Imagine standing on a plot of land that you own. It could be a grassy field with a perfect view of the sunset, or a wooded lot nestled in a quiet neighborhood. You can see it clearly in your mind: the front porch, the sprawling living room, the garden out back. You have the land and the dream. But then, the reality of finances hits you. Building a custom home is expensive, and making a massive cash down payment can feel overwhelming.

This brings us to the big question that thousands of landowners ask every year: Can I use my land as collateral to build a house?

If you own land, you are sitting on a valuable asset. Instead of scrambling to save tens of thousands of dollars in cash for a down payment, your land’s value can often do the heavy lifting. It’s a financial strategy that can unlock the door to your custom home much sooner than you think.

What Does It Mean to Use Land as Collateral?

Before we dive into loan applications and interest rates, let’s strip away the banking jargon and look at what this actually means.

When you take out a loan, the bank wants security. They want to know that if life happens and you can’t pay back the money, they won’t be left empty-handed. This security is called collateral. In a traditional mortgage, the house itself is the collateral. But when you are building from scratch, the house doesn’t exist yet.

So, what does the bank look at? They look at the dirt under your feet.

Understanding Land Equity

The magic word here is equity. Equity is simply the difference between what your land is worth and what you owe on it.

- Free and Clear: If you bought a lot for $100,000 and have paid it off in full, you have $100,000 in equity.

- Partial Ownership: If that same lot is worth $100,000, but you still owe $40,000 on a land loan, you have $60,000 in equity.

Lenders view this equity as “skin in the game.” Instead of asking you to bring $50,000 in cash to the closing table, they can use the equity in your land to satisfy the down payment requirement.

Real-World Example: Sarah’s Strategy

Let’s look at a quick example to make this concrete. Meet Sarah. Sarah wants to build a home that will cost $400,000 to construct. Usually, a bank might require a 20% down payment, which is $80,000. That is a lot of cash to have on hand.

However, Sarah owns a plot of land valued at $100,000, and she has paid it off. Because she owns this land “free and clear,” the bank considers the $100,000 land value her down payment. Since her land value ($100,000) exceeds 20% of the total project cost, she could start building without bringing a single dollar of cash to the closing.

Not All Land is Created Equal

While the answer to “can I use my land as collateral to build a house” is generally yes, the type of land matters immensely. Lenders love stability. They prefer land that is immediately ready for building.

Here is a breakdown of how lenders typically view different types of land:

Land TypeDescriptionEligibility for Collateral

Improved Land has access to roads, electricity, water, and sewage. High. This is the gold standard for lenders.

Vacant/Raw Land No utilities or improvements. Just dirt and trees. Medium/Low. Lenders may require you to pay for utility installation first.

Agricultural Land Zoned for farming. Low. Often requires specialized USDA loans rather than standard construction loans.

Unrestricted Land: Remote land with no zoning laws. Variable. Lenders may worry about future property values.

If your land falls into the “Improved” category, you are well-positioned to move forward.

Types of Loans That Accept Land as Collateral

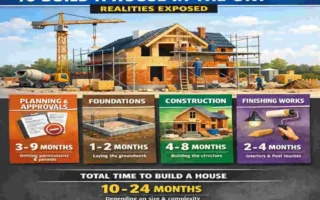

Financing a custom build is different from buying an existing house. You can’t just walk into a bank and ask for a 30-year fixed mortgage because there is no house to mortgage yet. You need a specific construction product.

Fortunately, several loan types allow you to use land as collateral for home building financing.

Construction-to-Permanent Loans C2P

This is often considered the “Holy Grail” of home building finance. Also known as a “Single-Close” loan, this product combines the financing for home construction and the permanent mortgage into a single package.

How it works: You apply once, pay closing costs once, and have one appraisal. During the building phase (usually 12 months), you typically make interest-only payments on the funds you have paid out to the builder. Once the house is finished, the loan automatically converts into a standard mortgage (like a 30-year fixed).

- The Land Benefit: If you already own the land, the value of that land counts toward your down payment. If your land equity covers the required percentage (usually 20-25%), you might not need to put any cash down.

Construction-Only Loans

As the name suggests, this loan covers only the building phase. It is a short-term loan, usually lasting a year or less.

How it works: You take out this loan to pay the builder. Once the house is done, you have to pay the loan back in full. Since most people don’t have that much cash, you typically have to apply for a second loan (a standard mortgage) to pay off the construction loan.

- Why choose this? It sounds more complicated (and it is, because of two sets of closing costs), but it can be good for “flippers” who plan to sell the house immediately, or for people who have a lot of cash now but want to shop for better mortgage rates later.

FHA and VA Construction Loans

If you are worried about high credit score requirements or large down payments, government-backed loans are a lifesaver.

- VA Construction Loans: If you are an eligible veteran, this is arguably the best loan on the market. The VA allows for 0% down payments. If you already own the land, you can use it as collateral to cover closing costs or to reduce the loan amount.

- FHA One-Time Close: Designed for borrowers with lower credit scores (sometimes as low as 620). It allows for a low down payment (3.5%). If your land equity is worth at least 3.5% of the total project, you can start building with very little cash out of pocket.

Home Equity Loans or HELOCs (On Land)

This is a less common route but valid for certain situations. If you own your land outright, you can take out a loan against its value and use the proceeds to fund the start of construction.

However, be careful. Land loans typically have higher interest rates and shorter repayment terms than construction loans. This is usually only a good idea for smaller projects or for financing the build in phases.

Quick Comparison of Loan Options

Loan Type: Land as Collateral?Min. Equity Typically NeededInterest Rate Trend (2026 est.)Best For

C2P (Single Close) Yes 20-25% 6.0% – 7.0% First-time builders seeking simplicity.

Construction-Only Yes 20% 6.5% – 7.5% Investors or those shopping for future rates.

VA Construction Yes 0% (Benefit of VA) 5.5% – 6.5% Eligible Veterans.

FHA Construction Yes 3.5% 5.8% – 6.8% Borrowers with lower credit/savings.

HELOC on Land Yes 30-50% 7.0% – 9.0% (Variable) Small projects or phased builds.

Eligibility Requirements: Do You Qualify?

You might be thinking, “Great, I have land, let’s start digging!” But before the bank hands over a check, they need to verify a few things. Asking “Can I use my land as collateral to build a house?” is the first step; proving you are a safe bet is the second.

Lenders look at the “Three Cs”: Capacity (your income), Credit (your history), and Collateral (the land and the future house).

The Land Criteria

Your land must be “buildable.” Banks don’t want to lend money on a swamp or a cliffside that might slide away.

- Title Search: You must have a “clean title.” This means there are no liens (unpaid debts) attached to the property from previous owners.

- Zoning: The land must be zoned for residential use. If it is zoned for commercial or agricultural use, you may face hurdles.

- Access: The property needs access to a public road. If your driveway crosses a neighbor’s land, you need a legal easement.

- Utilities: Lenders will want proof that you can connect to water (or drill a well), sewer (or install a septic tank), and electricity.

Borrower Requirements

Because construction loans are riskier than buying an existing home (since the home doesn’t exist yet!), the standards are often stricter.

- Credit Score: While FHA allows lower scores, most private lenders require a credit score of 680 to 720 or higher.

- Debt-to-Income (DTI) Ratio: Lenders look at how much debt you have compared to your income. They typically want your total monthly debt payments (including the new mortgage) to be under 43-45% of your gross monthly income.

- Cash Reserves: Even if you use land equity for construction loan down payments, banks often want to see that you have savings left over—usually enough to cover 6 months of mortgage payments. This is your safety net.

The “As-Completed” Appraisal

This is the most confusing part for many people, so let’s simplify it.

When you buy a house, the appraiser looks at what the house is worth today. When you build, the appraiser has to guess what the house will be worth once it is finished.

They look at your blueprints, your materials list (granite vs. laminate, hardwood vs. carpet), and the value of your land. They compare this to other homes in the neighborhood. If your total cost to build is $500,000 but the appraiser says the house is only worth $400,000 in the current market, the bank won’t lend you the full amount.

Pros and Cons of Using Land as Collateral

Using your land to finance your home is a powerful tool, but, like any financial decision, it has two sides. It is important to weigh the benefits against the risks.

The Advantages Why You Should Do It

- Cash Conservation: This is the biggest benefit. By using land collateral home building financing, you keep your cash in the bank. You can use that saved cash for furniture, landscaping, or emergency funds.

- Lower Interest Rates: Secured loans (loans backed by collateral) almost always have lower interest rates than unsecured loans. Because you are putting up a valuable asset, the bank rewards you with a better rate.

- Instant Equity: If you build a home for $300,000 on land worth $100,000, you immediately have a property worth $400,000 (conceptually). You aren’t “underwater” on the loan.

- One Set of Closing Costs: If you use a Construction-to-Permanent loan, you avoid paying double fees.

The Disadvantages What to Watch Out For

- Risk of Loss: This is the scary part. If you default on the loan, you don’t just lose the house; you lose the land too. Even if the land has been in your family for generations, it is now tied to the mortgage.

- Complex Appraisals: As mentioned earlier, if the “future value” of your home doesn’t appraise high enough, you might have to bring cash to the table anyway to make up the difference.

- Strict Timelines: Construction loans have deadlines. If your builder takes too long and goes past the 12-month window, you might have to pay extension fees or refinance the loan, both of which cost money.

Step-by-Step Guide: How to Finance Your Build

Ready to turn that dirt into a driveway? Here is the roadmap. If you are wondering, “Can I use my land as collateral to build a house?” here is exactly how you execute that plan.

Determine Your Land’s Value

You need to know how much equity you actually have. You can look at recent sales of similar lots in your area, or check sites like Zillow Land for estimates, but the best method is to hire a professional appraiser. This gives you a hard number to present to the bank.

Shop for Lenders

Not all banks offer construction loans. Big national banks sometimes do, but often your best bet is a local credit union or a regional bank. They know the local market better. Ask them specifically about “Single-Close Construction Loans using land equity.”

Choose a Licensed Builder

This is critical. Banks generally will not let you build the house yourself (unless you are a licensed professional builder). You must hire a licensed, insured General Contractor. The bank will vet the builder to make sure they are financially stable.

Finalize Plans and Budget

Work with your architect and builder to create the blueprints and a detailed cost breakdown. The bank needs to know every penny—from the foundation concrete to the kitchen faucet.

The Appraisal and Underwriting

The bank will order an “As-Completed” appraisal. They will review your credit, the builder’s credentials, and the land title. Once everything clears, you sign the closing documents.

The “Draw” Process

Unlike a regular mortgage, which pays out in a lump sum, a construction loan pays out in “draws.”

- The builder completes the foundation.

- The bank sends an inspector to verify it.

- The bank releases funds to pay for the foundation. This continues through framing, roofing, and finishing. You usually only pay interest on the amount that has been paid out so far.

Conversion

Once the house is done and a Certificate of Occupancy is issued, the loan converts to your permanent mortgage. You start making regular monthly payments of principal and interest.

Costs, Fees, and Budgeting Tips

Building a house is notorious for going over budget. When using land as collateral, be aware of the specific costs involved so you aren’t blindsided.

The “Soft Costs”

People remember the cost of lumber and labor, but they forget the “soft costs.”

- Appraisal Fees: Construction appraisals are more expensive than standard ones, often running $500 to $800.

- Inspection Fees: Each time the bank releases funds (a draw), it sends an inspector. This can cost $150-$200 per visit.

- Title Insurance: You will need to re-insure the land’s title to cover the lender’s interest.

- Closing Costs: Expect to pay 2% to 5% of the total loan amount in closing fees.

Sample Budget for a $400,000 Project

Expense ItemEstimated Cost

Construction Costs (Hard Costs) $320,000

Permits & Fees $10,000

Architect/Design Fees $15,000

Site Prep (Grading, Utilities) $25,000

Loan Closing Costs & Reserves $15,000

Contingency Fund (10%) $15,000

TOTAL $400,000

If your land is worth $100,000, you have $100,000 in equity. Since 20% of $400,000 is $80,000, your land equity covers the down payment entirely, with $20,000 of “extra” equity to spare!

Savings Tip

Shop for your interest rate! A difference of just 0.5% in your interest rate can save you nearly $100 a month on your mortgage payment. That adds up to $36,000 over a 30-year loan.

Risks and How to Mitigate Them

We touched on the cons, but let’s talk about specific risks and how to protect yourself.

The Risk of Cost Overruns

What if lumber prices spike? What if you hit rock while digging the foundation?

- The Fix: Always, always have a Contingency Fund. Set aside 10% to 15% of the total budget in cash (or built into the loan) for surprises. If you don’t use it, great! But if you need it, it saves the project.

The Risk of Builder Issues

What if the builder goes bankrupt halfway through?

- The Fix: Ensure your builder is bonded and insured. Also, consider “Completion Insurance.” Check references thoroughly. Don’t just look at online photos; call previous clients and ask if the builder stayed on budget and on time.

The Risk of Low Appraisal

What if the house appraises for less than it costs to build?

- The Fix: Keep your design practical. Highly unusual homes (like a dome home or a castle replica) are hard to appraise. Sticking to styles common in your area ensures the value holds up.

Alternatives If Land Won’t Work

Sometimes, the answer to “Can I use my land as collateral to build a house?” is “No.” The land may have environmental issues, or you may still owe more than it’s worth. Don’t panic; you have alternatives.

Cash-Out Refinance If you own another home

If you currently own a home with equity, you can do a cash-out refinance on your current home to get the cash needed for the down payment on the new build.

Personal Loans

For smaller amounts (like $20,000 to install utilities and make the land eligible), a personal loan can bridge the gap. Rates are higher, but it can solve immediate problems.

Seller Financing

If you are buying the land and want to build a home, ask the land seller if they will finance the land for you. Sometimes, private sellers are more flexible than banks when it comes to down payments and terms.

Frequently Asked Questions (FAQ)

Here are the most common questions we hear from landowners looking to build.

Can I use my land as collateral to build a house if it’s not paid off?

Yes, but it’s trickier. You don’t need to own the land 100% free and clear. However, you need enough equity to meet the lender’s requirements. If the land is worth $100k and you owe $20k, you have $80k in equity. The bank will use part of the new loan to pay off the remaining $20k in land debt, and the rest of the equity will count as your down payment.

What if my land is in a rural area?

USDA loans are your best friend here. The USDA offers construction loans specifically for rural areas. They often require $0 down and have very favorable terms. Check the USDA property eligibility map to see if your land qualifies.

How much equity do I need to start building?

Typically 20% to 25%. Most conventional lenders require a loan-to-value (LTV) ratio of 75% or 80%. This means your equity (land value) plus any cash you put down needs to equal 20-25% of the total project value.

Is it better to use raw land or improved land?

Improved land is much easier to finance. If your land is “raw” (no sewer, water, or electricity), the bank views it as a higher risk because development costs can spiral out of control. You may need to pay to install utilities before the bank will approve the main construction loan.

Are there tax implications?

Generally, yes—good ones. During construction, the interest you pay on the loan is often tax-deductible, similar to mortgage interest. However, always consult a CPA to confirm your specific situation.