Home insurance can help in some drainage and plumbing situations, but not all of them. That is where many homeowners get confused. A pipe may burst, a drain may clog, or water may back up into the house, and the damage can be expensive very fast.

It usually depends on what caused the problem. If the damage was sudden and accidental, your policy may help. If the issue is due to poor maintenance, gradual wear and tear, or old pipes, it is often excluded.

| Drainage or Plumbing Issue | Usually Covered by Home Insurance? | Notes |

|---|---|---|

| Burst pipes | Yes | Covered if damage is sudden and accidental |

| Accidental water leaks | Yes | Interior water damage is often included |

| Sewer backup | Sometimes | Usually requires additional sewer backup coverage |

| Clogged drains | No | Maintenance-related issues are typically excluded |

| Flood-related drainage damage | No | Requires separate flood insurance |

| Pipe corrosion or wear and tear | No | Considered a maintenance issue |

| Frozen pipe damage | Yes | Covered if reasonable precautions were taken |

| Underground drain pipe damage | Sometimes | May require service line coverage add-on |

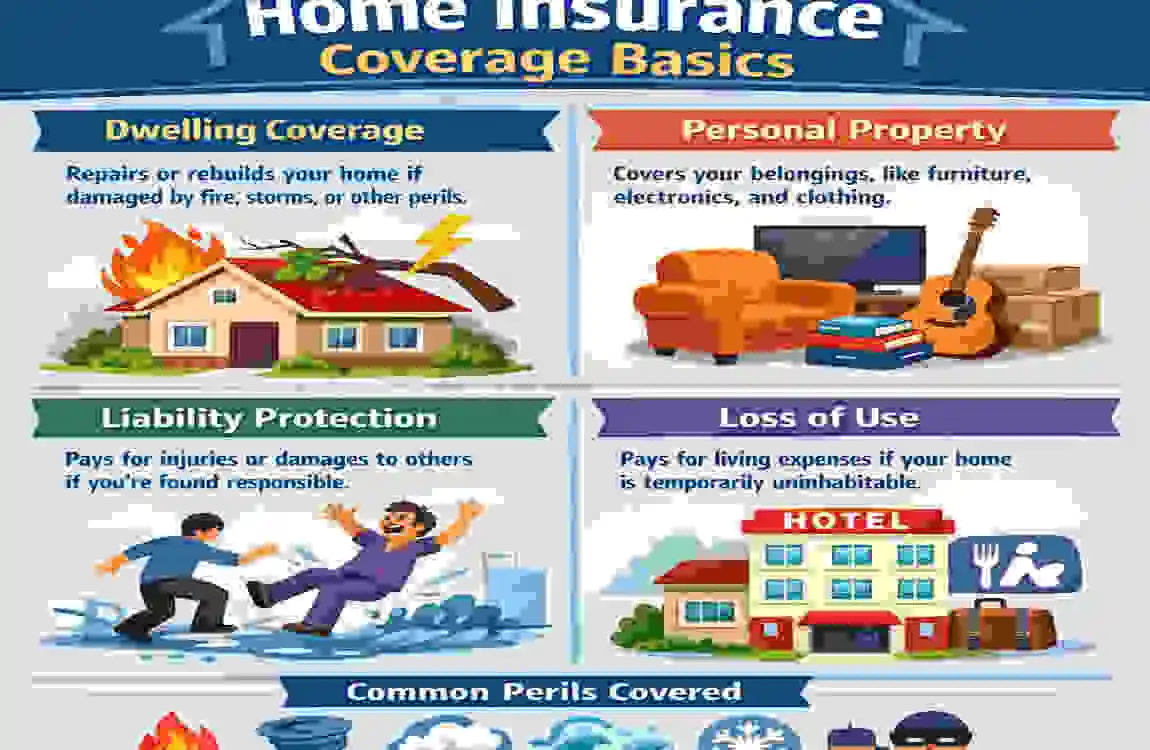

Understanding Home Insurance Coverage Basics

What Standard Home Insurance Policies Typically Cover

Most standard home insurance policies include several main types of coverage.

Dwelling coverage helps pay for damage to the structure of your home, such as walls, floors, and built-in features.

Personal property coverage protects your belongings, like furniture, clothing, and electronics, if a covered event damages them.

Liability protection helps if someone gets hurt on your property and you are found responsible.

Additional living expenses, often called ALE, may help pay for temporary housing and other costs if your home becomes unlivable after a covered loss.

Difference Between Sudden Damage and Maintenance Issues

This is one of the most important rules in insurance.

Insurance usually covers sudden and accidental damage. That means something unexpected happened, like a pipe bursting overnight.

Insurance usually does not cover damage caused by wear and tear, age, or neglect. For example, if a pipe has been leaking for months and you never repaired it, that is often treated as a maintenance problem.

Why Plumbing and Drainage Claims Are Common

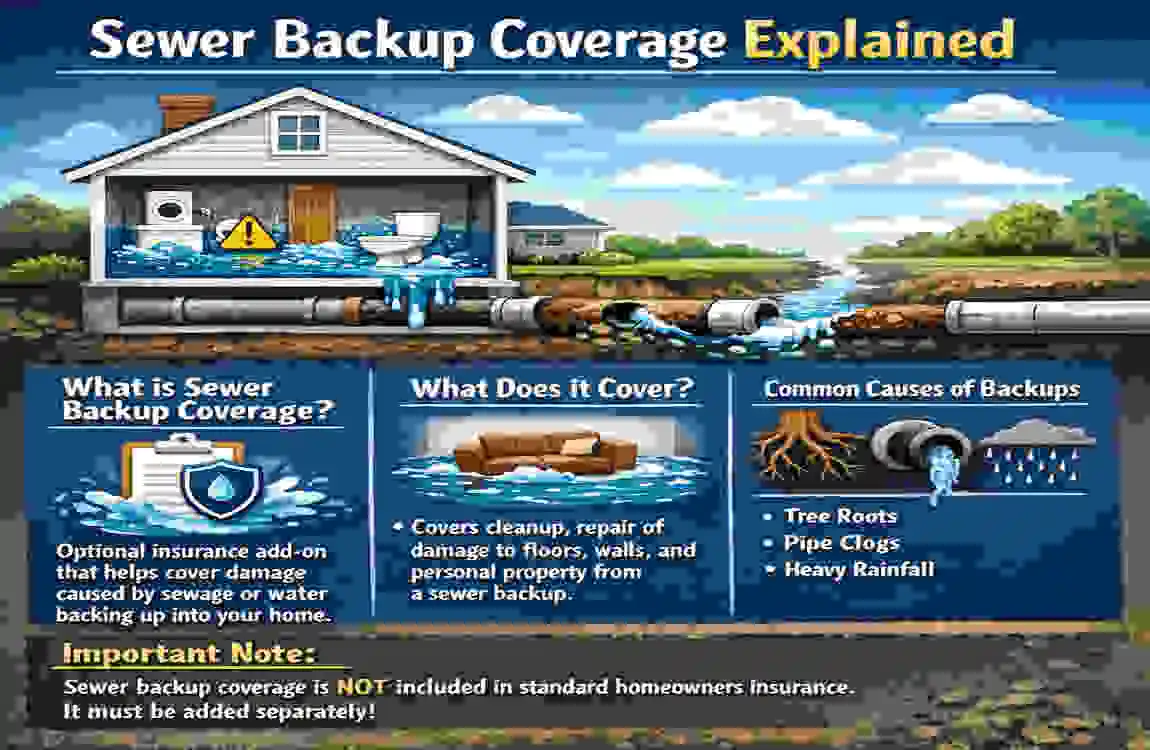

Plumbing and drainage problems happen often because homes deal with daily water use and weather changes. Common causes include:

- Aging pipes

- Heavy rainfall

- Tree root intrusion

- Frozen pipes

- Poor maintenance

That is why plumbing insurance claims and homeowners insurance water damage claims are so common. Drainage problems in homes can appear suddenly, but the root cause is often hidden for years.

Does Home Insurance Cover Plumbing and Drainage?

When Plumbing Damage Is Usually Covered

Home insurance often helps when the plumbing problem is sudden and not caused by neglect.

Common covered situations may include:

- A burst pipe

- An accidental leak

- Water overflow from an appliance

- A pipe that cracks because of freezing

If a pipe breaks and water damages your flooring or drywall, the policy may help cover the repair costs.

Drainage Issues That May Be Covered

Some drainage problems may also be covered if they happen suddenly and cause interior damage.

Examples may include:

- Water damage from an accidental drainage failure

- Overflow that damages walls, floors, or furniture

- Some storm-related drainage incidents, depending on the policy

The key question is not only what happened, but why it happened. That is why insurers look closely at the cause of loss.

Examples of Covered Claims

Here are a few simple examples:

- A kitchen pipe bursts and ruins the flooring

- A toilet overflows and damages the drywall

- A frozen pipe cracks during winter and floods a room

In each case, the damage happened quickly and unexpectedly. That makes the claim more likely to be covered.

Coverage Depends on the Cause of the Damage

This is the part many people miss.

Insurance companies care more about the cause of the loss than the drainage issue itself. If the problem was sudden, it may be covered. If the problem came from neglect, age, or poor upkeep, it may be denied.

So, when asking whether home insurance covers plumbing and drainage, always ask: What caused the water damage?

What Plumbing and Drainage Problems Are Not Covered?

Gradual Wear and Tear

Insurance usually does not pay for damage that builds over time.

Examples include:

- Corroded pipes

- Slow leaks

- Old drainage systems that fail from age

These problems are often seen as normal deterioration rather than a surprise event.

Poor Maintenance and Neglect

If warning signs were ignored, the insurer may deny the claim.

For example:

- You noticed a leak but did not fix it

- You ignored repeated drain clogs

- Moisture built up for months and caused mold

This is why plumbing maintenance responsibilities matter so much. Insurance expects homeowners to take reasonable care of their systems.

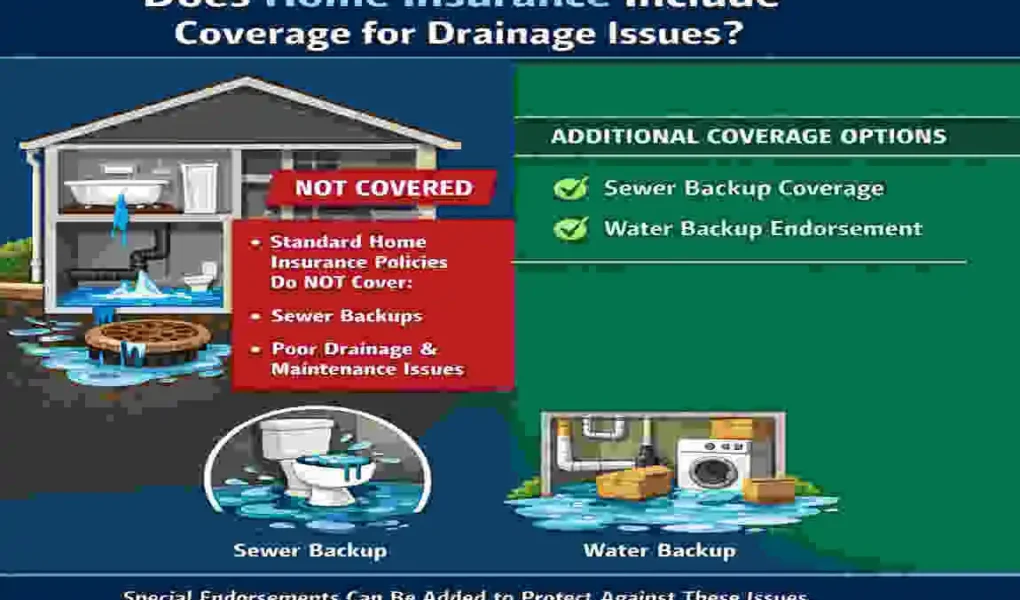

Sewer Backup Exclusions

Most standard policies do not include sewer backup coverage automatically.

That means if sewage backs up through a drain or toilet, you may need a separate add-on or endorsement. Without it, the claim may be denied.

Flood-Related Drainage Problems

If drainage issues occur due to flooding, standard home insurance usually will not help.

That type of damage often needs separate flood insurance.

Sewer Backup Coverage Explained

What Is Sewer Backup Insurance?

Sewer backup insurance is usually an optional add-on. It helps protect your home from wastewater backups through drains, toilets, or sump pump systems.

This type of coverage is often called a sewer backup endorsement.

What Sewer Backup Coverage Usually Includes

This coverage may help pay for:

- Cleanup costs

- Water removal

- Damaged flooring and furniture

- Repair expenses

It can be very helpful if sewage enters the basement or lower levels of your home.

Typical Coverage Limits

Like all insurance, sewer backup protection has limits. That means the policy will only pay up to a certain amount.

You will also usually have a deductible, which is the amount you pay before the insurance begins to help.

Is Sewer Backup Coverage Worth It?

For many homeowners, yes.

It may be especially useful if you live in:

- An older neighborhood

- An area with heavy rain

- A home with a basement

If you are worried about backups, this add-on can bring real peace of mind.

Does Home Insurance Cover Drain Pipes Outside the House?

Underground Drain Pipe Coverage

Exterior drain pipes may be covered in some situations, but not always.

If a buried pipe suddenly breaks and causes damage, your policy may help cover the cost. But if the pipe failed because of age or root damage, coverage may be limited.

Service Line Coverage Add-Ons

Some insurers offer service line protection for:

- Water lines

- Sewer lines

- Drain pipes

- Electrical service lines

This kind of coverage can be useful because underground repairs can be costly and hard to spot early.

Common Exclusions for Exterior Pipes

Exterior pipes are often excluded when the problem comes from:

- Tree root damage

- Pipe deterioration

- Ground movement

So if you are worried about underground pipe insurance, it is smart to review your policy carefully.

Water Damage vs Flood Damage: Understanding the Difference

What Counts as Water Damage

Water damage usually comes from inside the home.

Examples include:

- A burst pipe

- A leaking appliance

- An overflowing sink or toilet

This kind of damage is often covered if it is sudden and accidental.

What Counts as Flood Damage

Flood damage usually results from water entering the home from outside.

Examples include:

- Rising groundwater

- Storm surge

- Overflowing rivers

This usually requires separate flood insurance.

Why This Difference Matters for Claims

This is one of the biggest reasons claims get denied.

A homeowner may think, “Water is water.” But insurers do not see it that way. Standard insurance often covers internal water damage, while flood insurance covers water that enters the home from the outside.

Water Damage Flood Damage

Burst pipe Rising river

Appliance overflow Heavy rainfall flooding

Usually covered Requires flood insurance

How to File a Plumbing or Drainage Insurance Claim

Steps to Take Immediately

If a plumbing or drainage issue happens, act fast.

- Shut off the water supply

- Try to stop further damage

- Contact your insurer right away

Document the Damage

Good records help support your claim.

Take:

- Photos and videos

- Receipts for emergency repairs

- Plumber reports

Work With an Insurance Adjuster

Your insurer may send an adjuster to inspect the damage. They will review the cause, the extent of the loss, and whether the claim fits your policy.

Tips to Improve Claim Approval Chances

- Act quickly

- Keep maintenance records

- Understand your policy wording

The more organized you are, the easier the process becomes.

How to Prevent Plumbing and Drainage Problems at Home

Routine Plumbing Maintenance Tips

A little care can prevent big trouble.

- Inspect pipes regularly

- Clean drains often

- Monitor water pressure

Seasonal Prevention Strategies

Weather can put extra stress on your home.

- Winterize pipes before freezing weather

- Clear gutters and drains before storms

Install Preventive Devices

Some simple devices can reduce risk.

- Sump pumps

- Backwater valves

- Leak detectors

Why Prevention Helps With Insurance Claims

Prevention does more than protect your home. It also shows that you are properly caring for it.

That can help avoid claim denials caused by neglect.

How Much Does Plumbing and Drainage Coverage Cost?

Factors Affecting Insurance Costs

The cost of coverage depends on things like:

- Home age

- Location

- Plumbing condition

- Previous claims history

Average Cost of Sewer Backup Riders

Sewer backup add-ons are usually affordable compared to the cost of major water damage repairs. Prices vary, but they are often modest for the protection they provide.

Is Additional Coverage Worth the Investment?

For many homeowners, yes.

A small yearly cost may protect you from a very expensive cleanup and repair bill. That makes extra coverage worth considering, especially if your home has older systems or a basement.

Frequently Asked Questions

Does homeowners insurance cover clogged drains?

Usually no, if the clog occurred due to buildup, misuse, or lack of maintenance. If the clog caused sudden water damage, some parts of the damage may be covered under the policy, depending on the policy.

Does insurance pay for pipe replacement?

Usually not, if the pipe failed due to age, corrosion, or wear and tear. If the pipe bursts suddenly due to a covered event, the resulting damage may be covered.

Is mold from plumbing leaks covered?

Sometimes, but only if the mold came from a covered water loss and you acted quickly. Long-term mold from ignored leaks is often excluded.

Does insurance cover sewer line repair?

Not usually under a standard policy. Some homeowners buy extra service line or sewer line coverage for this type of repair.

What happens if a drain backs up into my basement?

If you have sewer backup coverage, your policy may help with cleanup and repairs. Without that add-on, the claim may not be covered.

Do I need flood insurance for drainage problems?

If the issue comes from outside flooding, yes, you usually need flood insurance. Standard home insurance does not normally cover flood damage.