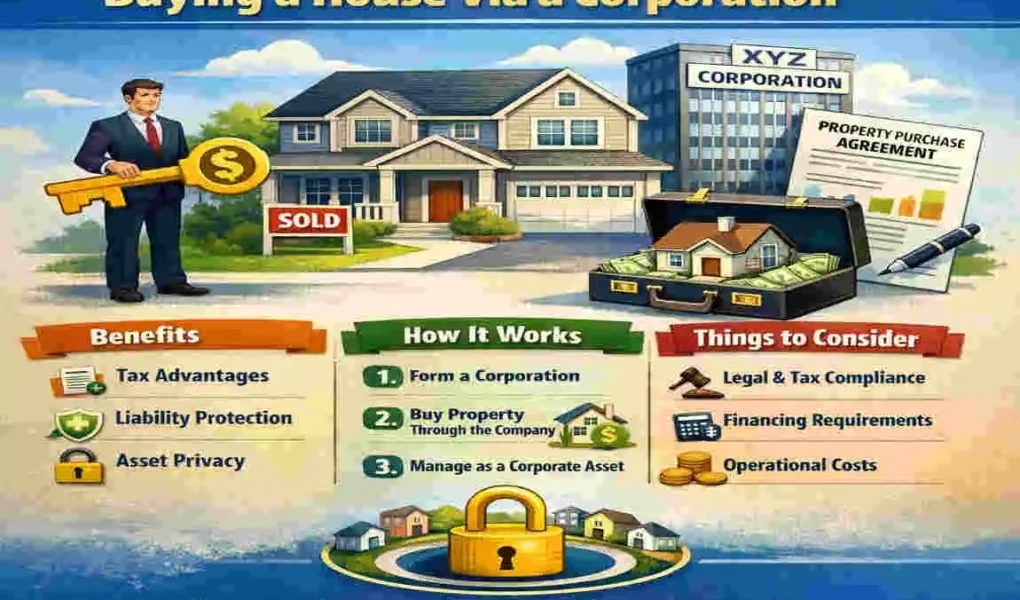

If you are looking for a smarter way to grow your real estate portfolio, how to buy a house under a corporation is one of the first questions worth asking. The idea sounds simple at first: instead of buying property in your personal name, you buy it through a company. But once you look closer, you’ll see that this choice affects your taxes, financing, liability, paperwork, and long-term planning.

If you’re wondering how to buy a house under a corporation, this article breaks it down in plain language. We’ll walk through the full process from setting up the company to closing on the property and handling the tax side after the purchase. You’ll also learn when corporate ownership makes sense, when it does not, and what mistakes investors often make when they rush into it.

In 2026, more investors are paying attention to corporate ownership because markets remain uncertain in many places. Interest rates remain a concern, property prices are uneven, and many buyers want better protection for their personal assets. A corporation can offer that kind of separation, but it is not a magic solution. It can help in the right situation, yet it can also add cost, complexity, and extra obligations.

Why Use a Corporation to Buy Property?

There are several reasons people choose to buy a house through a corporation rather than in their own name. For many investors, the biggest reason is simple: they want to keep personal and business risk separate.

Liability protection and personal asset separation

One of the biggest benefits of corporate ownership is liability protection. If a company owns the property and something goes wrong, the claim is usually tied to the company, not your personal bank account or home. That separation can give you peace of mind, especially if you own rental property.

For example, if a tenant is injured on the property and sues, the corporation serves as the first line of defense. That does not mean you are immune from all risk, but it can reduce the extent to which your personal assets are directly exposed. For many investors, that is the main reason they start researching how to buy a house under a corporation.

Better structure for multiple owners

Corporate ownership can also make life easier when more than one person is involved. Instead of managing a property through informal agreements, you can define ownership shares, voting rights, profit distribution, and exit rules within the company’s structure.

This is especially helpful for family investing, business partnerships, and joint ventures. When people ask about the best steps to buy property through LLC, they are often trying to solve exactly this problem: how to keep ownership organized and avoid confusion later.

More flexible estate and succession planning

A corporation can also make long-term planning easier. Instead of transferring a property directly from one person to another, you may be able to transfer shares in the company. That can be a smoother way to pass assets to heirs, partners, or successors.

This matters if you want your real estate portfolio to survive beyond one generation. If you are thinking far ahead, buying a house under a corporation may be part of a broader estate strategy rather than just a tax move.

Tax planning possibilities

Many people are drawn to corporate ownership because they hope to save on taxes. That can happen in some situations, but this area needs careful planning. The real benefit often comes from deferral, not necessarily from paying less forever.

For example, in some jurisdictions, corporate structures may allow investors to retain funds within the company for reinvestment. That can help if you plan to buy more properties or expand your portfolio. In other cases, the tax treatment can be similar to that of personal ownership. Still, the timing of tax payments may differ.

When it may not be the right choice

Corporate ownership is not automatically better.

If you plan to live in the home as your primary residence, corporate ownership often becomes less attractive. You may lose certain homeowner tax benefits, face higher financing costs, and add more legal work than necessary. For many everyday buyers, buying personally is still simpler and cheaper.

That is why how to buy a house under a corporation should be treated as a strategic decision, not a default one.

Personal vs. Corporate Ownership at a Glance

AspectPersonal OwnershipCorporate Ownership

Liability Full personal exposure Risk is generally separated from personal assets

Taxes Simpler for many homeowners Can support deferral and business planning

Mortgages Often easier to obtain May require commercial-style approval

Administration Less paperwork More records and compliance

Best use case Primary home, simple ownership Rentals, partnerships, portfolio growth

If you are building a real estate business, this table shows why many people research how to buy a house under a corporation before they buy their second or third property.

Types of Corporations for Real Estate

Before you move forward, you need to understand that “corporation” does not mean only one thing. The right structure depends on where you live, how you invest, and whether you are buying alone or with others.

LLC: Flexible and popular for investors

In the United States, the LLC is one of the most common choices for real estate investors. It is popular because it is flexible and can be easier to manage than a traditional corporation.

An LLC often works well for small- and mid-sized investors because it can separate the property from your personal finances while still providing a straightforward ownership structure. Many people exploring steps to buy property through LLC choose this structure first because it is familiar and relatively adaptable.

An LLC may also be easier to use when you want pass-through style tax treatment, depending on how it is set up and how your jurisdiction treats it.

C-Corp: Better for larger growth plans

A C-Corp can make sense in some growth-focused strategies, especially when a company is designed to scale. Some investors prefer this structure when they want a more formal corporate setup and expect to raise capital, hold multiple assets, or build a larger enterprise.

The downside is that a C-Corp can lead to more complex tax outcomes. In some situations, profits may be taxed at the corporate level and then taxed again when distributed. That is why C-Corps are not always the first choice for smaller real estate investors.

Still, when people ask how to buy a house under a corporation, the C-Corp often comes up because it sounds strong, structured, and businesslike. That is true, but it is only the right fit in certain scenarios.

S-Corp: Useful in specific situations, but limited

An S-Corp can be useful in some business setups. Still, it is usually not the simplest choice for directly holding rental property. Ownership restrictions and tax rules can limit flexibility.

Some investors consider an S-Corp for certain operating activities. Still, for actual property holding, the structure often needs careful review. It is important not to assume that every business entity is equally suited for owning real estate.

Ltd. companies in Canada and the UK

Outside the United States, many investors use a limited company or Ltd. company instead. In places like Canada and the UK, this is often the more common corporate route for property ownership.

If you are buying through a limited company, the registration process usually involves forming the company, naming directors and shareholders, and completing local business filings. In the UK, this is typically done through the appropriate company registration system. At the same time, in Canada you work through the relevant provincial or federal process.

This is one reason the phrase how to buy a house under a corporation can mean different things depending on where you live. The legal structure changes, even if the strategy feels similar.

Entity Comparison Table

Entity TypeTax TreatmentBest For

LLC Often flexible and pass-through friendly Small to medium investors

C-Corp Corporate-level taxation structure Larger portfolios or growth plans

S-Corp Pass-through style with restrictions Specific business setups

Ltd. Company Local corporate tax treatment Investors in the UK, Canada, and similar markets

If you are unsure which entity fits your goal, stop and ask a professional before you move ahead. The best way to learn how to buy a house through a corporation is to align the entity with your actual investment plan.

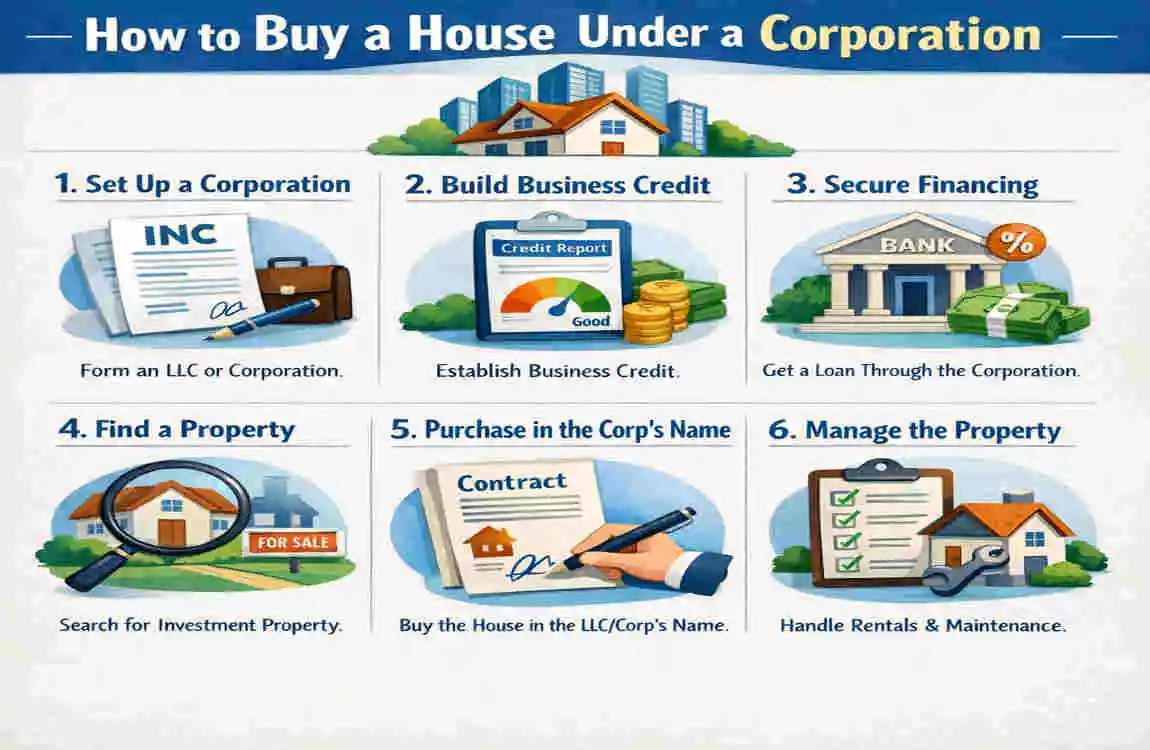

Step-by-Step Process: How to Buy a House Under a Corporation

Now let’s get practical. This is the part most people want first. If you want to know how to buy a house under a corporation in the real world, the process usually follows a series of clear steps.

Form the corporation

The first step is to create the company that will hold the property.

That means choosing a name, registering the entity with the proper government office, and deciding who the directors, shareholders, or members will be. You also need to ensure the company is legally active and ready to enter into contracts.

This step matters because the corporation must exist before it can buy anything. You cannot usually close the company under its name if it is not properly formed. If you are serious about buying a house through a corporation, this is where the plan begins.

You should also carefully consider the ownership structure at this stage. Who will own the shares? Will there be one owner or multiple owners? Will family members be involved? These choices affect taxes, control, and succession later on.

Get the tax ID or business number

Once the company exists, you usually need a tax ID, business number, or equivalent registration number. Banks, lenders, lawyers, and tax authorities often require this before they can move forward.

You will likely need this number to:

- Open a business bank account

- Apply for financing

- Register for taxes

- Sign closing documents

- Keep proper corporate records

This is a small step on paper, but it is a major part of buying a house under a corporation because it allows the company to function as a real legal buyer.

Open a business bank account

Your corporation should have its own bank account. Do not mix your personal money with the company’s money.

This is one of the simplest but most important habits you can build. It keeps bookkeeping clean, helps with taxes, and supports the legal separation between you and the company. If you blend funds, you create confusion, and confusion can become a problem during an audit, a dispute, or a lawsuit.

As you continue learning how to buy a house under a corporation, remember this rule: the company should act like a real business, not like a personal side wallet.

rrange financing early

Financing is one of the biggest differences between personal and corporate buying.

When a corporation buys property, lenders often scrutinize the deal more closely. They may ask for stronger documentation, a larger down payment, and a personal guarantee from the owner. In many cases, the loan behaves more like a business loan than a standard homeowner mortgage.

That is why this part of buying a house under a corporation can feel harder than buying personally. You may need to show:

- Strong income or company financials

- A clear business plan

- Rental projections

- Credit history of the owners

- Proof of down payment funds

Some lenders are comfortable working with new companies, while others want a track record. If your corporation is new, expect more questions and more paperwork.

Search for the right property

Not every property is ideal for corporate ownership. This is where your strategy matters.

If the home is meant to be an investment property, rental unit, or part of a portfolio, corporate ownership may be a strong fit. If it is a primary residence, the fit may be weaker.

When you shop for the property, make sure the offer is written correctly so the corporation is the buyer. Your purchase agreement should name the company, not you personally, if that is the intended ownership structure.

This is one of the most important details for buying a house under a corporation. A small paperwork mistake can create major delays.

Submit the offer in the corporate name

When you make the offer, the legal buyer should be the corporation.

Sometimes an investor signs personally at first and then assigns the purchase to the corporation later. That can work in some cases, but it must be handled carefully. In many deals, it is cleaner to make sure the corporation is named correctly from the start.

You should also make sure the deposit comes from the corporate bank account or another approved source. That keeps the transaction consistent and easier to document.

Complete due diligence

Due diligence means checking everything before closing. This includes title review, property condition, zoning, tax obligations, and any legal issues associated with the property.

At this stage, your lawyer or solicitor should review the purchase documents and make sure the corporation is listed properly. They should also check whether the title transfer, tax filings, and any corporate filings are complete.

If you are serious about how to buy a house under a corporation, do not rush this step. Due diligence can save you from expensive problems later.

Close the deal

Closing is the process by which ownership officially transfers to the corporation.

The property title will usually be recorded in the company’s name, and the final documents will confirm that the corporation is now the legal owner. After closing, you should carefully store all paperwork, including the purchase contract, title documents, financing records, and corporate resolutions.

This is the point where the strategy becomes real. You have moved from planning how to buy a house under a corporation to actually owning property through a separate legal entity.

Set up post-purchase records

After closing, the work is not done. You still need to keep the company in good standing.

That usually means:

- Keeping books and records updated

- Filing taxes on time

- Maintaining the corporate registration

- Renewing licenses if needed

- Tracking rental income and expenses

Good recordkeeping makes the company easier to manage and easier to defend if questions ever arise.

Quick checklist for corporate buyers

- Form the entity

- Get the tax ID

- Open the bank account

- Line up financing

- Make the offer in the company name

- Complete due diligence

- Close correctly

- Keep ongoing records

This checklist is a simple guide to buying a house through a corporation, but it covers the essential steps.

Tax Implications of Buying Through a Corporation

Tax is one of the biggest reasons people explore buying a house through a corporation. But it is also one of the most misunderstood parts.

Rental income and business taxation

When a corporation owns a rental property, the rental income is usually treated as company income. That means the corporation reports its earnings and pays tax under the rules of that jurisdiction.

This can be helpful if you want to retain profits and reinvest them. Instead of taking all the money out right away, you may be able to keep the cash inside the business and use it for repairs, future purchases, or reserve funds.

This is one of the strongest reasons investors consider buying a house through a corporation rather than buying everything personally.

Capital gains treatment

If the property grows in value and is later sold, capital gains rules may apply. In some structures, gains inside a corporation are taxed differently than gains in personal ownership.

However, this is not automatically better or worse. It depends on where you live, how the corporation is structured, and whether you plan to withdraw the money later. Sometimes the tax is delayed, not erased.

That is why how to buy a house under a corporation should be viewed as a planning decision, not just a tax-saving trick.

Dividends, salaries, and withdrawals

When money leaves the corporation, it usually has to be paid out in an approved way. That may mean dividends, salary, owner’s draw, or another tax-recognized method.

This is a key point because the company may pay tax first and you may also pay tax later when you take the money personally. The goal is to understand the full chain, not just the first layer.

If you ask experts about how to buy a house under a corporation, they will often remind you that the real issue is not just how the property is taxed. It is also how the cash leaves the company.

Principal residence concerns

Buying your own home through a corporation usually makes less sense than buying a rental property through one. In many systems, a personal primary residence can qualify for tax benefits that corporate-owned property cannot.

That is why the house you live in is often treated differently from a house you rent out. The corporate route may remove valuable personal-home advantages. If the property is your family home, be cautious before deciding how to buy a house under a corporation.

Corporate tax planning table

Tax EventPersonal OwnershipCorporate Ownership

Rental income Reported personally Reported by the company

Reinvestment Limited by personal cash flow Easier to retain earnings in the company

Capital gains Taxed under personal rules Taxed under corporate rules

Cash withdrawal Direct access Usually taxed again when distributed

Primary residence benefit May be available Often not available

Why tax advice matters here

There is no one-size-fits-all answer. A structure that works well for one investor can be a poor choice for another. Your salary, other income, family setup, and long-term goals all matter.

So if you are serious about buying a house through a corporation, make sure a tax professional reviews the deal before you close. That advice may save you far more than it costs.

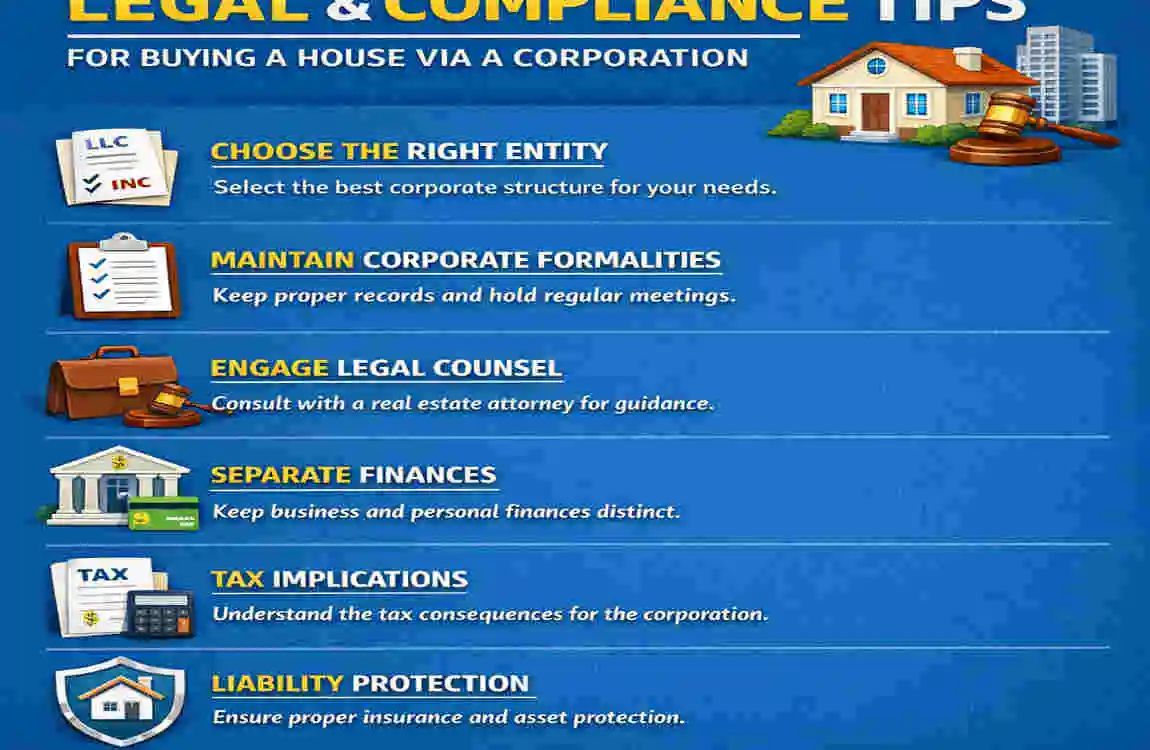

Legal and Compliance Tips You Should Not Ignore

Many investors focus only on the purchase itself. But if you want to make how to buy a house under a corporation work smoothly over time, you also need strong legal habits.

Create a proper ownership agreement

If more than one person owns the company, put the terms in writing. A shareholder agreement, operating agreement, or similar document can explain who owns what, who makes decisions, how profits are split, and what happens if someone wants out.

Without this, small disagreements can turn into major problems. A clear agreement protects everyone involved and makes the business more professional.

Keep the company separate from your personal life

The corporation should behave like a real company.

That means separate bank accounts, separate books, separate contracts, and separate records. When the company pays for property costs, those payments should be documented. When you put money in, it should be recorded properly too.

This separation is one of the core reasons people choose how to buy a house under a corporation in the first place. If you ignore the separation, you weaken the benefits.

Review insurance carefully

Insurance should match the propertyis ownership. If the company owns the property, the policy should usually reflect that. You may also need extra coverage for rental risk, liability, or vacancy periods.

Do not assume your old personal policy will be enough. Make sure the insurer understands the ownership structure and the property’s use.

Update your will and estate plan

If the corporation is part of your long-term wealth plan, your will and estate documents should reflect that.

Shares in the corporation may need to pass to heirs, trust structures, or successors. If your estate plan does not match your business structure, your family may face confusion later.

That is why how to buy a house under a corporation is often only one piece of a larger planning puzzle.

Watch for transfer taxes and filing requirements

Depending on the location, moving property into or out of a corporation can trigger taxes, fees, or filing obligations. If you buy personally and transfer later, you may create extra cost.

So, if you already know you want the company to own the property, it is usually better to set that up correctly from the start rather than clean up a transfer later.

Common Pitfalls When Buying Under a Corporation

A lot of mistakes happen because people rush. They hear about the benefits and move too fast. If you want to master how to buy a house under a corporation, you should also understand where investors usually go wrong.

Financing gets harder than expected

One of the most common issues is financing. Many lenders treat corporate purchases more cautiously, especially for new companies.

You may face higher rates, more documentation, and personal guarantees. Some buyers are surprised by this because they expected the corporation to make the deal cleaner, not more difficult.

Fix: Talk to lenders early and get pre-approval before making an offer.

Taxes become more complicated

Another common problem is assuming that corporate ownership automatically lowers taxes.

That is not always true. In some cases, you simply change the timing of the tax or the way it is collected. If you withdraw money from the company, you may face an additional layer of tax.

Fix: Get a tax plan before closing, not after.

Investors use the wrong property type

Many people think every house should go under a corporation. That is not the case.

A primary residence may be better held personally, while a rental or investment property may be better in a company. The right answer depends on your goals.

Fix: Match the entity to the purpose of the property.

Records are poor from day one

If the books are messy, the structure becomes harder to defend and harder to manage.

Fix: Set up bookkeeping, separate accounts, and filing systems immediately.

Owners mix personal and company spending

This is a classic mistake. If you pay property bills personally and never document them, or if you use company money for unrelated personal expenses, you create confusion.

Fix: Keep everything documented and separated.

Pitfalls and practical fixes

- Weak financing plan → Get lender feedback before offering

- Bad tax assumptions → Review the full tax picture with a professional

- Wrong entity choice → Choose the structure based on the property’s purpose

- Poor records → Use separate accounts and bookkeeping software

- Personal/company mixing → Treat the corporation like a real business

If you avoid these mistakes, how to buy a house under a corporation becomes much more manageable.

When Corporate Ownership Makes the Most Sense

Not every buyer needs a corporation, but some situations are especially suitable.

You own rental property

If your goal is to hold rentals, collect income, and expand your portfolio, corporate ownership often makes more sense than personal ownership. The company can act as the home base for your real estate business.

You invest with partners

If more than one person is involved, a corporation can give you a cleaner way to divide ownership and responsibilities. That can reduce friction and make the deal easier to manage.

You want to build a portfolio

If you plan to buy multiple properties over time, corporate ownership may help you organize the business side of investing. It may also help with financing strategy, bookkeeping, and long-term planning.

You are thinking about succession

If you want to pass property to family members or future partners, shares in a company may be easier to manage than a direct property transfer.

In all these cases, buying a house through a corporation can be part of a broader strategy rather than a one-off decision.

FAQs About How to Buy a House Under a Corporation

Is it better than buying in my own name?

Not always. If you are buying a primary residence, personal ownership is often simpler and more tax-friendly. If you are buying rentals or building a portfolio, corporate ownership may be more useful.

Can I finance the purchase personally even if the property is in a corporation?

In many cases, yes. Lenders may ask for a personal guarantee, especially if the corporation is new. That means the company owns the home, but you may still be personally responsible for the debt if the deal goes bad.

How much does it cost to set up?

The cost varies depending on your location and the structure’s complexity. You may have formation fees, legal fees, accounting costs, and ongoing compliance expenses. A simple setup can be affordable, but a well-planned setup is worth more than a cheap one.

Can I transfer a home I already own into a corporation?

Sometimes, but it may create tax, legal, and financing consequences. A transfer can trigger fees or taxes, so it should be reviewed carefully before you do it.

Is it a good idea for a primary home?

Usually not. For many buyers, a primary residence is better held personally because of potential tax advantages and simpler financing.

Do I need a lawyer or accountant?

Yes, in most cases. A lawyer can help with title, entity structure, and contracts, while an accountant can help with tax planning and reporting. If you are learning how to buy a house under a corporation, professional advice is not optional in serious deals.

What is the safest first step?

The safest first step is to decide whether the property truly belongs in a corporation at all. Then speak with a lender, lawyer, and tax advisor before you make an offer.