A roof replacement is one of the most expensive repairs a homeowner can face. It can cost thousands of dollars, which is why many people wonder whether insurance will help cover it. If you are asking how to claim a new roof on your homeowners insurance, you are not alone.

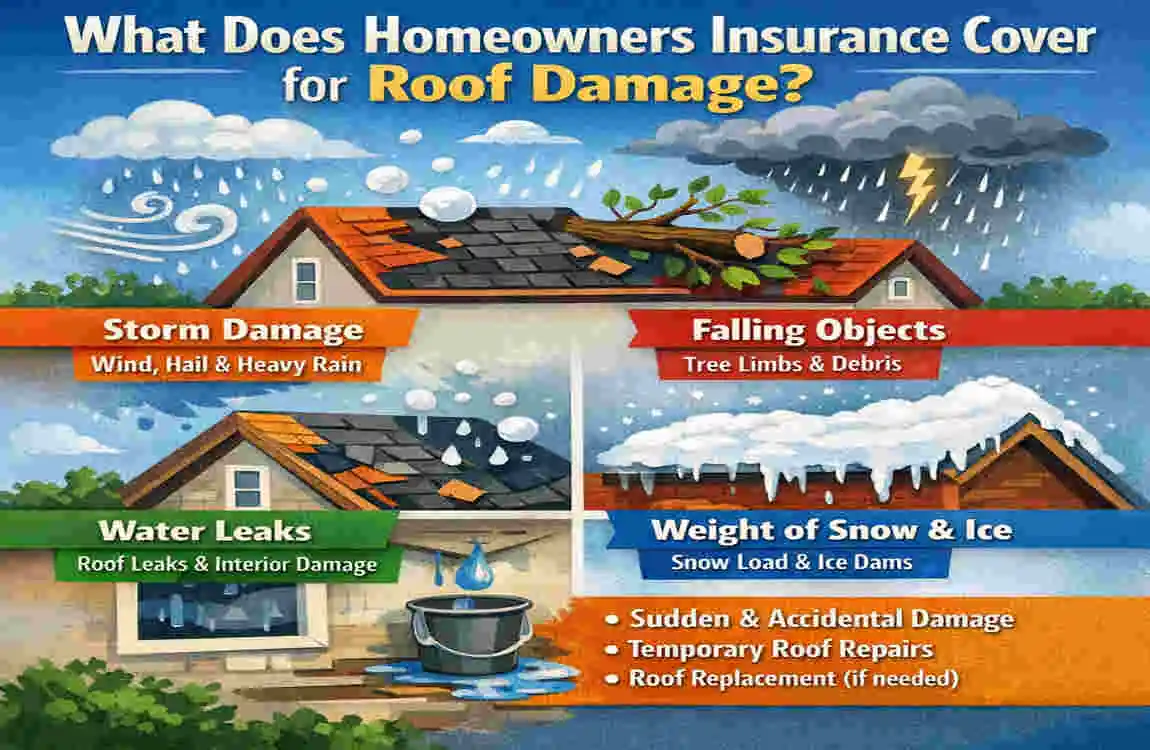

The short answer is yes, sometimes. Homeowners insurance may cover the cost of a new roof if the damage is caused by a covered event such as hail, wind, fire, lightning, or a fallen tree. But it usually will not pay for damage caused by age, wear and tear, or poor maintenance.

| Situation | Usually covered? | Notes |

|---|---|---|

| Storm, hail, wind, fire damage | Yes | File a claim, document damage, and pay your deductible. |

| Age, wear and tear, neglect | No | Insurance generally excludes normal deterioration. |

| Full roof replacement after covered loss | Sometimes | Coverage depends on your policy, roof age, and deductible. |

That is where many claims become confusing. One homeowner may get a full roof replacement approved, while another only gets a small repair or has a claim denied. The difference often comes down to the cause of damage, the condition of the roof, and how well the claim is documented.

What Does Homeowners Insurance Cover for Roof Damage?

Understanding Roof Coverage

Homeowners insurance is designed to protect your home from sudden and accidental damage. For the roof, that usually means damage caused by a covered peril. A covered peril is simply a problem your policy agrees to pay for.

If your roof is damaged by a storm, fire, or falling debris, your policy may help with repairs or even a full replacement. But if the roof slowly deteriorates over time, insurance usually treats it as a maintenance issue, not a sudden loss.

That is an important difference. Insurance helps with unexpected events, not normal aging.

Common Covered Causes of Roof Damage

Some of the most common covered causes include:

- Hail storms

- Wind damage

- Fallen trees

- Fire damage

- Lightning strikes

- Severe weather events

If one of these events hits your home and your roof is badly damaged, you may have a strong roof replacement insurance claim.

Common Exclusions

Insurance does not cover everything. In many cases, claims are denied because a covered event did not cause the damage. Common exclusions include:

- Normal wear and tear

- An old roof reaching the end of its life

- Poor maintenance

- Manufacturing defects

- Neglect

If your roof already had weak spots, missing shingles, or long-term leaks, the insurer may argue that the damage was not sudden.

Can You Claim a New Roof Through Homeowners Insurance?

When Insurance Will Pay for a New Roof

Yes, you can often claim a new roof through homeowners insurance when the damage is serious enough and caused by something the policy covers.

This is more likely when:

- A major storm tears off large sections of the roof

- Hail causes widespread damage

- A tree falls and crushes part of the roof

- Fire or lightning causes major structural damage

- The roof suffers a total loss

If the damage is severe, insurance may approve a full replacement instead of a repair.

When Insurance May Only Cover Repairs

Sometimes the insurer agrees that damage exists but says only part of the roof needs work. This often happens when:

- The damage is limited to one area

- The rest of the roof still looks sound

- The roof is older but still usable

- The problem is seen as minor or cosmetic

In these cases, the company may only pay for the damaged section.

Full Replacement vs Partial Replacement

Insurers consider several factors when deciding between repair and replacement. They may inspect:

- How much of the roof is affected

- Whether the damage is spread out

- The age and condition of the roof

- Whether matching repair materials are available

- Whether the damage weakens the roof as a whole

If the roof cannot be repaired fairly or safely, a full replacement becomes more likely.

Situation Likely Outcome Why

Small hail damage on a newer roof Partial repair Damage is limited

Major wind damage across many sections Full replacement Damage is widespread

Old roof with missing shingles Often denied or limited repair Age and wear are excluded

Tree falls on roof during storm Full or partial replacement Sudden covered event

Slow leak over several years Usually denied Gradual damage is not covered

How to Claim a New Roof on Your Homeowners Insurance: Step-by-Step Process

Assess the Damage Safely

After a storm or accident, do not rush onto the roof if it looks unsafe. Broken shingles, slick surfaces, and weak spots can be dangerous.

Instead, walk around your home and look for visible signs like:

- Missing shingles

- Dented gutters

- Fallen branches

- Water stains on ceilings

- Pieces of roofing on the ground

Take photos and videos from the ground and from inside the home if water has entered. The sooner you document the damage, the better.

Review Your Insurance Policy

Before you file, read your policy carefully. You want to understand:

- Your deductible

- Your coverage limits

- Whether your policy uses RCV or ACV

- Any special rules for wind or hail damage

Here is the simple version:

- Replacement Cost Value (RCV) means insurance may help pay for a new roof at today’s prices, minus your deductible.

- Actual Cash Value (ACV) means the amount the insurance pays for the roof after depreciation. Older roofs usually get less money.

This one detail can significantly affect your payout.

Contact Your Insurance Company

Report the claim as soon as you can. Delays can cause problems, especially if further damage occurs later.

When you call, be ready to share:

- Your policy number

- The date of the storm or damage

- What happened

- What you noticed so far

- Whether the home is leaking or unsafe

Keep your explanation clear and honest. Do not guess. Just describe what you saw.

Schedule an Insurance Inspection

The insurance company will usually send an adjuster to inspect the roof. This person checks whether the damage matches your claim and whether it came from a covered event.

During the inspection, the adjuster may look for:

- Missing or lifted shingles

- Bruising from hail

- Soft spots

- Broken flashing

- Signs of age or prior repairs

Be present if possible. You can point out the damage you found and share your photos.

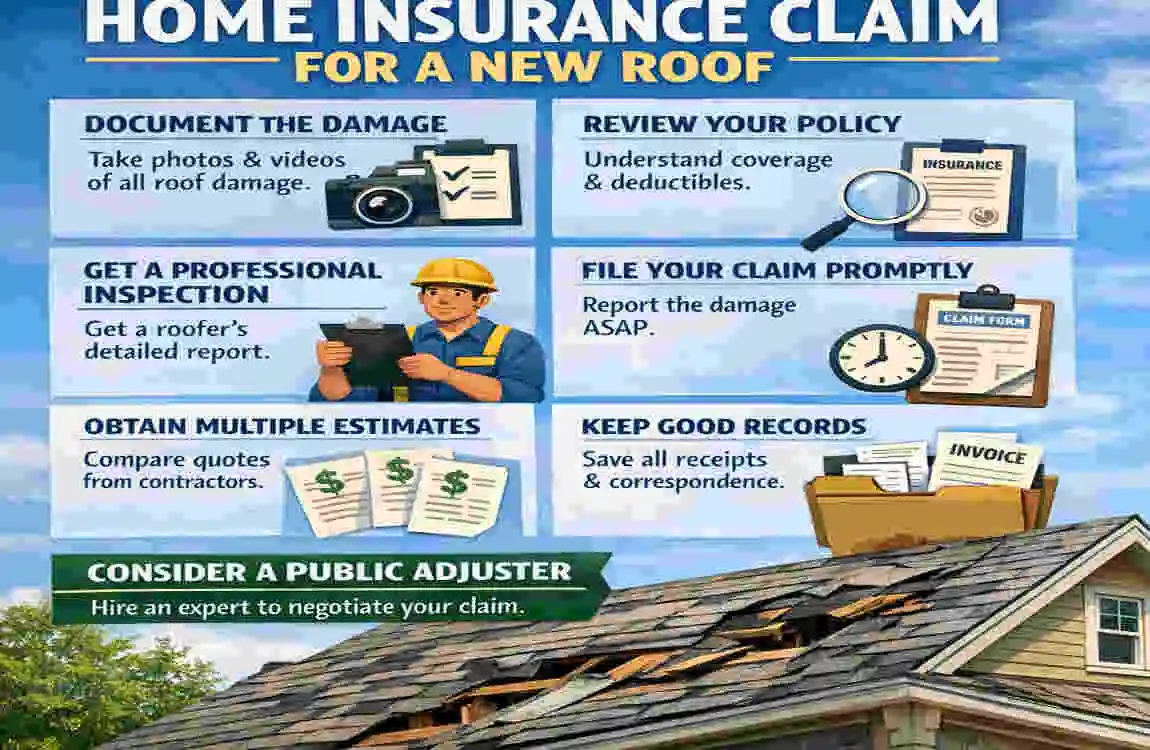

Obtain a Professional Roofing Inspection

An independent roofing contractor can give you another opinion. This can help if the damage is hard to see or if you think the insurer missed something.

A contractor may provide:

- A written roof inspection

- Photos of the damage

- A repair or replacement estimate

- Notes about storm impact or structural issues

This paperwork can strengthen your insurance claim for roof damage.

Receive Claim Approval

If the claim is approved, the insurer will send a settlement offer. Read it carefully. Check:

- What repairs are approved

- Whether it is a repair or replacement

- How much the deductible is

- Whether depreciation is being withheld

- What paperwork you need next

Do not rush to accept if something looks off. Ask questions if the estimate seems too low.

Hire a Licensed Roofing Contractor

Once the claim is approved, choose a trusted contractor. Look for someone who is licensed, insured, and experienced with insurance work.

Be careful with anyone who:

- Pressures you to sign quickly

- Promises to “get you a free roof”

- Asks you to lie on paperwork

- Offers a deal that sounds too good to be true

Good contractors help you through the process without pushing scams.

Complete the Roof Replacement

The contractor will remove the damaged roof, install the new materials, and clean up the site. Depending on the size of the job, this may take a day or several days.

A final inspection may be done after the work is finished. Keep all paperwork and receipts in one place.

Receive Final Insurance Payment

If your policy is RCV, you may receive part of the payment first and the rest later. That second payment is often referred to as recoverable depreciation.

This means the insurer withholds part of the money until the work is completed. After you submit the final invoice, they release the rest.

That is how many roof insurance settlement claims are finished.

Documents You’ll Need for a Roof Insurance Claim

Essential Documentation Checklist

A strong claim depends on good records. Keep these items ready:

- Insurance policy details

- Photos of damage

- Repair estimates

- Roofing contractor reports

- Maintenance records

- Weather reports

- Claim correspondence

Why Proper Documentation Matters

Good records can make the claim move faster. They can also reduce arguments about what happened and when.

If the insurer asks for proof, your documents can show:

- The damage was sudden

- The roof was maintained

- The storm really happened

- The repair cost is reasonable

In short, paperwork helps you protect your claim.

Factors That Affect Roof Claim Approval

Roof Age

Newer roofs are usually easier to insure. Older roofs often face more pushback because insurers assume age contributed to the damage.

Type of Damage

Sudden damage is easier to cover than gradual damage. A storm, tree fall, or fire is different from a roof that slowly wears out over time.

Maintenance History

If you can show that you took care of the roof, your claim may look stronger. Regular inspections and small repairs can help prove the damage was not caused by neglect.

Policy Type

Your policy matters a lot. An RCV policy usually provides better protection than an ACV policy because it is more likely to cover a full replacement.

Local Weather Conditions

If your area recently had hail, high wind, or a major storm, that can support your claim. Weather records may help prove the roof damage came from a real event.

How Insurance Companies Calculate Roof Replacement Payments

Actual Cash Value (ACV)

ACV means the insurer pays the roof’s value after age and use are deducted. For older roofs, this can be much less than the cost of a new one.

Replacement Cost Value (RCV)

RCV means the insurer pays what it costs to replace the roof today, not what the old roof was worth after wear and tear. This usually leads to a better payout.

Deductibles Explained

Your deductible is the part you pay first before insurance starts paying.

There are two common types:

- Fixed deductible: a set dollar amount

- Percentage deductible: based on a percentage of your home’s insured value

Always check this before filing. A large deductible can reduce your final payout.

Sample Roof Claim Calculation

Here is a simple example:

Item Amount

Roof replacement estimate $14,000

Depreciation -$3,500

Deductible -$1,000

Initial payment $9,500

Recoverable depreciation after work is done $3,500

This is only an example, but it shows how a payout may be split into two parts.

Common Reasons Roof Insurance Claims Get Denied

Lack of Evidence

If you cannot show clear damage, the insurer may deny the claim. Photos, reports, and estimates matter.

Delayed Claim Filing

Waiting too long can hurt your case. The insurer may argue that the damage worsened because you did not report it promptly.

Pre-Existing Damage

If the roof was already damaged before the storm, the insurer may refuse to pay for that part.

Poor Roof Maintenance

A roof that was never maintained can raise red flags. Missing maintenance records can make denial more likely.

Policy Exclusions

Some damage simply is not covered. That includes wear and tear, gradual leaks, and some types of cosmetic damage.

Contractor Fraud Concerns

If the insurer thinks a contractor inflated the estimate or exaggerated the damage, they may deny or reduce the claim.

How to Avoid Claim Denials

A few simple habits can help:

- File quickly

- Take clear photos

- Keep maintenance records

- Use honest estimates

- Work with reputable professionals

Tips to Maximize Your Roof Insurance Claim

Document Damage Immediately

Do not wait days or weeks. Take photos right after the storm if it is safe to do so.

Keep Maintenance Records

Save receipts for inspections, repairs, and cleaning. These records can show your roof was cared for.

Work With Reputable Roofing Contractors

A trusted contractor can explain the damage clearly and help you avoid mistakes.

Understand Your Policy

Know what your policy covers before you file. That simple step can save time and stress.

Request a Second Inspection if Necessary

If the first inspection missed damage, ask for another look. A second opinion can change the outcome.

Consider a Public Adjuster for Complex Claims

If your claim is large or complicated, a public adjuster may help. They work on your side and can help present the case more clearly.

What If Your Roof Claim Is Denied?

Review the Denial Letter

Start by reading the denial letter carefully. It should explain why the claim was rejected.

Gather Additional Evidence

If you have more photos, weather records, or contractor notes, bring them together.

Request Reconsideration

You can ask the insurer to review the claim again. Be polite, clear, and organized.

File an Appeal

If the denial still stands, follow the appeal process listed in your policy or denial letter.

Seek Professional Assistance

For serious disputes, you may need help from:

- Public adjusters

- Roofing experts

- Insurance attorneys

The right help can make a big difference in a hard case.

Frequently Asked Questions

Does homeowners insurance cover an old roof?

Sometimes, but not always. If the damage resulted from a covered event, the roof’s age does not automatically end coverage. Still, older roofs are more likely to receive limited payments or denials because insurers may attribute the damage to wear and tear.

How long do I have to file a roof insurance claim?

This depends on your policy and state rules, but you should file as soon as possible. Waiting too long can weaken your claim.

Will filing a roof claim increase my premiums?

It might. A claim can affect future rates, especially if your area has many storm claims. Still, a valid claim may be worth it if the damage is serious.

Can I choose my own roofing contractor?

Yes, in most cases you can choose your own contractor. Insurance companies may suggest someone, but you are usually free to hire the roofer you trust.

What happens if repair costs exceed the estimate?

If the work costs more than the insurer estimated, your contractor can submit additional documentation. The insurer may review the extra costs before paying more.

Can I claim roof leaks through homeowners insurance?

Yes, if the leak resulted from a covered event, such as wind or hail. But if the leak was caused by long-term wear or neglect, it is often denied.

Does insurance cover cosmetic roof damage?

Sometimes, but not always. Some policies cover only functional damage, not damage that changes how the roof looks but not how it works.

Is hail damage always covered?

No. Hail damage is often covered, but only if your policy includes it and the damage is not considered old or minor. Documentation is very important.