Buying a home usually starts with one big question: can you prove enough income to qualify for a mortgage? Lenders look closely at this because they want to know you can make your monthly payments without trouble.

| Factor | Lender Consideration | Explanation |

|---|---|---|

| Unemployment Benefits | Usually NOT accepted | Considered temporary and not stable long-term income |

| Job Stability | Very important | Lenders prefer consistent employment history |

| Alternative Income (rental, investments) | Accepted | Must be documented and consistent |

| Government Loans (FHA/VA/USDA) | Sometimes considered indirectly | Still require proof of stable repayment ability |

| Co-borrower Income | Accepted | Can strengthen application if primary applicant is unemployed |

| Cash Savings | Helpful but not income | Supports affordability but doesn’t replace income |

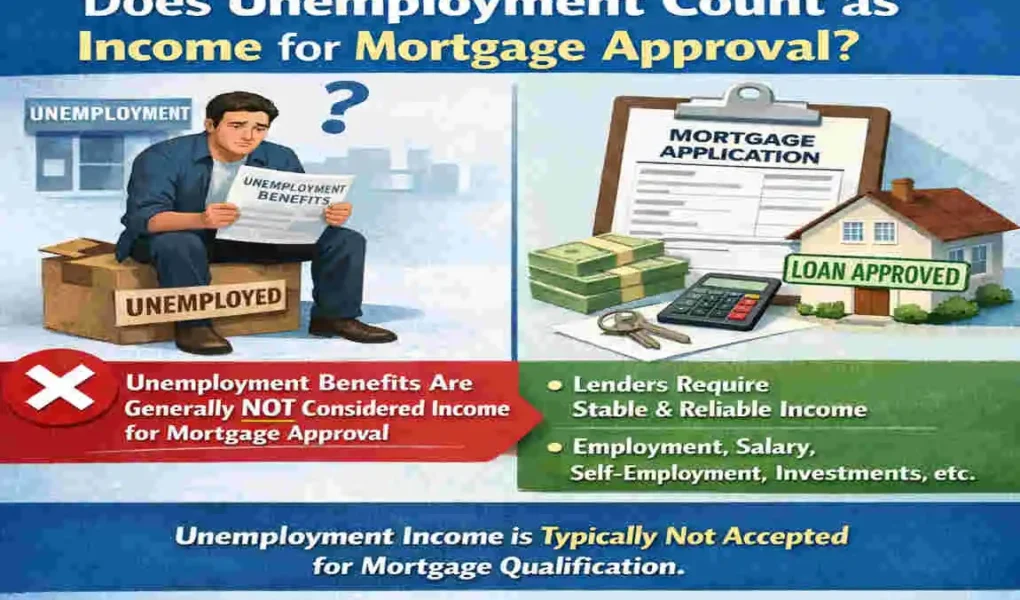

This is where many people get confused, especially when they are receiving unemployment benefits. If you are wondering whether unemployment counts as income when buying a house, the short answer is usually no for mortgage approval.

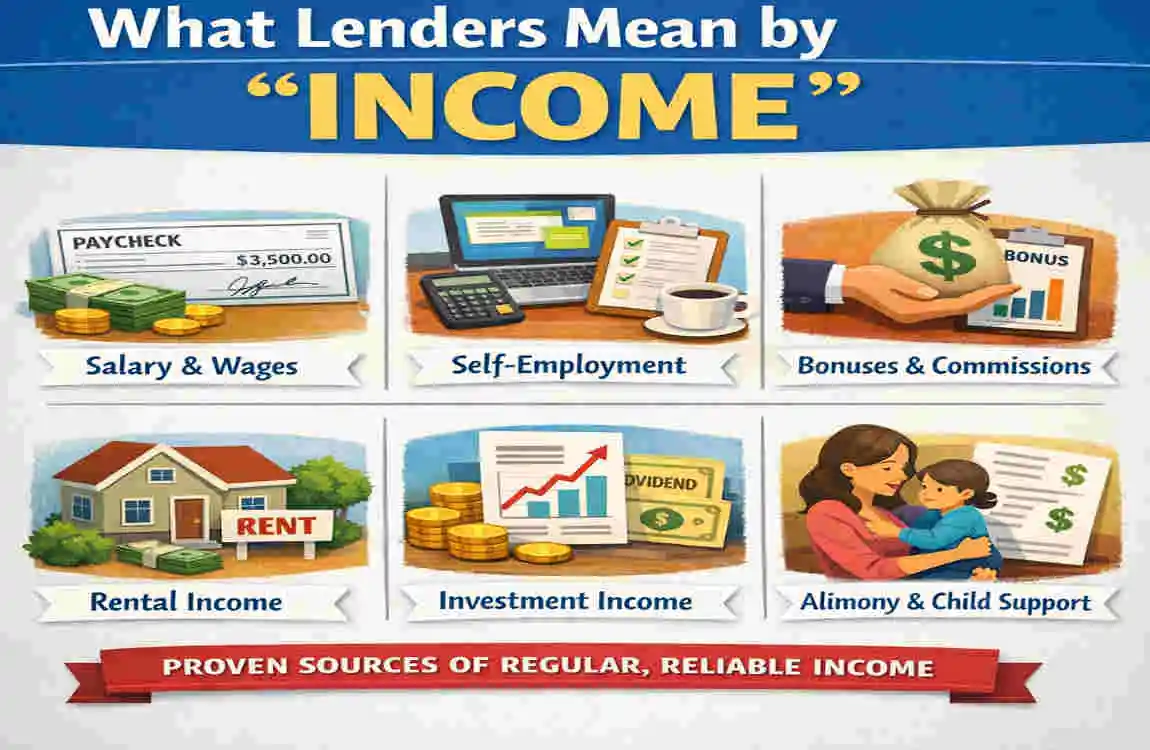

What Lenders Mean by “Income”

Types of acceptable income sources

Lenders prefer income that is steady and easy to verify. This usually includes:

Income Type Lender View

Full-time wages Strong and reliable

Part-time wages Acceptable if consistent

Self-employment income Accepted with proof

Rental income Often accepted

Retirement income is usually accepted if stable

Investment income may be accepted if regular

What lenders prioritize

Lenders care most about stability, predictability, and documents. They usually want pay stubs, tax returns, or bank records that show the income is real and ongoing.

Why income classification matters

Not every source of money counts the same way. A lender wants to see income that will likely continue after the loan closes. That is why some payments help with everyday bills but do not help much with mortgage approval.

Does Unemployment Count as Income When Buying a House?

Short answer

In most cases, unemployment benefits do not count as qualifying income for a mortgage.

Why lenders usually reject it

Unemployment benefits are temporary. They are meant to support you while you look for work, not to show long-term earning power. Because of that, lenders usually do not treat them as stable income.

Exceptions in some cases

There are a few situations where unemployment-related money may be reviewed differently, such as:

- short gaps between jobs for seasonal workers

- temporary underwriting reviews

- cases where a co-borrower has a high income

Even then, the lender usually wants to see stronger sources of income before approving the loan.

When Unemployment Benefits May Be Considered

Temporary support, not main qualification income

Unemployment benefits may help show that you have some cash coming in, but they are rarely enough by themselves to qualify for a mortgage.

Government-backed loan rules

Programs like FHA, VA, and USDA loans can be flexible in some areas, but they still require proof of stable income. These loans are not designed to approve borrowers solely based on unemployment benefits.

Documents lenders may ask for

If unemployment income is reviewed at all, lenders may want:

- benefit award letters

- bank statements showing deposits

- proof of prior employment

- records explaining why the job ended

Types of Income That Strengthen Mortgage Approval

Stronger income sources

If you want a smoother approval process, these income types help more than unemployment benefits:

- full-time salary

- part-time work with a steady history

- self-employment income with tax proof

- rental income from property

- dividends, pensions, or retirement income

- co-borrower income from a spouse or partner

Why do these help more

These income sources show a lender that money is coming in regularly. That gives the lender more confidence that you can handle the loan.

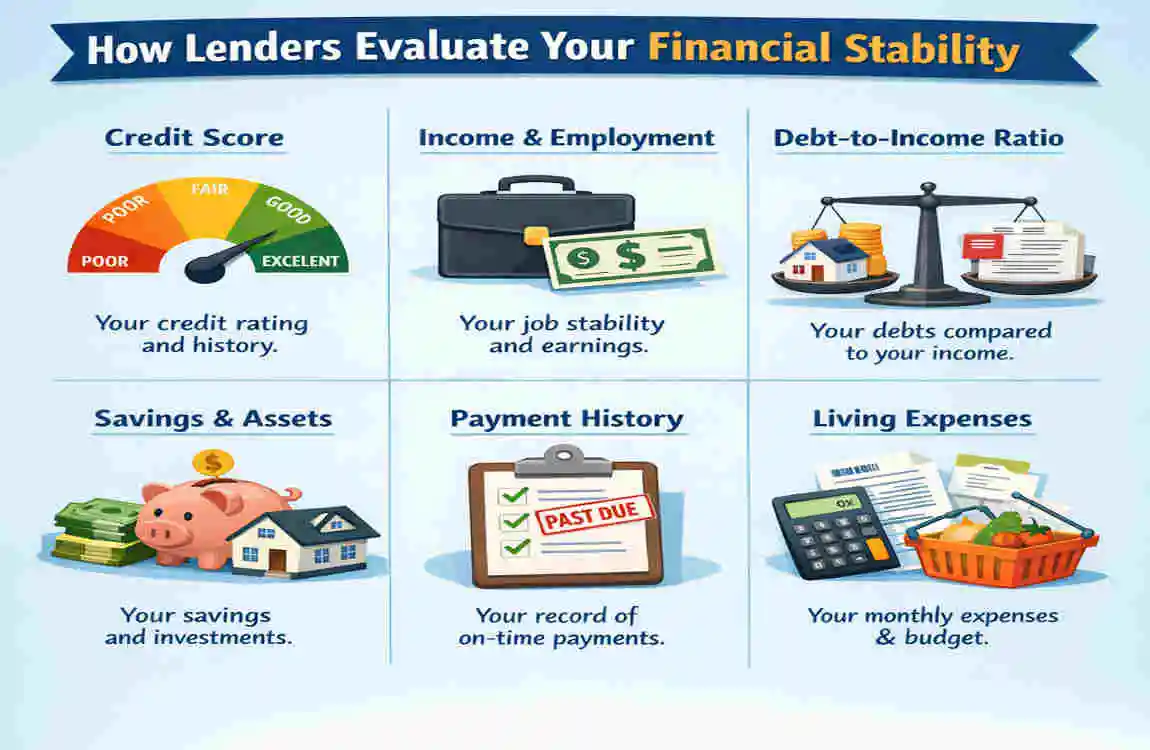

How Lenders Evaluate Your Financial Stability

Debt-to-income ratio

Your debt-to-income ratio, or DTI, compares your monthly debt to your monthly income. A lower DTI usually makes approval easier.

Credit score

A stronger credit score can help, but it does not replace income. Lenders still want to see that you can pay the mortgage each month.

Employment history

Stable work history matters a lot. A lender wants to know that your income has been steady and is likely to continue.

Savings and cash reserves

Extra savings can help, especially if your income is inconsistent. Still, savings usually support the application rather than completely replace income.

What Happens If You Are Unemployed but Want to Buy a House?

Main challenges

If you are unemployed, you may face:

- loan rejection

- stricter lender review

- less favorable loan terms

- higher interest rates if approved

Possible alternatives

If you are not working right now, you may want to:

- wait until you are employed again

- add a co-borrower

- Make a larger down payment

- Use other stable income sources if available

Loan Options and Programs

FHA loans

FHA loans can be more flexible, but they still require stable, verifiable income.

VA loans

VA loans may work well for eligible veterans, but income must still be documented and dependable.

USDA loans

USDA loans can help with rural home purchases, but the borrower must still show stable household income.

Conventional loans

Conventional loans are usually the strictest. They often need the clearest proof of reliable income.

Common Myths About Unemployment and Mortgage Approval

Myth: Any income is enough

Not true. Lenders care about stable income, not just any money coming in.

Myth: Government benefits guarantee approval

Also false. Benefits may help with living costs, but they usually do not guarantee a mortgage.

Myth: Credit score alone decides approval

Credit matters, but income, savings, and debt level matter too.

Myth: Savings can replace income completely

Savings help, but they usually cannot fully replace a steady income source.

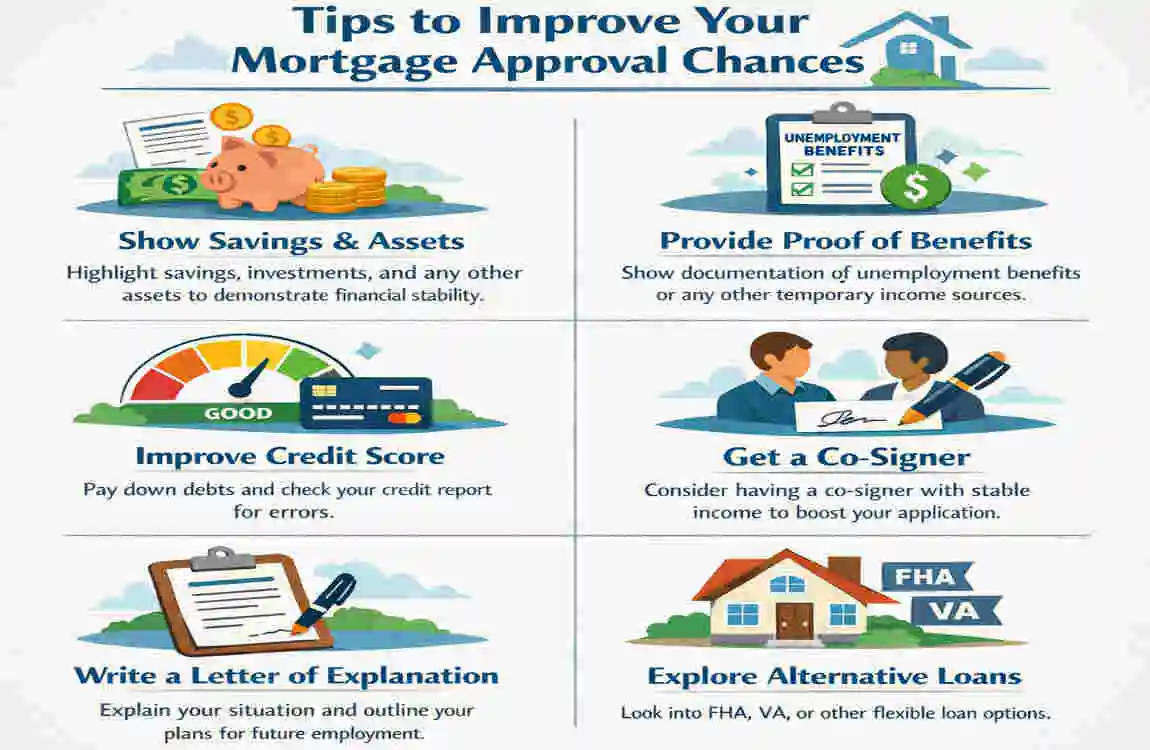

Tips to Improve Mortgage Approval Chances

Build a stronger application.

You can improve your chances by:

- getting stable employment first

- paying down debt

- improving your credit score

- saving more for the down payment

- speaking with a mortgage broker

These steps can make a big difference, especially if your income history is not simple.

Frequently Asked Questions

Can unemployment benefits be used to qualify for a mortgage?

Usually no. They may be reviewed in some cases, but they are not commonly accepted as qualifying income.

Do lenders check unemployment history?

Yes, they may review your employment history and ask why your income changed.

Can I get a house loan while unemployed?

It is possible in rare cases, but much harder without other strong sources of income.

What income do banks accept for mortgages?

Banks usually accept wages, self-employment income, rental income, retirement income, and some investment income if it is stable and documented.

How long should I be employed before applying?

Many lenders prefer a steady work history, often around two years, though this can vary by loan type.