Buying a home is exciting, but it can also feel stressful. When you find a house you love, it is easy to get caught up in the moment and lose sight of the price. That is one of the main reasons many buyers overpay. They focus on winning the house instead of checking whether the price truly makes sense.

| Indicator | What to Check | Why It Matters |

|---|---|---|

| Comparable Sales (Comps) | Compare the listing price to recently sold homes (last 30 days) in the same neighborhood | Homes in the same area should have similar prices; significantly higher = potential overpay |

| Online Valuation Estimates | Check Zillow/Zestimate, Redfin Estimate, or other automated valuations | If online estimates are drastically lower than the list price, you may be in the danger zone |

| Days on Market | How long has the home been listed vs. average for the area? | Homes listed for months/years often indicate overpricing |

| Price vs. Neighborhood | Is it the most expensive home in the neighborhood without justification? | Priced far higher than counterparts is a major red flag |

| Homes Taken Off Market | Are similar unsold homes priced similarly to this listing? | If unsold homes have similar prices, this home may be overpriced |

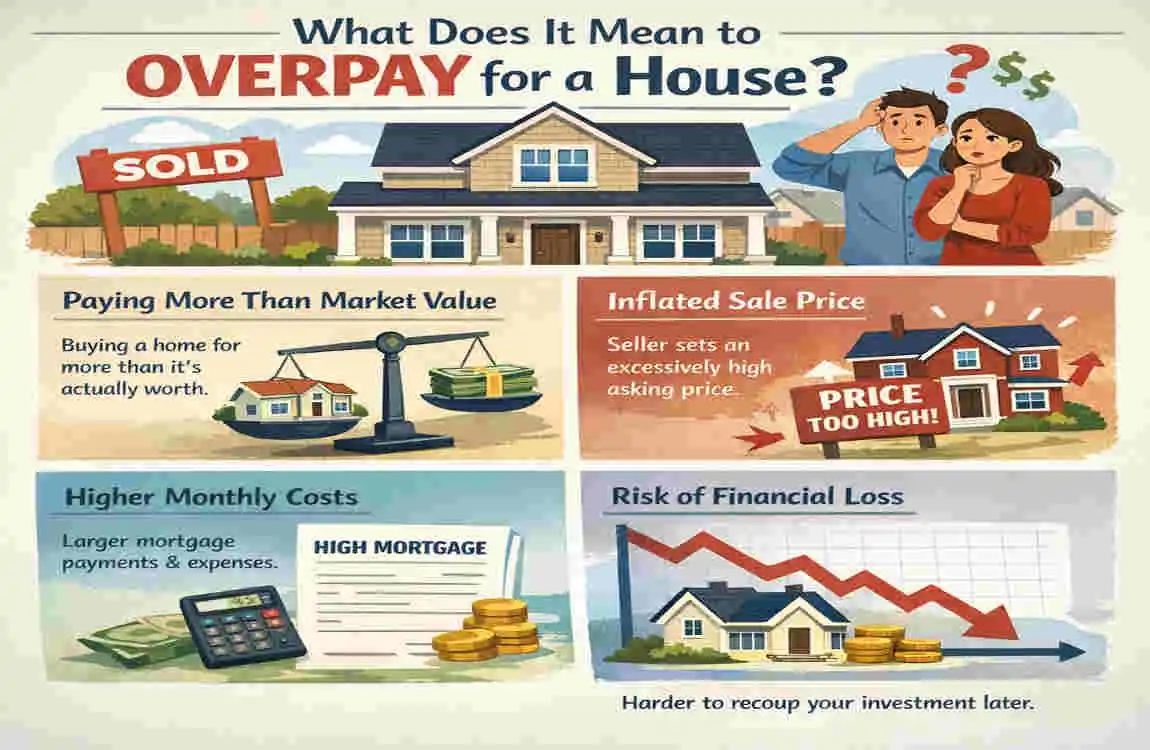

What Does It Mean to Overpay for a House?

Definition of Overpaying in Real Estate

Overpaying for a modern house means paying more than the home’s fair market value. In simple terms, it means the price you agree to is higher than what similar homes in the same area are selling for.

This does not always mean the house is “bad.” It just means the numbers may not support the price. A home can feel perfect to you and still be overpriced compared to the market.

It is also important to separate emotional value from real value. You may love the kitchen, the yard, or the location, but those feelings do not always change the homeis value to buyers in general.

Why Buyers Commonly Overpay

Many buyers overpay because of bidding wars, low inventory, and fear of losing the home. When several people want the same property, the pressure rises fast.

Another common reason is FOMO, or fear of missing out. Buyers may worry that if they do not act now, they will never find another home. That feeling can lead to rushed decisions.

Some buyers also skip research. If you do not study local sales, recent appraisals, or neighborhood prices, it is easy to make an offer that is too high.

Is Paying Above Asking Price Always Bad?

Not always. Sometimes paying above asking price can still make sense, especially in a fast-growing neighborhood or a very competitive market.

If home values in the area are rising quickly, a slightly higher price may still be reasonable over time. The key is to check whether real market data support the price.

In other words, paying above asking price is not automatically a mistake. It becomes a problem when the home price is higher than its true value, putting your finances under pressure.

10 Signs You May Be Overpaying for a House

The Home Appraisal Comes in Lower Than Your Offer

A home appraisal is an expert opinion of a propertyis value. Lenders care about appraisals because they want to make sure the home supports the loan amount.

If the appraisal is lower than your offer, that is a strong warning sign. It may mean you agreed to pay more than the home is worth. In many cases, the bank will only lend based on the appraised value, not your offer price.

Comparable Homes Sold for Much Less

Comparable homes, often called comps, are similar houses that recently sold nearby. If those homes sold for far less, your target home may be overpriced.

Look at homes with similar sizes, conditions, lot sizes, bedroom counts, and neighborhoods. Recent sales matter most because old sales may not reflect today’s market.

The House Has Been Sitting on the Market

A home that stays on the market too long can be a sign that the price is too high. Buyers are often passing on it for a reason.

Sometimes sellers guessed wrong on price. Other times, the house has issues that are not obvious at first glance. Either way, a stale listing gives you room to question the asking price.

You’re Waiving Important Contingencies

Contingencies are your safety net. They protect you if the inspection finds problems, the appraisal comes in low, or the loan does not go through.

If you are waiving the inspection, appraisal, or financing contingency, you are taking on more risk. That does not always mean you are overpaying, but it does mean you need to be extra careful.

The Seller Reduced the Price Multiple Times

Multiple price cuts can mean the home is not selling because the market disagrees with the original price.

This often creates a good opportunity for negotiation. If the seller has already reduced the price once or twice, they may be more open to a lower offer.

Monthly Payments Stretch Your Budget

A home can look affordable on paper and still leave you feeling squeezed every month. That is a sign you may be paying too much for your situation.

If the mortgage, taxes, insurance, repairs, and utilities push your budget too far, you may become house poor. That means most of your income goes to the home, leaving very little room for savings or daily life.

The Neighborhood Prices Don’t Match

If one house is priced much higher than the homes around it, you should ask why.

Sometimes a home is over-improved for the area. That means it has features that the neighborhood may not support in terms of resale value. It can also be risky to buy the most expensive house on the block if nearby homes are much cheaper.

Renovations Don’t Add Real Value

Not all upgrades raise value equally. Some cosmetic changes look nice but do not justify a big price jump.

A fresh coat of paint, trendy fixtures, or basic staging may improve appearance, but they do not always add much value. The same goes for DIY work without permits or sloppy flips that hide bigger problems.

Your Agent Seems Pushy

A good buyer’s agent should guide you, not rush you. If you feel pushed to make a fast offer without enough facts, pause and rethink.

You want someone who gives honest feedback, not someone who wants to close the deal. A pushy agent can make overpaying more likely.

Your Gut Feeling Says the Price Is Too High

Your instincts matter. If something feels off, do not ignore that feeling.

It may mean you need more information, a second opinion, or just more time. A smart buyer listens to the facts but also pays attention to discomfort when the numbers don’t seem right.

How to Check a House’s Fair Market Value

Compare Similar Home Sales (Comps)

This is one of the best ways to value a home. Compare recent sales of similar houses in the same area.

Focus on:

- Square footage

- Lot size

- Bedrooms and bathrooms

- Condition

- School district

- Recent sale date

The more similar the homes are, the more useful the comparison becomes.

Use Online Home Valuation Tools

Online valuation tools can give you a quick estimate. These tools use public data and market trends to create a rough price range.

They are helpful as a starting point, but they are not perfect. They may miss upgrades, repairs, or unique neighborhood details.

Analyze Price Per Square Foot

Price per square foot can help you compare homes more easily. You calculate it by dividing the asking price by the home’s square footage.

This method is useful, but it should not be used alone. Two homes can have the same size and still have very different values because of their layouts, conditions, and locations.

Hire a Professional Appraiser

If you want a more exact opinion, a professional appraiser can help. They examine the home, local sales, and condition before giving a value estimate.

This is especially useful when you are making a large purchase or when the price seems questionable.

Study Local Market Conditions

The value of a home also depends on the broader market. In a seller’s market, prices may rise because demand is strong and inventory is low. In a buyer’s market, homes may sit longer and sellers may negotiate more.

Interest rates, job growth, and available homes all affect pricing too. A home does not exist in isolation; the local market shapes it.

Quick Comparison Table

MethodWhat It ShowsBest Use

Comps What similar homes sold for Checking fair market value

Online tools Fast price estimate Early research

Price per square foot Easy comparison measure Screening similar homes

Appraisal Professional value opinion Final decision support

Market study Supply, demand, and trends Understanding price pressure

Key Factors That Affect House Prices

Location and Neighborhood Demand

Location plays a huge role in pricing. Good schools, low crime, access to shopping, and nearby jobs can raise home values.

Future development also matters. If a new transit line, shopping area, or employer is coming to the area, prices may rise over time.

Market Trends and Timing

Timing can affect how much you pay. Homes often sell faster in spring and summer, when more buyers are active.

Economic conditions matter too. When rates go up, buyer budgets shrink. When rates are lower, more buyers can afford to compete.

Home Condition and Age

A home with an old roof, aging HVAC, plumbing issues, or structural concerns should usually cost less than a home in better condition.

Age alone does not make a house bad, but older homes often need more upkeep. That cost should show up in the price.

Renovations and Upgrades

Some upgrades add value, like a modern kitchen, updated bathrooms, or energy-efficient systems.

Other upgrades do not add as much value as people expect. Very personal design choices may not appeal to future buyers.

Future Resale Potential

Always think beyond your first day in the house. Ask yourself how easy it will be to sell later.

A property with strong resale potential usually holds value better over time. Nearby growth, better roads, and community improvements can help.

How Much Above Asking Price Is Too Much?

Understanding Asking Price Psychology

The asking price is not always the true value. Some sellers list low to attract attention and start a bidding war.

Other sellers list high because they hope a buyer will pay more. That is why asking price should be treated as a starting point, not the final answer.

Typical Over-Ask Percentages by Market Type

In hot markets, buyers may sometimes pay several percent above asking price. In balanced markets, offers are often closer to list price. In slow markets, buyers may even pay below the asking price.

The right amount depends on local conditions. There is no single number that works everywhere.

Calculating Your Maximum Safe Offer

Your safest offer should fit your budget, not your emotions. Start with your monthly payment comfort zone, then factor in taxes, insurance, repairs, and savings.

If a higher offer would force you to cut back on essentials or emergency savings, it is probably too high for you.

Questions to Ask Before Making an Offer

Why Is the Seller Moving?

A seller who needs to move quickly may be more open to negotiation. A seller with no urgency may hold firm.

How Long Has the Property Been Listed?

The longer it has been listed, the more likely the price is too high or the home has a problem buyers noticed.

Have There Been Previous Offers?

If other buyers walked away, ask why. That can reveal issues with price, condition, or contract terms.

What Repairs or Issues Exist?

Always ask about known problems. A modern home that looks polished may still have expensive hidden repairs.

Is the Price Negotiable?

Never assume the asking price is fixed. Many sellers expect buyers to negotiate.

Smart Negotiation Strategies to Avoid Overpaying

Get Pre-Approved Before Shopping

Pre-approval helps you understand your real budget. It also shows sellers that you are serious.

Use Inspection Results Strategically

If the inspection reveals issues, you may be able to ask for repairs, credits, or a lower price.

Don’t Reveal Your Maximum Budget

Keep your top number private. If the seller knows your limit, you lose bargaining power.

Be Willing to Walk Away

This is one of your strongest tools. If the deal does not make sense, walk away and protect your money.

Work With a Skilled Real Estate Agent

A good agent knows local prices, market trends, and common negotiation tactics. That knowledge can help you avoid overpaying.

Simple Negotiation Tips

- Stay calm and stick to your budget.

- Use market data, not emotion.

- Ask for value, not just a lower number.

- Be patient if the home is overpriced.

Common Mistakes Home Buyers Make

Falling in Love With the House Too Early

Once emotions take over, people often justify a higher price. Try to stay practical until the numbers are clear.

Ignoring Hidden Repair Costs

A house may look affordable until you add repairs, maintenance, and upgrades. Always look at the full cost of ownership.

Focusing Only on Monthly Payments

A low monthly payment does not always mean a good deal. You also need to think about total price, interest, taxes, and future resale value.

Skipping Market Research

If you do not know what similar homes cost, you are guessing. And guessing can get expensive.

Buying Due to Pressure or Competition

A rushed decision is one of the fastest ways to overpay. Slow down and check the facts.

Should You Buy a House Even If It Seems Slightly Overpriced?

When Paying More Can Still Be Worth It

Sometimes a slightly higher price is acceptable. That may be true if the house is in your dream location, has rare features, or sits in a market where values keep rising.

If you plan to stay for many years, a small price difference may not matter much over time.

Situations Where You Should Walk Away

Walk away if the appraisal gap is large, repairs are severe, or the payment would strain your budget.

If buying the home would cause long-term stress, the deal is not worth it.

Long-Term vs Short-Term Thinking

A home should fit both your life today and your plans. If the house works long term, a slightly higher price may be acceptable.

But if you are stretching too far to win the deal, the pressure may not be worth it.

Expert Tips to Avoid Overpaying in Any Market

Research Before Touring Homes

Know the neighborhood prices before you even step inside. That way, you can spot bad deals faster.

Monitor Local Sales Weekly

The market changes quickly. Watching recent sales helps you stay current.

Stick to Your Financial Limits

Your limit should come from your budget, not from the excitement of the moment.

Never Skip Inspections

Inspections can uncover major problems that affect value and safety.

Keep Emotions Separate From Investment Decisions

A house cost should feel right, but it also has to make financial sense. Balance both sides.

FAQ

How do I know if I am overpaying for a house?

Check the home against similar recent sales, the appraisal, and the local market. If the price is much higher than comparable homes, that is a warning sign.

Is it normal to pay above asking price?

Yes, it can be normal in competitive markets. What matters is whether the price still matches fair market value.

What percentage over asking is reasonable?

There is no single safe number. In some hot markets, buyers may pay above asking, while in slower markets they may negotiate below asking.

Can a low appraisal mean I overpaid?

Yes, a low appraisal can suggest that your offer was above market value. It is one of the clearest warning signs.

How can I calculate fair market value?

Use recent comparable sales, price per square foot, online valuation tools, and, if needed, a professional appraiser.

Should I walk away from an overpriced house?

If the price is too high for your budget or the gap is too large, walking away is often the smartest move.

Do housing markets affect overpaying risks?

Yes. In a seller’s market, buyers face a higher risk of paying too much because demand is strong and inventory is tight.

Is buying in a seller’s market risky?

It can be. You may face bidding wars and feel pressure to move quickly, making careful research even more important.