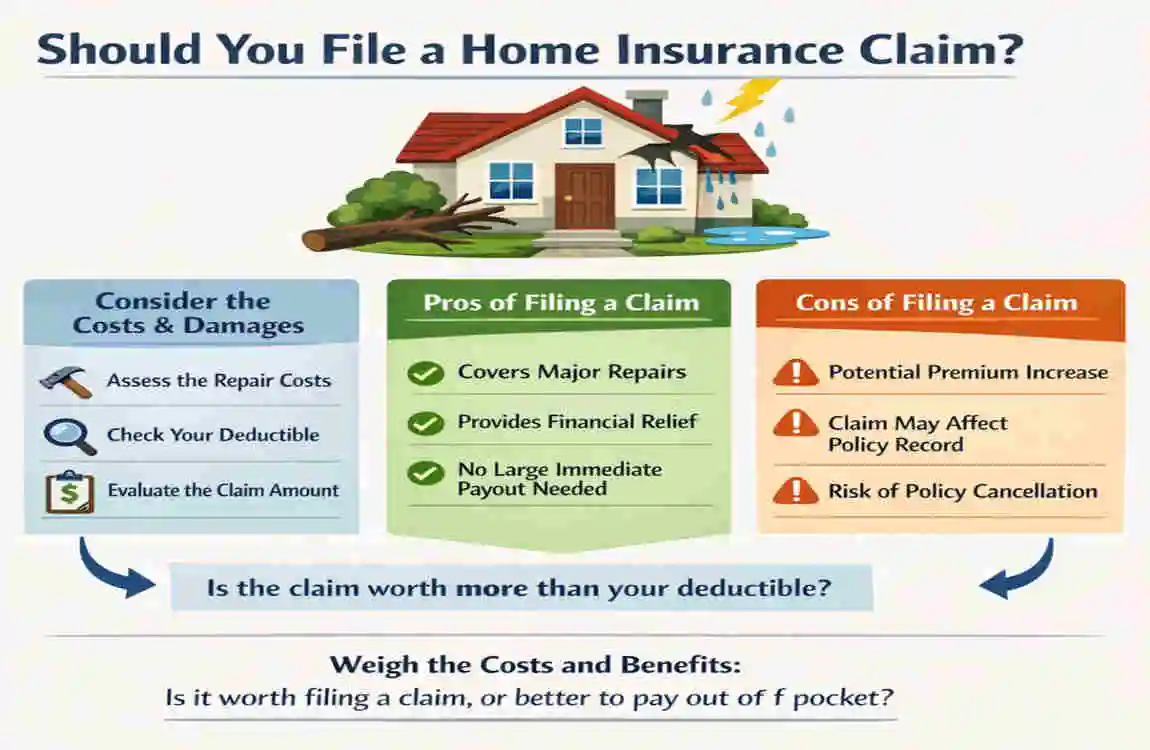

Homeowners often pause before filing a claim because the decision can affect more than just today’s repair bill. It can also influence your future premium, your claim history, and even how your insurer views your risk. That is why many people ask a very practical question: is it worth making a claim on home insurance?

If your home has been damaged, suffered theft, or been involved in an accident, you may feel pressure to act quickly. But before you call your insurer, it helps to slow down and look at the full picture. You want to understand the size of the damage, what your policy covers, and whether paying out of pocket might be the smarter move.

Understanding Home Insurance Claims

What Is a Home Insurance Claim?

A home insurance claim is a request you make to your insurance company asking them to pay for a covered loss. That loss may be damage to your home, damage to personal belongings, or even liability costs if someone is injured on your property.

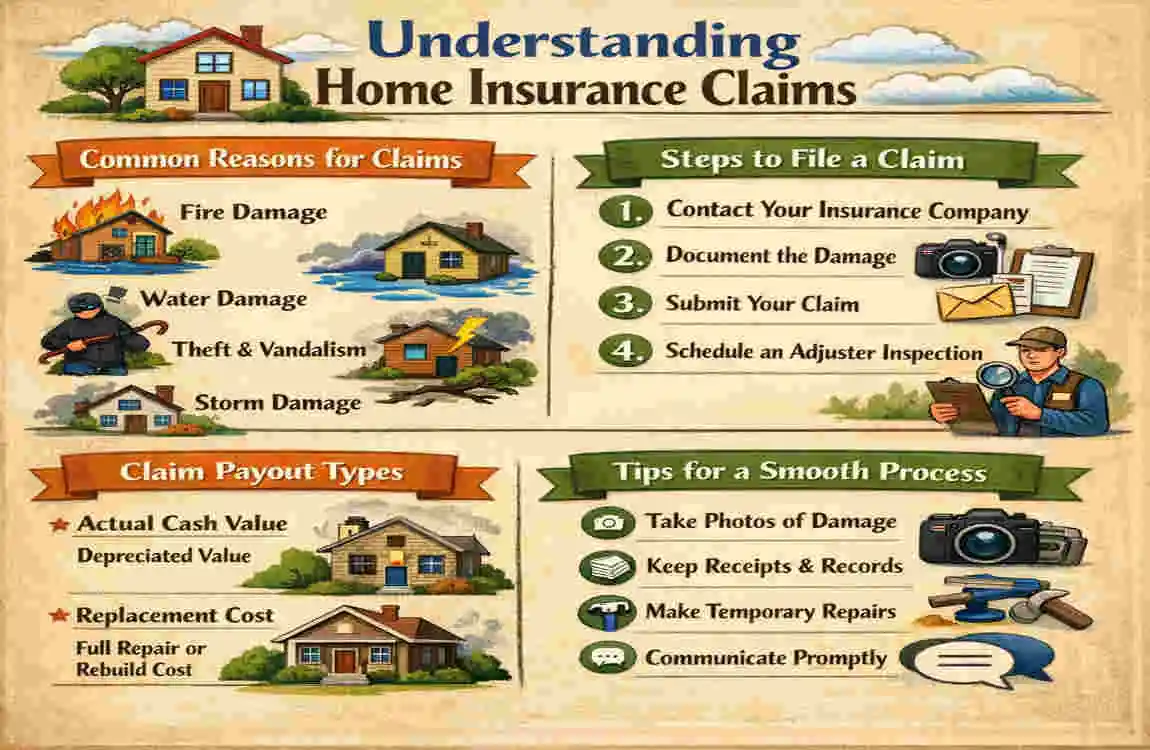

The process usually starts when you report the damage. Then the insurer reviews the situation, checks your policy, and decides whether the loss is covered. If it is, they estimate the payout after subtracting your deductible.

People file claims for many reasons. A storm may tear off part of your roof. A pipe may burst, flooding a room. A thief may steal valuable items. Or a visitor may slip and get hurt, which can lead to a liability claim.

Events Typically Covered

Most home insurance coverage is designed to help with sudden and accidental damage. Common covered events often include:

- Fire damage

- Water damage from a burst pipe or sudden leak

- Storm damage from wind, hail, or falling objects

- Theft or vandalism

- Liability claims if someone is injured on your property

These are the kinds of losses that can become expensive very quickly. A single event can result in thousands of dollars in repair costs, replacement costs, or legal expenses.

What Home Insurance Usually Doesn’t Cover

Not every problem in a home qualifies for a payout. Standard policies often exclude:

- Flooding from outside water

- Earthquakes

- Wear and tear

- Damage caused by neglect or poor maintenance

This matters because many homeowners assume any damage should be covered. In reality, if the issue developed slowly or came from a maintenance problem, your insurer may deny the claim.

That is why reading your policy carefully is so important. A homeowners insurance claim only helps when the loss falls within the policy’s terms.

Is It Worth Claiming on Home Insurance? Key Factors to Consider

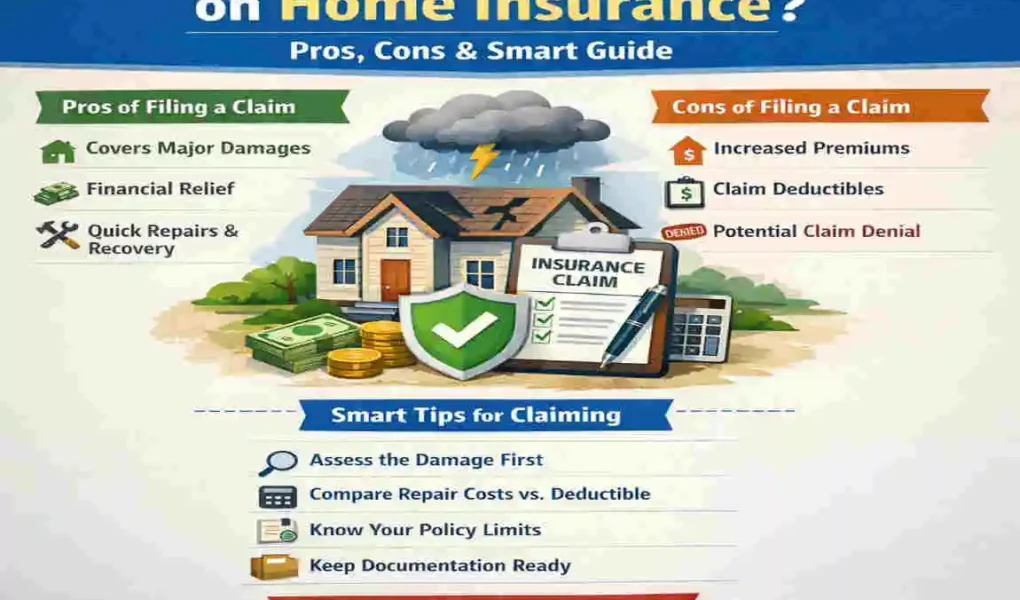

Compare Repair Costs vs. Deductible

Your deductible is the amount you pay before insurance starts covering the rest. If your deductible is $1,000 and your repair cost is $1,300, your insurer may only pay $300. In that case, filing a claim may not feel very helpful.

This is why people often ask about home insurance deductible vs repair cost. If the repair is only slightly above your deductible, the claim may not be worth the potential premium increase later.

A simple rule of thumb is this: if the repair is small enough that you can handle it comfortably, paying yourself may be the better choice. If the damage is far above the deductible, the claim becomes more attractive.

Claim History and Future Premium Increases

Insurance companies pay close attention to how often you file claims. One claim may not matter much, but repeated claims can raise questions about your home’s risk level.

That is one reason people worry about does home insurance go up after a claim. In many cases, yes, it can. Even if the insurer pays the claim, they may raise your premium at renewal because they now see your home as more expensive to insure.

Frequent claims can also make you appear to be a higher-risk customer. This may affect your rate, your discounts, or even your ability to stay with the same insurer.

Severity of Property Damage

The bigger the damage, the more likely a claim makes sense. A broken tile or a small stain is very different from a roof collapse or a major fire.

When the damage threatens the structure of your home or makes the property unsafe, the decision becomes easier. Emergency repairs are often too expensive to handle on your own. In those cases, the claim may protect your finances and help you recover faster.

Policy Limits and Coverage Terms

Even if the damage is serious, your policy may still have limits. A policy limit is the most the insurer will pay for a covered loss. If your home repair exceeds that amount, you may need to cover the rest yourself.

You also need to check exclusions, special limits, and endorsements. Some items, like jewelry or collectibles, may have lower payout caps unless they were specifically scheduled.

Quick Comparison Table: Claim or Pay Out of Pocket?

Situation Filing a Claim May Help Paying Yourself May Be Better

Repair cost is far above deductible Yes No

Damage is small and manageable No Yes

You already filed claims recently Maybe not Yes

Damage is major or urgent Yes No

Loss is not covered by policy No Yes

This table is not a rule for every case, but it gives you a quick way to think through the decision.

Pros of Claiming on Home Insurance

Benefits of Filing a Claim

A home damage claim can be a lifesaver when the bill is too large to pay on your own. Here are the biggest benefits.

Financial Relief

The most obvious benefit is money. If a storm tears up your roof or a kitchen fire causes serious damage, repairs can cost thousands. A claim can reduce that burden and protect your savings.

This is especially helpful when the damage affects something important, such as your home’s structure, heating system, or electrical system. In those situations, waiting too long can make the problem worse.

Protection After Major Disasters

Big events can leave you with no safe or usable living space. Fires, severe storms, and structural damage are not small problems. They often require fast action and expensive repairs.

In these cases, your insurance payout can help you rebuild, replace damaged items, and restore the home more quickly. That support can make a stressful situation much easier to manage.

Liability Coverage Help

Sometimes a claim is not about the house itself. It may be about someone getting hurt on your property. If a guest slips on icy steps or a neighbor’s property gets damaged by something from your home, liability coverage may help.

This type of claim matters because legal and medical costs can grow fast. A single accident can become a major financial problem without the right coverage.

Peace of Mind

Money is not the only issue. When your home is damaged, peace of mind matters too. Knowing that insurance may help can reduce stress and help you focus on recovery.

For many homeowners, that comfort is worth a lot. It can make the difference between feeling stuck and moving forward with confidence.

Cons of Claiming on Home Insurance

Downsides Homeowners Should Know

Even when a claim seems helpful, there are real downsides. Understanding them will help you make a smarter decision.

Higher Insurance Premiums

One of the biggest concerns is a homeowners insurance premium increase after a claim. Your insurer may adjust your rate when they renew your policy, especially if the claim was large or avoidable.

That means a claim that seems helpful now may lead to higher costs for years to come. Over time, those extra premium payments can reduce or even erase the benefit of the claim.

Risk of Non-Renewal

Some homeowners do not think about renewal until it becomes a problem. But if you make several claims in a short period, your insurer may decide not to renew your policy.

This is especially important if the claims suggest recurring issues, such as water damage or theft. Insurers want predictable risk, and frequent claims can make your home look less stable to cover.

Claims Stay on Insurance Records

A claim is not forgotten after the repair is done. It stays on your insurance record for a period of time, and future insurers may see it when you apply for new coverage.

That can affect the price you are offered later. Even a single claim can matter if it was expensive or happened recently.

Small Claims May Not Be Worth It

This is where many homeowners make the wrong call. If the repair cost is close to the deductible, the claim may only bring a small payout. In that case, the future home cost of higher premiums may outweigh the short-term benefit.

This is a common example of when not to claim home insurance. Small problems often cost less in the long run if you handle them yourself.

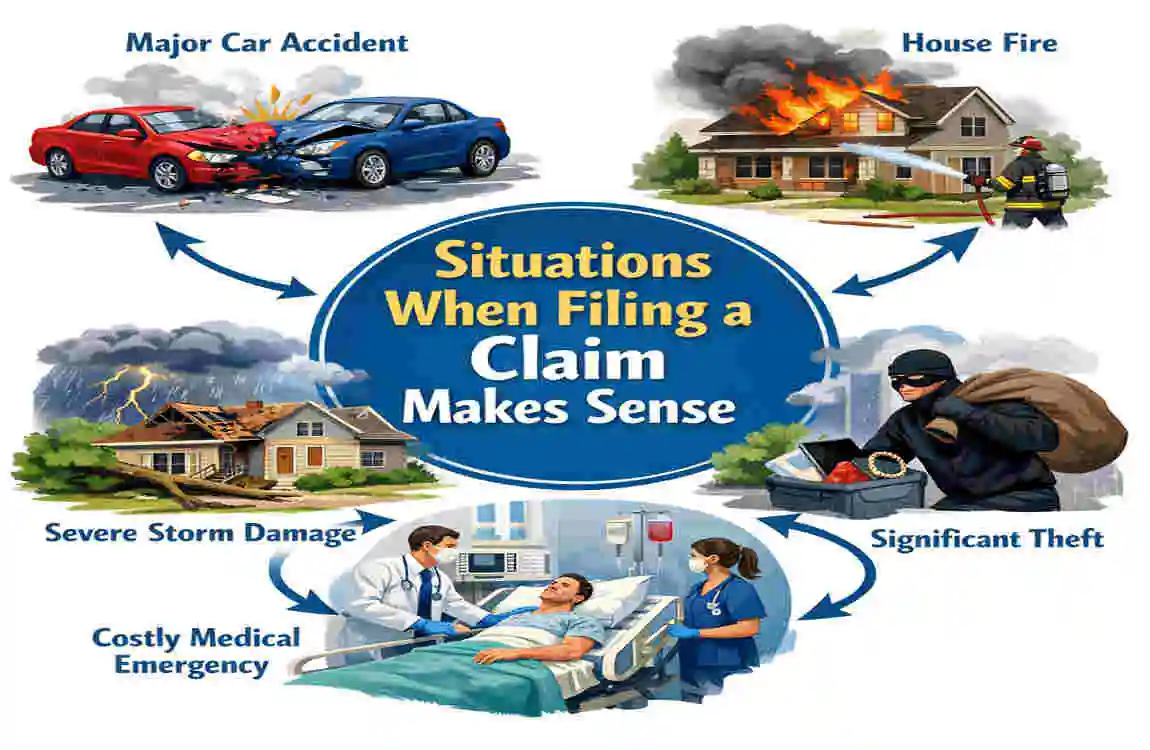

Situations When Filing a Claim Makes Sense

Smart Times to File

There are times when filing a claim is the right move, even if you worry about future costs. These situations usually involve major damage or serious risk.

Major Structural Damage

If your roof collapses, part of your home catches fire, or a severe storm destroys key parts of the house, a claim makes sense. These losses are too large for most homeowners to handle on their own.

In these cases, waiting can also increase the damage. A quick claim may help you get repairs started faster and prevent further loss.

Theft of High-Value Items

If someone steals electronics, jewelry, or other expensive belongings, a claim can help replace them. This is especially true if the items were worth much more than your deductible.

Just make sure you have proof of ownership if possible. Receipts, photos, or serial numbers can help support your claim.

Liability or Injury Claims

If someone is injured on your property and medical or legal costs follow, your policy may help cover the situation. These claims can become expensive fast, so home insurance can offer important protection.

This is one of the clearest examples of when should you file a homeowners insurance claim. When legal risk is involved, the claim may be worth far more than the premium increase.

Water Damage from Covered Causes

Sudden water damage from a burst pipe or unexpected leak is often a good reason to file. Water can spread quickly and ruin flooring, walls, furniture, and more.

The key word is sudden. If the damage came from a long-term maintenance problem, the claim may not be approved.

Situations When You Should Avoid Filing a Claim

When It May Cost More Than It Helps

Not every problem should turn into a claim. Sometimes the smartest decision is to pay for the repair yourself.

Minor Repairs Under Deductible

If the cost of the fix is less than, or only slightly above, your deductible, filing rarely helps. For example, a $700 repair with a $1,000 deductible does not make sense as a claim.

This is one of the clearest cases for when is it not worth claiming on home insurance. You may spend less overall by paying out of pocket.

Cosmetic Damage

Scratches, dents, faded paint, and similar issues usually do not justify a claim. These are frustrating, but they often do not threaten the safety or structure of your home.

Insurance is usually best for bigger losses, not small appearance issues.

Frequent Small Claims

If you keep filing small claims, the long-term cost can rise fast. Your insurer may see the pattern and increase your rates or limit your renewal options.

Sometimes one small repair is no big deal. But repeated small claims can create a much bigger problem later.

Damage Not Covered

If the damage came from neglect, poor maintenance, or an excluded event, the claim may be denied. That can waste your time and still leave you with the property repair cost.

Before filing, ask whether the policy truly covers the issue. If it does not, a claim will only add to your record without helping your wallet.

How Filing a Claim Can Affect Your Premium

Will Home Insurance Go Up After a Claim?

In many cases, yes. That does not mean every claim causes a huge increase, but insurers often review your risk after each one.

The size of the increase depends on a few things: the type of claim, the amount paid, your past claim history, and your insurer’s own rules. A large water-damage claim may affect your rate more than a small broken-window claim.

Some claims are viewed as especially costly.

Claims That Impact Rates Most

Certain claims tend to raise concern more than others:

- Water damage

- Liability claims

- Repeated theft claims

These losses can signal future risk, potentially leading to higher premiums. If you are wondering whether home insurance increases after a claim, the safest answer is that it often does, especially if the claim is large or repeated.

Questions to Ask Before Filing a Claim

Quick Checklist Before You Claim

Before you contact your insurance company, ask yourself these simple questions:

- What is my deductible?

- How much will repairs cost?

- Is the damage covered?

- Will this increase my premium?

- Is this my first recent claim?

- Can I afford to pay out of pocket?

These questions help you slow down and make a calmer choice. Sometimes the answer becomes clear very quickly once you compare the numbers.

Smart Steps Before Contacting Your Insurance Company

Protect Yourself First

A few smart steps can make the whole process easier and stronger.

Document the Damage

Take clear photos and videos of everything you can. Save receipts for damaged items if you have them. Good records can help support your claim and make the process smoother.

Prevent Further Damage

If it is safe, take temporary steps to stop more home damage. For example, cover a broken window, shut off water after a pipe burst, or move items away from a leak.

Do not make major repairs before documenting the scene. You want proof of what happened.

Get Repair Estimates

If possible, get one or two repair quotes. This helps you compare the likely cost against your deductible. It also gives you a better sense of whether a claim is worth it.

Review Your Policy

Look at your coverage, exclusions, and limits before you file. This is one of the smartest things you can do. It helps you avoid surprises and gives you a stronger idea of what the insurer may cover.

Alternatives to Filing a Home Insurance Claim

Other Ways to Handle Small Damage

Sometimes there are better options than filing a claim. Here are a few common alternatives to home insurance claims:

- Use emergency savings

- Ask about a home warranty if the problem fits the plan

- Set up payment plans with contractors

- Handle minor repairs yourself if you have the skills

These choices can help you avoid a claim record when the damage is small. They also keep your policy cleaner for bigger emergencies later.

Expert Tips to Decide If It’s Worth Claiming

Practical Decision-Making Advice

If you want a simple method, use the 2x deductible rule as a rough guide. If the repair is less than about twice your deductible, paying yourself may be smarter. If the loss is much larger, a claim may be worth considering.

Also, try to avoid repeated small property claims. Keep your home in good shape and save records of maintenance work. That can help if you ever need to show that the damage was sudden and not caused by neglect.

Review your policy once a year. Insurance needs change, and your coverage should match your home’s real value and risk level.

FAQ: Home Insurance Claim Questions

Is it worth claiming on home insurance for small repairs?

Usually not if the repair cost is close to your deductible. In many small cases, paying yourself is cheaper in the long run.

Does filing a home insurance claim raise premiums?

Yes, it can. The impact depends on the claim type, amount, and how often you file.

How many home insurance claims are too many?

There is no single number, but several claims in a few years may affect renewal or rates.

Should I pay out of pocket instead of claiming?

For minor damage, yes, that is often the better choice. It can help you avoid premium increases.

What types of damage should always be claimed?

Major structural damage, liability problems, and serious covered losses are the strongest reasons to file.