Many homeowners worry that filing bankruptcy means losing their home right away. That fear is very common, and it makes sense. Your house is often your biggest asset, and the thought of losing it can feel overwhelming.

The good news is that bankruptcy does not always mean you will lose your home. The answer to “can I keep my house if I file bankruptcy?” depends on a few important factors. These include the type of bankruptcy you file and how much equity you have in the home,

In simple terms, some people can keep their house, while others may not. The outcome depends on your specific situation. If you understand the rules early, you can make smarter choices and better protect yourself.

What Happens to Your House When You File Bankruptcy?

How Bankruptcy Affects Homeownership

Bankruptcy is a legal process that helps people deal with debt. When you file, the court looks at your debts, income, assets, and payment history. Your house becomes part of that review.

That does not mean the house is automatically taken. It only means the court and the trustee will assess whether the home has value that can be used to pay creditors.

Why Your Home Is Considered an Asset

Your home is considered an asset because it has value. Even if you still owe money on the mortgage, the house may be worth something above what you owe.

That extra value is called equity. If exemptions protect your equity, you may be able to keep the home. If not, the trustee may look at whether the property can be sold.

The Role of Mortgage Debt

Your mortgage is different from credit card debt or medical bills. A mortgage is secured debt, which means the lender has a legal claim on the house.

If you stop paying the mortgage, the lender can move forward with foreclosure. Bankruptcy may slow that process, but it does not, by itself, erase the mortgage lien.

Secured vs Unsecured Debt

This difference matters a lot.

- Secured debt is tied to property, like a mortgage or car loan

- Unsecured debt is not tied to property, like credit cards or personal loans

Because the house secures your mortgage, you must stay current or work out a repayment plan if you want to keep it.

Can I Keep My House If I File Bankruptcy?

The Short Answer

Yes, you may be able to keep your house if you file bankruptcy. But that depends on your finances and the type of bankruptcy you choose.

If you keep up with mortgage payments and your home equity is protected, you often have a good chance of staying in the home.

Situations Where You Can Keep Your Home

You are more likely to keep your house if:

- You are current on your mortgage

- Your equity is within exemption limits

- You choose the right bankruptcy chapter

- You have a plan to catch up on missed payments

In many cases, homeowners use bankruptcy as a tool to protect their home rather than lose it.

When You May Lose Your House

You may be at risk if:

- You are far behind on payments

- Your home has too much non-exempt equity

- You cannot afford future mortgage payments

- You file under the wrong chapter for your situation

So the answer to “can I keep my house if I file bankruptcy” really depends on the details of your case.

Factors Courts Consider

The court may look at:

- Home value

- Mortgage balance

- Equity amount

- Bankruptcy exemptions

- Payment history

- Type of bankruptcy filed

Each factor helps decide whether the home can stay protected.

Bankruptcy and Your House

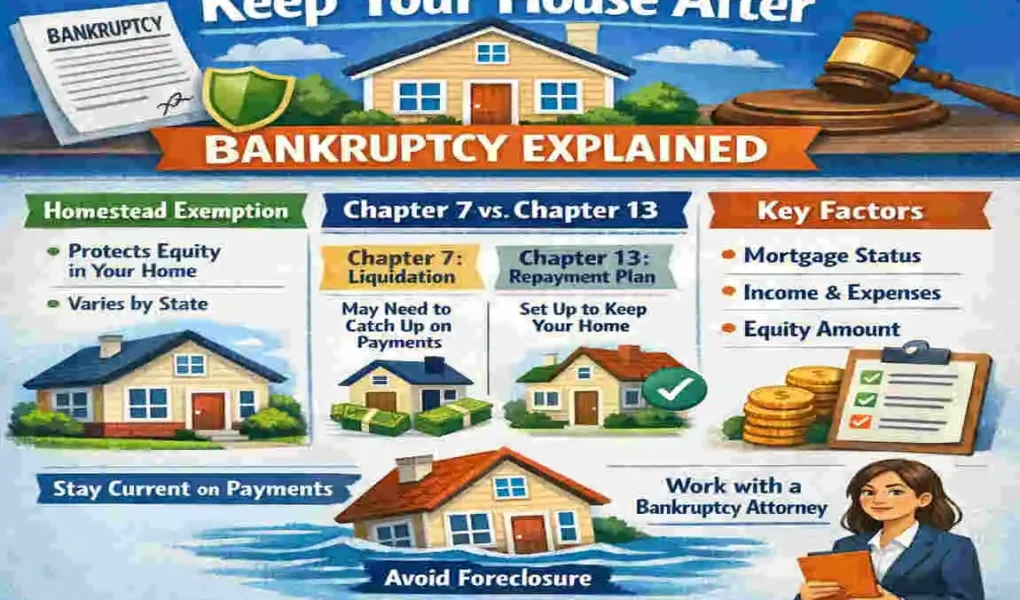

How Chapter 7 Works

Chapter 7 is often called liquidation bankruptcy. It can wipe out many unsecured debts, but it also gives the trustee power to review your assets.

That does not mean every homeowner loses their house. In fact, many people keep their home in Chapter 7 if the equity is protected and they stay current on payments.

Home Equity Rules

This is where things get important. If your home has a lot of equity that is not protected, the trustee may want to sell the property to pay creditors.

If your equity is low or fully covered by an exemption, the trustee may leave the home alone.

Bankruptcy Exemptions

Exemptions protect certain property from creditors. One of the most important is the homestead exemption, which helps protect your primary residence.

The amount protected depends on whether your state uses federal exemptions, state exemptions, or both. This can make a huge difference in whether you keep your house.

Keeping Current on Mortgage Payments

If you want to keep your home in Chapter 7, staying current on mortgage payments is very important.

Bankruptcy may clear other debts, but the mortgage remains. If you stop paying, the lender can still foreclose after the bankruptcy process.

When the Trustee May Sell Your Home

A trustee may consider selling the house if:

- The home has valuable equity

- Exemptions do not protect that equity

- Selling the home could pay creditors

This is why you should never assume Chapter 7 automatically protects your home. It might, but only if the numbers work in your favour.

Bankruptcy and Your House

How Chapter 13 Protects Homeowners

Chapter 13 works differently from Chapter 7. Instead of liquidating assets, it creates a repayment plan that lasts several years.

This is why many homeowners with missed mortgage payments choose Chapter 13. It gives them time to catch up while keeping the house in order.

Catching Up on Missed Mortgage Payments

If you are behind on your mortgage, Chapter 13 may help you bring those missed payments into a court-approved plan.

That means you do not have to pay everything at once. Instead, you spread the missed amount over time, which can make home retention more realistic.

Repayment Plans

A Chapter 13 plan usually lasts three to five years. During that time, you make payments to the trustee, who then distributes funds to creditors.

This can help you stay in your home as long as you keep making both the regular mortgage payment and the plan payment.

Benefits Compared

Chapter 13 may be better if:

- You are behind on mortgage payments

- You have too much equity to protect in Chapter 7

- You want more time to catch up

- You need foreclosure protection

For many homeowners, Chapter 13 offers a stronger path to keeping the house.

Home Equity and Bankruptcy Explained

What Is Home Equity?

Home equity is the difference between what your home is worth and what you still owe on the mortgage.

For example, if your home is worth $250,000 and you owe $180,000, you may have $70,000 in equity.

How Equity Impacts Bankruptcy

Equity matters because it reflects how much value your home has after subtracting debt. If that equity is protected, the house may stay safe.

If it is not protected, the trustee may view it as money available to pay creditors.

Federal vs State Homestead Exemptions

A homestead exemption is the legal protection for your home equity.

Some states offer generous protection. Others offer less. In some cases, federal exemptions may be available instead. The system used in your state can strongly affect the outcome.

Why Exemption Limits Matter

Exemption limits matter because they decide how much of your equity stays protected. If your equity is below the limit, you may be able to keep the house more easily.

If your equity is above the limit, part of it may be at risk. This is one of the biggest reasons people ask whether I can keep my house if I file bankruptcy before filing.

Tips to Keep Your House During Bankruptcy

Here are a few simple but important steps:

- Stay current on mortgage payments

- Know your homestead exemption

- Choose the right bankruptcy chapter

- Keep homeowner’s insurance active

- Respond quickly to court notices

- Work with a qualified bankruptcy attorney

- Do not transfer property before filing

These steps can help you avoid mistakes that put your home at risk.

Common Mistakes That Can Cost You Your Home

Ignoring Mortgage Payments

If you stop paying your mortgage, the lender may still foreclose even if you file bankruptcy. Bankruptcy is not a magic shield for missed mortgage payments.

Hiding Assets

Do not hide your luxury home or other assets from the court. That can cause serious legal trouble and may hurt your case.

Waiting Too Long to File

If foreclosure is already moving fast, waiting too long can limit your options. Early action gives you more choices.

Choosing the Wrong Bankruptcy Chapter

Filing the wrong chapter can create problems. Chapter 7 may not work well if you have too much equity or need time to catch up on payments.

Not Understanding Exemption Laws

Exemption laws are very important. If you do not understand them, you may make a decision that puts your house at risk.

Frequently Asked Questions

Can I keep my house if I file bankruptcy?

Yes, many people can keep their homes if they stay current on mortgage payments and qualify for homestead protection.

Will Chapter 7 take my home?

Not always. If your equity is protected and you keep paying the mortgage, you may keep the house.

Does Chapter 13 stop foreclosure?

Yes, it usually creates an automatic stay that can pause foreclosure and give you time to repay missed payments.

What is a homestead exemption?

It is a legal rule that protects some of the equity in your primary home from creditors.

Can I file bankruptcy if I’m behind on my mortgage?

Yes. Chapter 13 is often used by homeowners who need time to catch up on missed payments.

| Topic | Information |

|---|---|

| Can You Keep Your House? | Yes, many people can keep their home after filing bankruptcy, depending on the bankruptcy type and financial situation. |

| Chapter 7 Bankruptcy | You may keep your house if your home’s equity is protected by exemptions and you stay current on mortgage payments. |

| Chapter 13 Bankruptcy | Lets you keep your home while repaying missed mortgage payments through a 3–5 year repayment plan. |

| Mortgage Payments | Continuing to make on-time mortgage payments is usually required to keep your home. |

| Home Equity Exemptions | Federal or state exemption laws may protect part or all of your home’s equity from creditors. |

| Risk of Foreclosure | If you cannot keep up with mortgage payments, the lender may still foreclose after bankruptcy. |

| Automatic Stay | Filing bankruptcy temporarily stops most foreclosure actions through an automatic stay. |

| Second Mortgages | In some Chapter 13 cases, certain junior liens may be removed if legal requirements are met. |

| Best Option | Chapter 13 is often the better choice for homeowners who are behind on mortgage payments. |

| Key Takeaway | Bankruptcy does not automatically mean losing your home. The outcome depends on your bankruptcy chapter, equity, exemptions, and ability to maintain mortgage payments. |