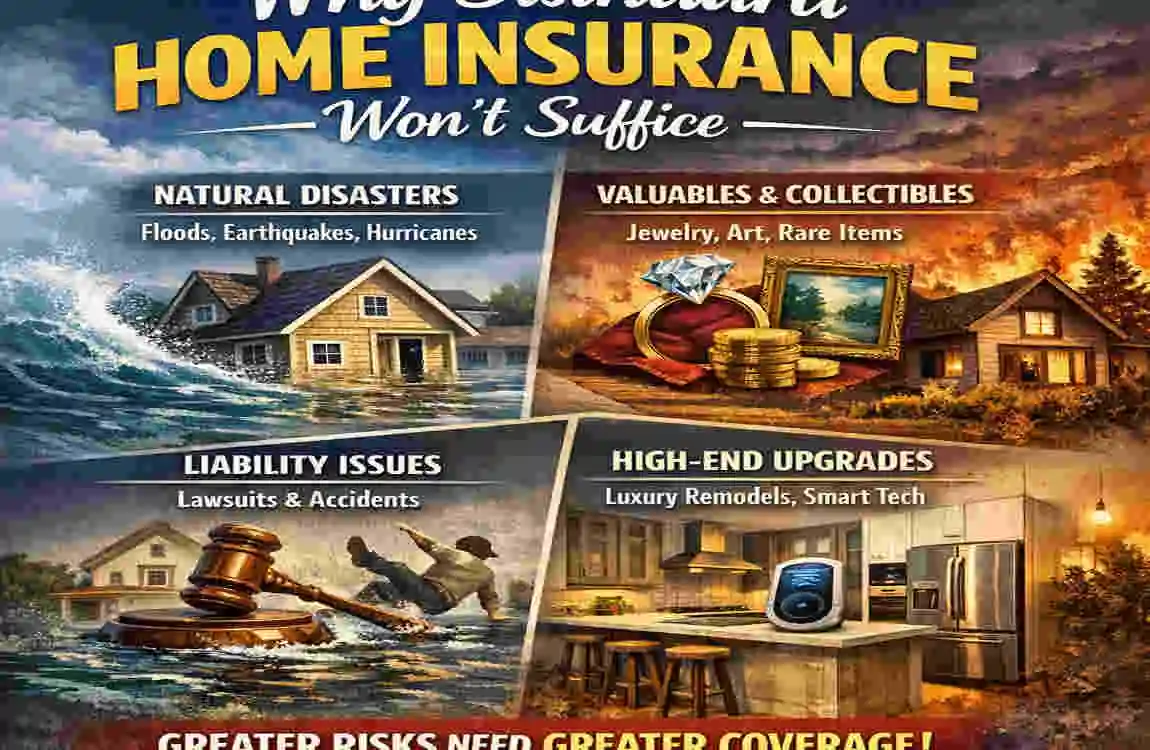

Why Standard Home Insurance Won’t Suffice

Many first-time buyers assume their existing home insurance can simply extend to cover another property. Unfortunately, that’s not how it works. Insurance providers treat second homes differently because they typically remain unoccupied for longer periods, which increases certain risks.

Empty properties face higher chances of vandalism, burst pipes going unnoticed, and damage from break-ins. Standard policies don’t account for these additional vulnerabilities. You’ll need a dedicated policy that addresses the unique challenges of owning a second property.

What Does Second Home Insurance Cover?

A comprehensive second home insurance policy typically includes buildings and contents cover, similar to your main residence. Buildings insurance protects the structure itself, the walls, roof, permanent fixtures, against damage from fire, flooding, storms, and other perils.

Contents insurance covers your belongings inside the property: furniture, electronics, clothing, and personal items. If you’re furnishing a holiday home or buy-to-let, this protection becomes particularly valuable.

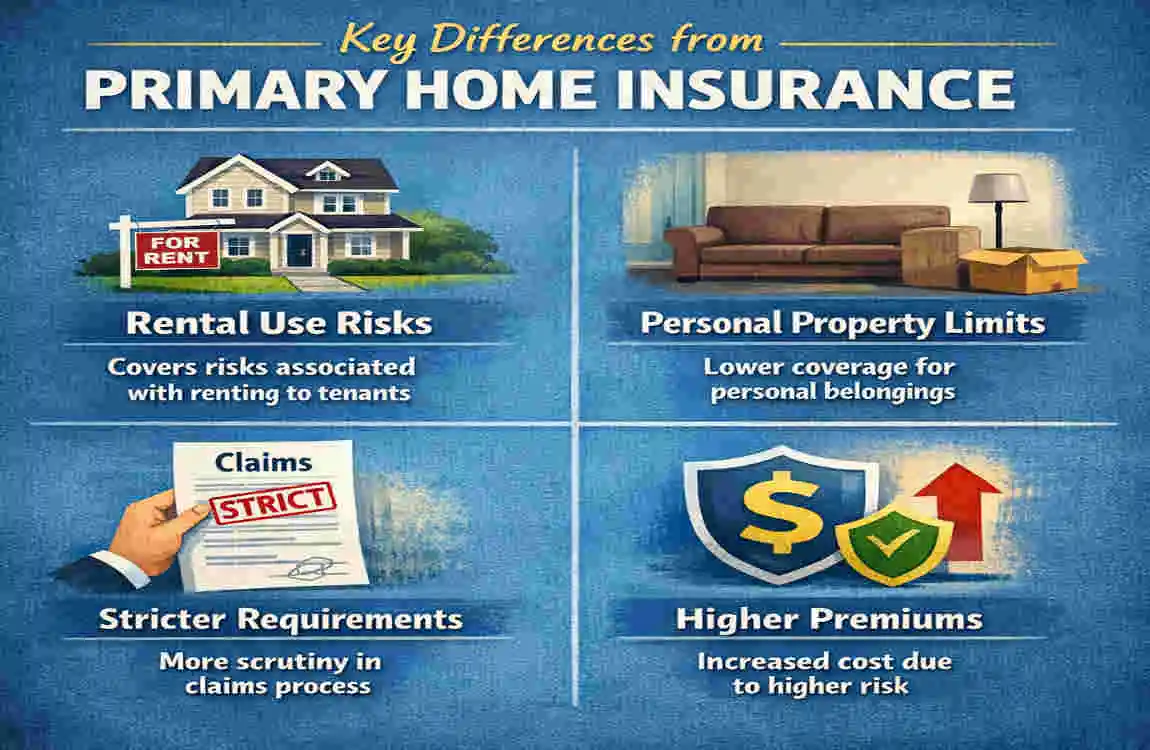

Key Differences from Primary Home Insurance

Occupancy requirements represent one of the biggest distinctions. Most insurers specify maximum periods your second home can remain empty, often around 30 to 60 consecutive days. Exceeding this limit without notifying your provider could invalidate your claim.

You’ll also find that premiums tend to be higher for second homes. Insurers calculate this increased cost based on the elevated risks associated with unoccupied properties. They may require additional security measures, such as approved locks, alarms, or regular property inspections.

What Affects Your Premium?

Several factors influence how much you’ll pay:

- Location – properties in flood-prone areas or high-crime locations cost more to insure

- Construction type – non-standard buildings or listed properties typically attract higher premiums

- Security measures – installing quality locks and alarm systems can reduce costs

- Occupancy patterns – how often you visit affects your risk profile

- Claims history – previous claims on any property can impact pricing

Being transparent about these factors when getting quotes ensures you’re properly covered.

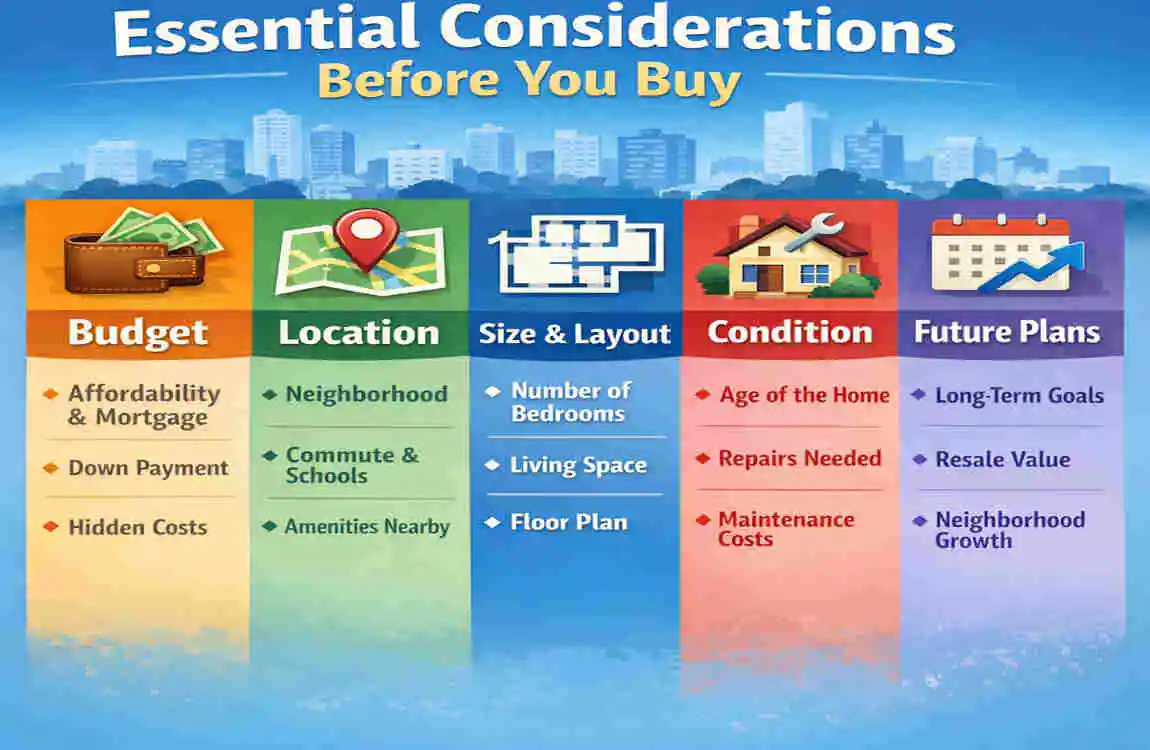

Essential Considerations Before You Buy

Will You Rent the Property?

Before purchasing a policy, clarify your intended use. Will you rent the property occasionally? This requires different coverage than a purely personal holiday home. Some policies exclude rental use entirely, whilst others accommodate it with adjusted terms.

Check Excess Amounts

Check the policy’s excess amounts carefully. Higher excesses reduce premiums but mean you’ll pay more when making a claim. You should also verify what’s excluded from coverage. Things like wear and tear, gradual damage, and certain weather events might not be covered.

Changing Circumstances

Don’t forget to inform your insurer if circumstances change. Converting your second home to a permanent rental, making significant renovations, or leaving it empty for extended periods all require notification.

Finding the Right Policy

Shopping around remains crucial. Different providers specialise in various property types and situations, so comparing quotes helps you find competitive rates without compromising on essential cover.

Consider working with a broker who understands the second home market. They’ll navigate policy nuances and find coverage that matches your specific needs, whether that’s a seaside cottage, a city flat, or a rural farmhouse.

Second Home Insurance Basics Explained for First-Time Buyers FAQ

What is second home insurance?

Second home insurance is a policy designed to protect a property that is not your main residence, such as a vacation home or investment property.

Why do I need insurance for a second home?

It protects against risks like fire, theft, storm damage, and liability issues, especially when the property is unoccupied for long periods.

Is second home insurance different from regular home insurance?

Yes. It usually costs more because second homes are considered higher risk due to less frequent occupancy.

What does second home insurance cover?

It typically covers the building structure, contents, accidental damage, weather damage, and public liability.

Do I need special coverage if I rent out my second home?

Yes. If you rent it out, you may need additional landlord or short-term rental insurance.

How much does second home insurance cost?

Costs vary based on location, property value, and usage, but it is generally higher than standard home insurance.

Can I reduce the cost of second home insurance?

Yes. Installing security systems, alarms, and maintaining regular inspections can help lower premiums.

Do insurers require home security for second homes?

Many insurers recommend or require security features like alarms, locks, and monitored systems.

What is the most important thing to know?

The key point is that second homes need specialized insurance due to higher risk and lower occupancy.

In Summary

Securing appropriate insurance for your second property is a crucial step in protecting a significant financial investment. With the right policy in place, you can enjoy your additional property with confidence, knowing you’re covered against the unexpected.

Take time to understand your options, ask questions, and choose coverage that genuinely reflects how you’ll use your second home. Your future self will thank you for getting it right from the start.