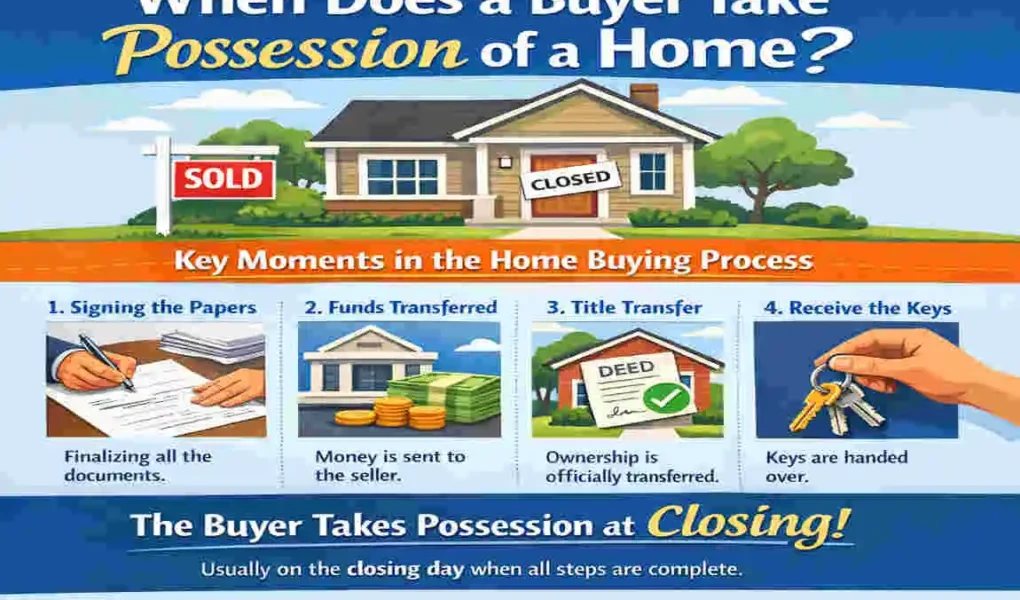

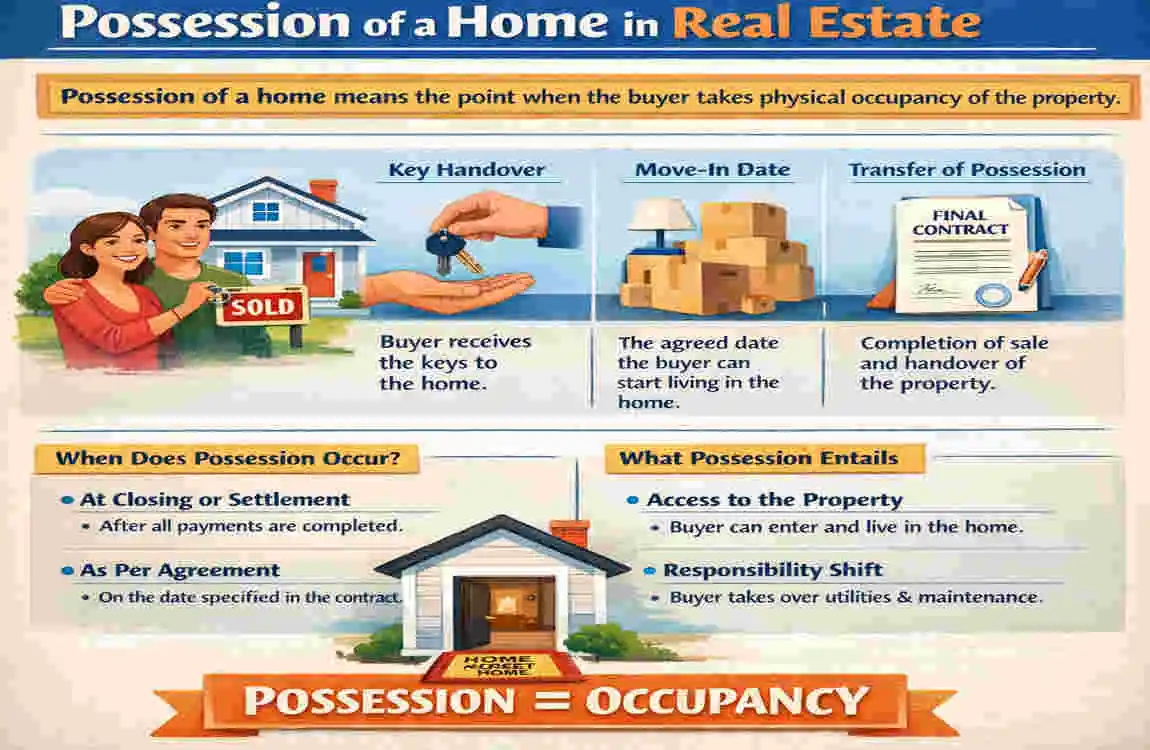

Buying a home is exciting, but one question matters a lot: when does the buyer take possession of the home? In simple terms, possession is the moment you can legally move in, get the keys, and start using the property as your own.

This is an important step because closing day and possession day are not always the same thing. Sometimes you get the keys right after closing. In other cases, the seller may stay for a short time after the sale, or you may agree to move in later.

If you are planning to purchase a home, it helps to understand the full timeline. That way, you can prepare your move, set up utilities, and avoid last-minute stress.

What Does “Possession of a Home” Mean?

Definition of Home Possession

Possession of a home means you have the right to occupy the property. In most cases, this happens when the sale is complete, the money has been transferred, and the property is officially yours.

It usually includes receiving the keys, garage openers, mailbox keys, and any access codes tied to the home.

Why Possession Day Matters

Possession day matters because this is when your responsibilities begin. You are now the person in charge of the home, which means you may need to handle:

- Utilities

- Insurance

- Security

- Maintenance

- Moving plans

It is also the day many buyers have been waiting for, so getting the timing right makes the whole move much smoother.

When Does Buyer Take Possession of Home?

Possession on Closing Day

In most home sales, the buyer takes possession on closing day. This is the most common setup. Once the loan funds are released, the title is transferred, and the seller has completed their part, you can usually take the keys.

This is the simplest arrangement because everything happens together. You close the sale, the sale is recorded, and then you move in.

Possession After Closing

Sometimes the seller needs extra time to move out. In that case, the buyer may close on the luxury home but take possession later. This is often called a rent-back agreement or delayed possession.

This arrangement can work well if both sides agree in writing. Still, you should be clear about the exact move-out date, who pays for utilities, and what happens if the seller stays longer than planned.

Early Possession Before Closing

Early possession is when a buyer moves in before the sale is fully closed. This is rare and usually not recommended.

It can pose legal and financial risks because the home is not yet fully yours. If something goes wrong with the loan, title, or contract, the situation can become messy fast.

Understanding the Home Closing Process

Final Walk-Through

Before closing, you usually do a final walk-through. This is your chance to check that the home is in the agreed condition.

You can look for things like:

- Unfinished repairs

- Damage after the inspection

- Missing appliances

- Cleanliness

- Signs the seller removed items they were supposed to leave

This step is important because it gives you one last look before the home becomes yours.

Signing Closing Documents

At closing, you sign the paperwork needed to complete the sale. These papers may include mortgage documents, title forms, and the settlement statement.

This is the official part of the real estate closing process. Once everything is signed and approved, the transfer can move forward.

Funding and Recording

After the documents are signed, the lender sends the money. Then the title is recorded in your name.

Once that is done, the deal is complete. This is usually the point when you can finally take possession of the home.

Timeline from Offer Acceptance to Possession

Stage Typical Timeline

Offer Accepted Day 1

Home Inspection 7–10 Days

Loan Approval 2–4 Weeks

Final Walk-Through 1–2 Days Before Closing

Closing Day 30–60 Days

Buyer Takes Possession Same Day or As Agreed

This timeline can change based on the lender, the seller, and the condition of the home. Some purchases move faster, while others take longer.

What Happens on Possession Day?

Receiving the Keys

On possession day, you usually receive the house keys and any other access tools. These may include:

- Garage remotes

- Mailbox keys

- Security codes

- Gate openers

This is often the moment buyers feel the move is truly real.

Utility Transfers

You also want to make sure the utilities are ready. This includes:

- Electricity

- Water

- Gas

- Internet

If you do not transfer these ahead of time, you may move in only to find the home without basic services.

Home Inspection Checklist

Before unpacking, check the home carefully. Test lights, locks, faucets, and appliances. Make sure everything works as expected.

A quick checklist can help you spot issues early:

- Test doors and windows

- Check plumbing

- Make sure heating and cooling work

- Look at walls and floors

- Confirm smoke detectors are active

Situations That Can Delay Possession

Mortgage Funding Delays

If the lender is late releasing money, possession may be delayed. This happens when paperwork is incomplete, or approval is still pending.

Title Problems

If there are title issues, the sale may not be final yet. The property must have a clear title before you can legally take possession.

Seller Hasn’t Moved Out

Sometimes the seller needs more time. If that happens, you may need to wait until they vacate the property, unless you already agreed otherwise.

Unexpected Repairs

Last-minute repair problems can also slow things down. This is especially true if the home inspection found issues that still need to be fixed.

Weather or Natural Disasters

Bad weather or other emergencies can affect closing and move-in schedules. Even a simple delay can push possession back a day or more.

Who Pays for the Property Before Possession?

Seller Responsibilities

Until possession changes hands, the seller usually remains responsible for the home. That means they should keep the property in decent condition and continue handling their side of the agreement.

Buyer Responsibilities

Once ownership transfers, you become responsible for the home. This is when you should begin managing insurance, utilities, and general upkeep.

Insurance Coverage

Home insurance is very important during this time. Make sure your policy is ready before closing so your new home is protected as soon as you own it.

Tips for Buyers Before Taking Possession

Before moving in, a little planning can save you a lot of stress.

- Schedule movers early

- Transfer utilities ahead of time

- Change the locks right away

- Deep clean before unpacking

- Keep closing papers organized

- Document the condition of the home with photos

These simple steps help you settle in faster and avoid common problems.

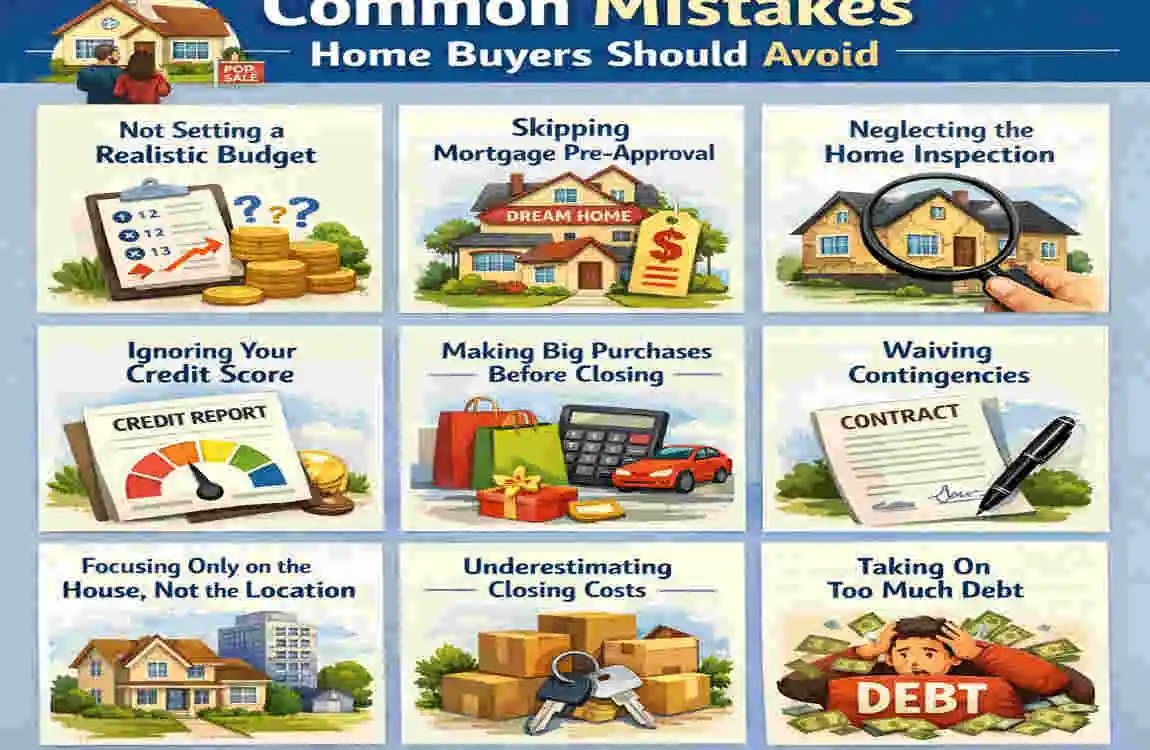

Common Mistakes Buyers Should Avoid

Some buyers run into trouble because they rush the process. Here are a few mistakes to watch out for:

- Moving in before closing

- Skipping the final walk-through

- Forgetting homeowner’s insurance

- Not changing the locks

- Ignoring utility setup

- Missing possession deadlines

If you avoid these problems, your move will feel much easier and more secure.

Frequently Asked Questions

What does possession date mean when buying a house?

It is the date on which the buyer gains the legal right to move into the home and use it.

When does the buyer take possession of the home after closing?

Usually on the same day as closing, unless the contract says otherwise.

Can a buyer move in before closing?

Yes, but it is uncommon and risky. It should only happen if both sides agree in writing.

Can the seller stay in the home after closing?

Yes, if a rent-back or delayed possession agreement is included in the contract.

What happens if the seller refuses to leave?

This becomes a legal issue, and you should contact your real estate professional or attorney right away.

| Stage | What It Means |

|---|---|

| Closing Day | In most real estate transactions, the buyer takes possession on the closing date after all documents are signed and funds are transferred. |

| After Recording | In some areas, possession is granted once the deed is officially recorded with the local government. |

| Immediate Possession | Many purchase agreements allow the buyer to move in immediately after closing. |

| Delayed Possession | The seller may stay in the home for a few days or weeks after closing if a post-closing occupancy agreement is included. |

| Early Possession | Some buyers can move in before closing through a separate early occupancy agreement, though this is less common. |

| Key Handover | The buyer typically receives the house keys once possession officially transfers. |

| Utilities & Services | Buyers usually transfer utilities and homeowner services to their name on the possession date. |

| Final Walk-Through | A final inspection is often completed within 24 hours before possession to ensure the home is in the agreed condition. |

| Legal Possession Date | The exact possession date is stated in the purchase agreement and is legally binding. |