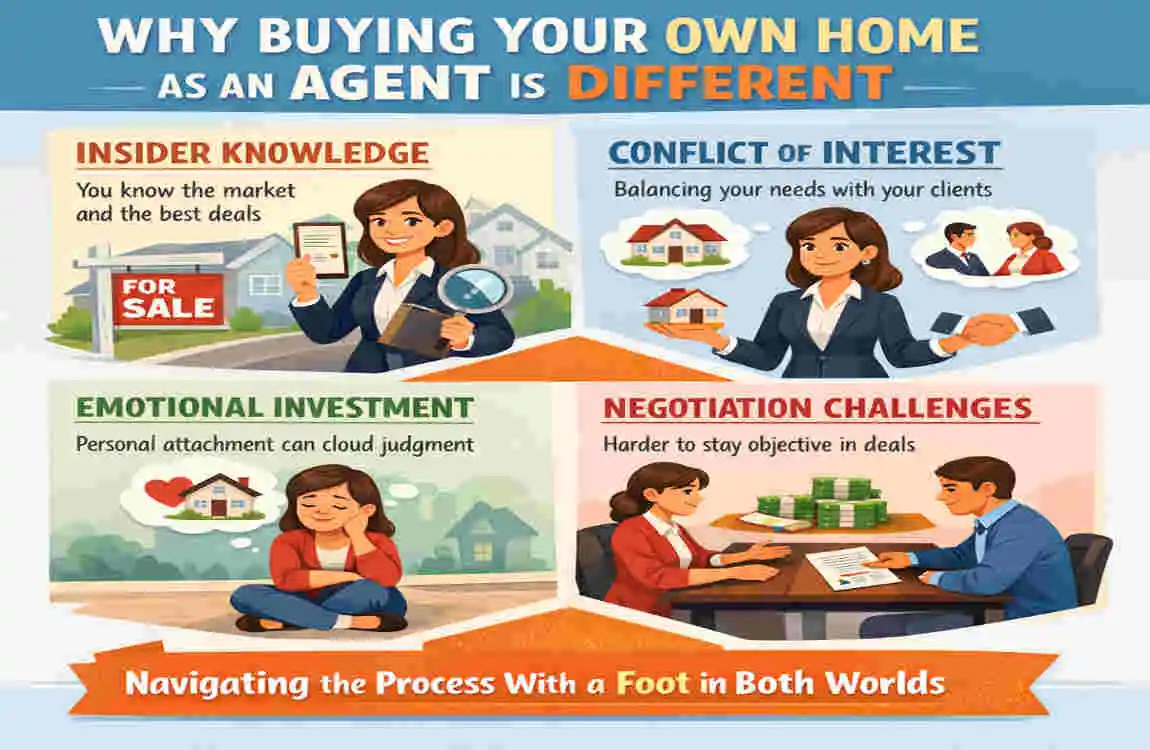

Buying a home is a big step for anyone, but buying a house as a real estate agent adds a few extra layers. You already know the market, the paperwork, and the pace of a real estate deal. That gives you an advantage.

| Method / Approach | How it works |

|---|---|

| Use own buyer‑agent commission | The agent represents themselves as the buyer and redirects the buyer‑side commission toward closing‑cost credits or repairs. |

| Buy their own listing (with disclosure) | The listing agent can buy the property they’re selling, but must disclose the dual role and follow local legal and brokerage rules. |

| Work with another agent | Some agents hire a different agent to avoid conflicts of interest and keep negotiations objective. |

| Leverage inside market knowledge | Agents use their access to off‑market deals, early listings, and pricing trends to time their purchase strategically. |

| Negotiate seller credits or terms | Agents often negotiate inspection credits, timelines, and financing terms more aggressively than typical buyers. |

At the same time, your professional role can create conflicts of interest, disclosure issues, and emotional pressure. That is why buying your own home as an agent is not just about finding the right property. It is also about staying careful, ethical, and organized.

Why Buying Your Own Home as an Agent Is Different

You have more market insight

As an agent, you usually have access to MLS data, market trends, and professional contacts. That can help you compare prices faster and spot value more easily than a regular buyer.

You may also be aware of upcoming listings, neighbourhood trends, and common inspection issues. This can save time and reduce guesswork.

But you also have more responsibility

Your experience does not exempt you from the rules. In fact, it often creates more responsibility. You must be careful with agency disclosures, brokerage policies, and any situation that could appear to be self-dealing.

You also need to avoid using private information from past clients or transactions in a way that could hurt trust.

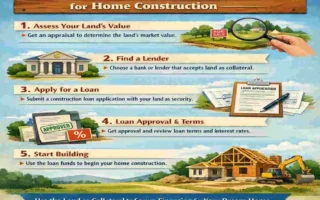

Preparing Financially

Get your credit and budget in shape

Before you shop, review your credit score, debts, and savings. Lenders will closely examine your income stability, especially if your commission income fluctuates month to month.

A strong plan includes:

- A healthy debt-to-income ratio

- Enough savings for the down payment

- Extra cash for closing costs and reserves

- A clear monthly payment target

If your income is uneven, it helps to be conservative. Do not base your budget on your best month. Base it on your average.

Organize your income documents

If you are a commission-based agent, lenders usually want solid proof of income. Keep these ready:

- Tax returns

- Bank statements

- Profit and loss records

- Commission statements

- Brokerage income documents

The more organized you are, the smoother the loan process becomes.

Understand how commission income affects approval

Many agents earn income in waves. One month may be busy, and the next may be slower. Lenders often average your income over time, which means you should be ready to explain your earnings clearly.

Quick comparison table

Loan or Income FactorWhat Lenders May Look AtWhy It Matters

Commission income Average over 12–24 months Shows stable earning patterns

Down payment Savings and source of funds Proves you can handle upfront costs

Debt load Monthly obligations Affects affordability

Reserves Extra cash after closing Helps show financial safety

Lender and Loan Considerations

Choose the right loan type

Different loan types fit different buyers. As an agent, you may want to carefully compare options.

Common choices include:

- Conventional loans – good for buyers with stronger credit and savings

- FHA loans – may help if you want a lower down payment

- VA loans – available if you qualify through military service

- Jumbo loans – useful for higher-priced homes

If your income is variable, ask the lender how they review commission earnings before you apply.

Shop around, even if you know lenders

Your network is helpful, but do not stop at one lender. Compare rates, fees, and approval speed. A lender who understands agent income can make the process easier, but you still want the best deal.

Also ask about:

- Preapproval timelines

- Income documentation rules

- Rate lock options

- Reserve requirements

Conflicts of Interest and Disclosure Obligations

Be transparent from the start

If you are buying a home for yourself, disclosure matters. In many places, you must state that you are a licensed real estate professional. If you are also representing yourself, you may need to sign additional forms.

This is important because it protects you, the seller, and everyone in the transaction.

Check brokerage policy first

Your brokerage may have its own rules about self-purchase. Some require written approval. Others may want a supervising broker involved. Do not assume your license alone gives you full freedom.

Be careful with commissions

If you buy a home through your own deal, commission handling must be clear. Sometimes an agent may receive a reduced commission, credit, or no commission at all, depending on the arrangement and local rules.

The key is to document everything early so there are no surprises later.

Using Industry Advantages Ethically

Use your knowledge, not unfair shortcuts

You can absolutely use your experience to make a smarter purchase. You can study comps, review market timing, and understand how to structure an offer.

But you should not misuse confidential data or pressure others because you “know the business.” Ethical behavior matters just as much as smart strategy.

Work with trusted professionals

Even if you know the process well, it can help to let another agent, attorney, or broker review parts of the deal. A second set of eyes can catch blind spots.

This is especially useful for:

- Contract review

- Inspection issues

- Negotiation strategy

- Closing documents

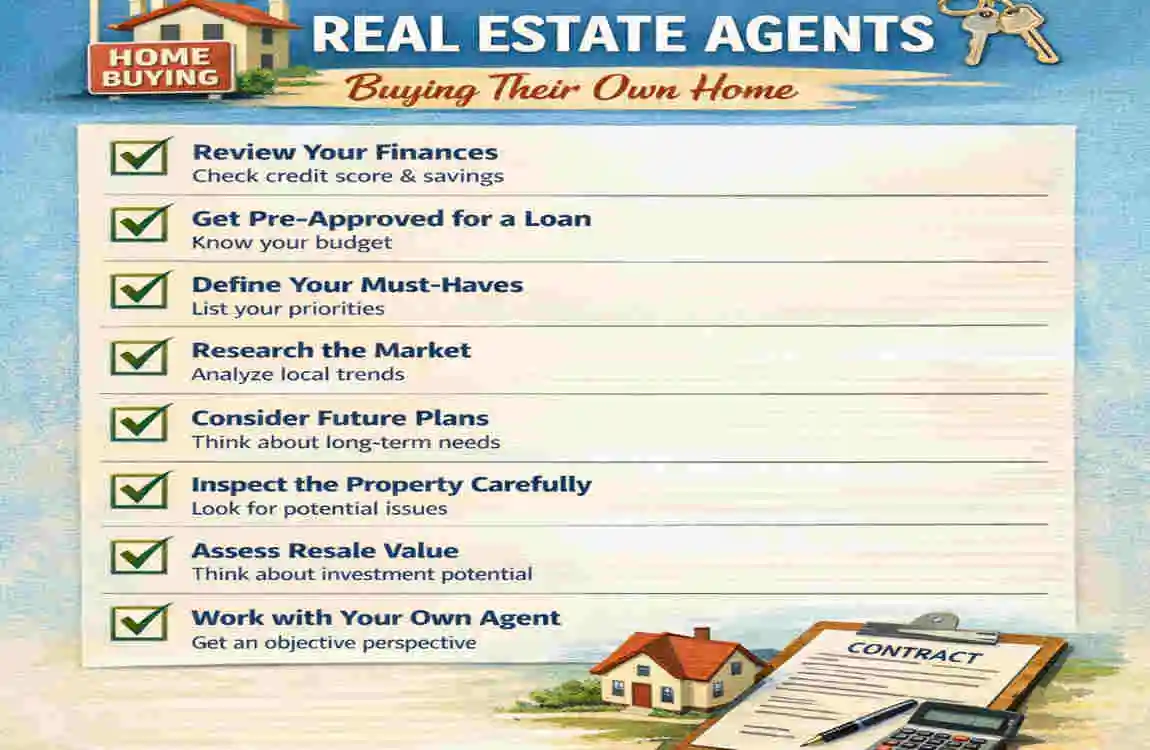

Step-by-Step Purchase Process for Agents

Set your goal

Decide whether this is your primary home, a future rental, or a short-term move. Your goal affects your budget, loan type, and location choice.

Get preapproved

Talk to a lender early and share your income records. Preapproval helps you shop with confidence and avoids delays later.

Decide on representation

Ask yourself whether you will represent yourself or use another agent. In many cases, having another professional represent you can reduce stress and protect your interests.

Search smart

Use MLS filters, local trends, and your professional network. If you find an off-market home, make sure the process still follows all disclosure and agency rules.

Make a clean offer

Keep your offer strong but realistic. Focus on price, contingencies, and earnest money. Do not overcomplicate the deal just because you know how contracts work.

Handle inspections carefully

Choose an inspector who won’t feel pressured to “go easy” on the home. You want honest answers, not comfort.

Stay ready for appraisal issues

If the appraisal comes in low, have a backup plan. You may need to renegotiate, bring extra cash, or adjust terms.

Close with full documentation

Before closing, review all disclosures, commission details, and final numbers. Small mistakes often show up at the end, so stay alert.

Common Pitfalls to Avoid

- Overconfidence: Knowing the market does not mean you know this exact property.

- Fix: Get a second opinion.

- Skipping disclosures: This can create legal and ethical trouble.

- Fix: Complete every required form.

- Using confidential info: That can damage trust and violate rules.

- Fix: Stick to public and permitted data.

- Ignoring closing costs: These can surprise even experienced agents.

- Fix: Ask for a full cost estimate early.

Quick Checklist Before You Buy

- Get preapproved

- Review brokerage rules

- Organize tax and income documents

- Decide if you need separate representation

- Compare loan options

- Schedule inspections

- Review disclosures carefully

- Confirm final closing costs

FAQ

Can real estate agents buy their own homes?

Yes. Agents can buy their own homes, but they must follow disclosure rules, brokerage policies, and local regulations.

Is it easier for agents to get a mortgage?

Sometimes, yes, because agents understand the process and can organize documents well. But lenders still look at income, credit, debt, and savings.

Should I represent myself when buying?

It depends, but having another agent represent you is often safer. It can help reduce blind spots and conflicts.

Can I use my commission toward the purchase?

In some cases, yes, but it depends on the deal structure, lender rules, and brokerage policy. Always confirm this early.

Are off-market deals okay for agents?

Yes, if handled ethically. Just make sure you follow disclosure rules and avoid using private client information.