A contractor in Lahore finishes a custom home, hands over the keys, and everyone is happy with the result. Then, months later, the builder’s business runs into serious trouble. A major defect appears, and the homeowner wants repairs. The bill lands at $50,000. Without protection, that kind of claim can destroy a small business and leave the homeowner stuck in a painful mess.

This type of insurance is designed to protect against builder insolvency, structural defects, and certain construction problems after a home is built or renovated. In many places, it is not just a smart choice; it is a necessity. It is a legal requirement for contractors on qualifying projects. For homeowners, it adds a layer of confidence that the money spent on a house is not lost if something goes wrong later.

| Item | Typical range / details |

|---|---|

| Typical premium as % | Roughly 0.25%–1% of the contract or home purchase price, depending on provider and region. |

| Per‑home example (US) | Often $500–$1,000 for a single‑family home, sometimes under 0.5% of total price. |

| Per‑$1,000 structure (US programs) | Around $2.50–$5.00 per $1,000 of home value for 10‑year structural warranty programs. |

| Australian state‑based HBCF ranges | Premiums expressed as a % of contract value (commonly 0.5%–1%), with minimum or maximum caps per project. |

| Who pays the premium? | Legally taken out by the builder, but cost is usually passed on to the homeowner via the contract. |

| Common coverage periods | 2–10 years depending on program: 2 years for materials/labour, 5 years for water tightness, 10 years for structural defects (“2‑5‑10”). |

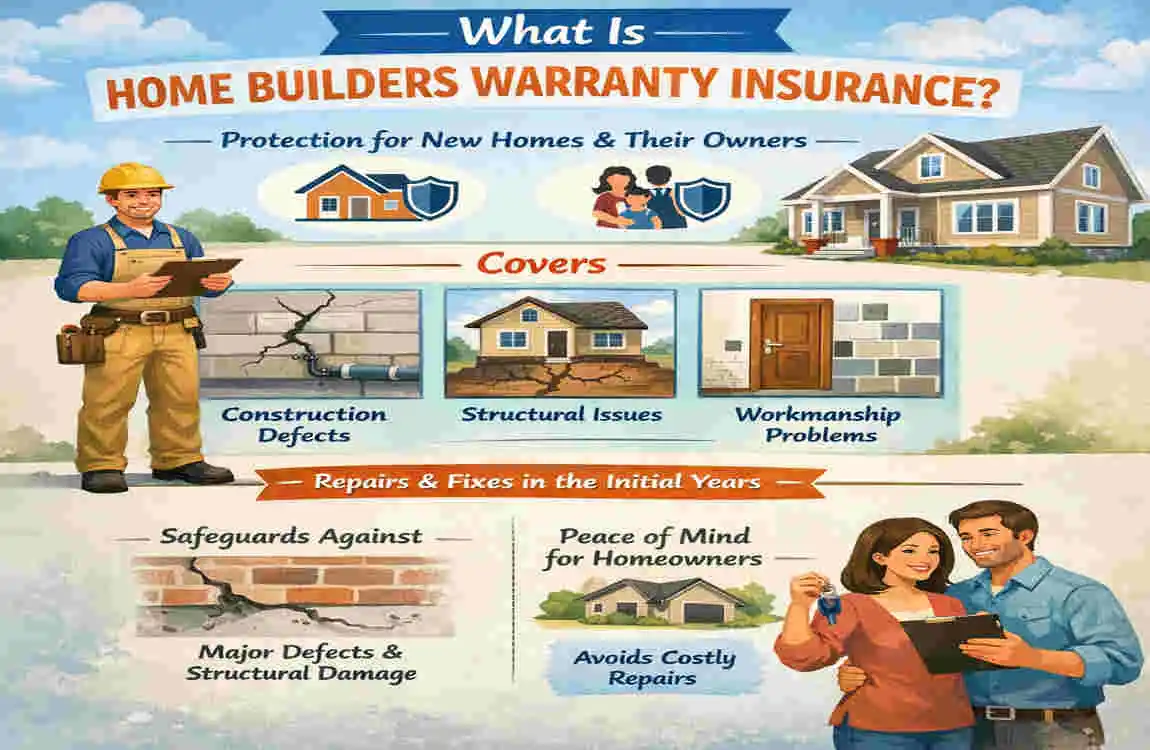

What Is Home Builders Warranty Insurance?

A simple way to understand it

At its core, home builders warranty insurance is a safety net for new homes and major renovations. It helps cover certain defects if the builder cannot fix them because of death, disappearance, or insolvency. It also protects against serious building issues that may arise after handover.

Think of it as a promise that the home is backed by more than just the builder’s word. It gives buyers and owners peace of mind when investing in a new property.

What it usually covers

The exact coverage depends on the policy and the country, but in general, it focuses on two broad areas:

- Structural issues that affect the strength and safety of the home

- Non-structural defects that may affect parts of the house, such as certain finishing or service items

For example, a cracked foundation is a serious structural issue. A leaking roof or failed plumbing connection may also fall under a covered defect, depending on the policy wording and timing.

Typical coverage periods

Many warranty policies are split into different timeframes:

- Structural coverage: often around 6 years

- Non-structural coverage: often around 2 years

That means some problems must be reported much sooner than others. The clock usually starts when the home is completed or handed over.

Common coverage examples

TypeDurationMax PayoutExample

Structural 6 years Up to $340,000 Cracked foundation

Non-Structural 2 years Up to $340,000 Leaky roof

Who needs it?

This insurance is often required for:

- Contractors working on qualifying new builds or major renovations

- Homeowners who want to confirm the builder is properly covered before paying a deposit

- Developers managing multiple homes or units

Why It’s Mandatory for Contractors

A legal requirement in many markets

For contractors, this is not always optional. In NSW, WA, and QLD, home warranty rules may apply once the project value exceeds certain thresholds. In other words, if you are building above the local limit, you may need to arrange the insurance before work can continue or before a permit is approved.

The threshold can vary by region. Some areas use a higher limit, while others use a lower one. But the idea is the same: the law wants to protect the homeowner if the builder cannot finish or fix the work.

What happens without it?

Skipping this coverage can cause serious trouble.

A contractor without the right warranty insurance may face:

- Fines or compliance penalties

- Stopped or delayed projects

- Problems getting permits approved

- Legal claims from unhappy clients

- Damage to business reputation

That last point is especially important. In construction, trust matters as much as skill. If clients think you are cutting corners on protection, they may not hire you again.

Why it helps business growth

There is also a positive side. Having home builders warranty insurance can actually help a contractor win more jobs.

Why?

Because homeowners feel safer when they know the project is protected. It tells them the builder is serious, compliant, and prepared for the unexpected. In many cases, the policy also makes it easier for the builder to collect deposits and move forward with the work.

A practical business view

For a contractor, home builders warranty cost is not just another line item. It is part of running a proper business. If you look at it from the right angle, it is a cost that protects cash flow, reduces risk, and builds trust.

In Pakistan, the market is also moving toward stronger protection models. Local insurers increasingly offer home-related policies that reflect this same need for risk control and buyer confidence.

Homeowner Perspective: Is It Worth It?

Why homeowners should care

If you are buying a new home or paying for a major renovation, you want to know that the work is protected after the handover. That is where homeowner builder insurance and structural warranty coverage can make a real difference.

Many homeowners focus only on the finished look. But the real risk often hides in the parts you cannot easily see, such as foundations, framing, drainage, wiring, or roofing details. If those fail later, repairs can become expensive fast.

What the protection gives you

A warranty policy can help with:

- Major defects discovered after handover

- Builder death, disappearance, or insolvency

- Repair costs tied to covered structural issues

- Peace of mind during the early years of ownership

That peace of mind has real value. When someone spends most of their savings on a house, they do not want a hidden defect to become a financial disaster.

Is the premium passed on to the buyer?

In many cases, yes. Builders often include the cost in the overall project price. That means the homeowner may effectively pay for it through the contract, even if the builder arranges the policy.

This is why buyers should always ask whether the project includes warranty protection and request proof before paying a large deposit.

Why it matters in Pakistan too

The Pakistani housing market is growing, and buyers are becoming more aware of build quality and long-term risk. As urban development expands, more homeowners want the same kind of safety net that is common in other markets.

How Much Is Home Builders Warranty Insurance? Average Costs

The short answer

So, how much is home builders warranty insurance in 2026?

The typical range is 0.25% to 1% of the home’s contract or sales value. For some projects, that can translate to a fixed premium of $200 to $5,000+, depending on the contract value and provider rules.

That means a $300,000 home might generate a premium of $750 to $3,000. A larger custom build may cost more, especially if the risk profile is higher or the insurer requires extra review.

Why prices vary so much

The price is not random. Insurers look at the size of the job, the location, the builder’s background, and the exact type of coverage. A small renovation with fewer risk points usually costs less than a large custom build with more complexity.

Example pricing by project value

Contract ValueBase Premium% of ValueNotes

Under $50K $200 + GST Fixed Small renos

$50K–$100K $250 + GST Fixed Mid-size projects

$100K+ 0.09% + $200 Variable Larger custom homes

$500K Home $1,250–$5,000 0.25%–1% Common U.S. range

What this means in real life

If your project is small, the premium may feel like a fixed administration fee. If your project is large, the policy may behave more like a percentage-based risk charge.

For many small firms, the monthly impact is around $100 to $300. However, the exact figure depends on the insurer and the project profile. Higher-risk projects can push costs upward by 1% to 5% in certain cases.

A better way to think about it

Instead of asking only, “What is the cheapest price?” ask, “What level of protection do I actually need?”

Sometimes a slightly higher premium gives better coverage, easier claim handling, or a smoother approval process. That can be worth far more than saving a few hundred dollars upfront.

Factors Affecting Pricing

Project value and location

The bigger the job, the higher the premium usually becomes. A luxury home, a multi-unit project, or a complex renovation attracts more attention than a small repair.

Location matters too. Urban areas often have higher labour costs, stricter regulations, and greater claim pressure. In many cases, home builders’ warranty costs will be higher in a city like Lahore than in a quieter rural area, simply because the project environment is more expensive and complex.

Builder experience and record

Insurers pay close attention to the builder’s background.

A contractor with a strong history of completed projects, low claims, and proper licensing may get better pricing. A newer builder, or one with a less stable record, may pay more because the insurer sees more risk.

That is why contractors warranty insurance pricing often rewards consistency and good documentation. If you run a construction business, clean records are not just good practice; they are essential. They can also save you money.

Coverage limits and deductibles

The more protection you want, the more you may pay.

Higher coverage limits usually increase the premium. Lower deductibles can also raise prices because insurers are taking on more of the smaller losses. If you choose a higher deductible, you may reduce your premium, but you will also pay more out of pocket if you file a claim.

Common deductible choices may include:

- $500

- $1,000

- $2,500

- $5,000

Provider selection

Not all insurers price the same way.

Some providers focus on new construction and charge less than 0.5% in many cases. Others may offer more flexible protection but at a slightly higher cost. Structural warranty pricing can shift depending on how the insurer assesses risk and the level of support included.

Regional rules and compliance needs

Regulations affect cost too. Some regions require minimum coverage, specific claim terms, or mandatory paperwork. The more administrative checks involved, the more the premium can rise.

In Pakistan, insurers may tailor policies to local market conditions and property types. That means pricing can vary even more, depending on the city, neighborhood, and project category.

Quick cost-saving tips

- Shop around and compare quotes

- Keep your builder record clean

- Choose the right coverage level, not the highest one

- Avoid unnecessary add-ons

- Bundle when possible

In many cases, careful quote shopping can save 20% to 30%.

Cost Comparison: Top Providers

A simple comparison can save money

When people ask how much home builder warranty insurance costs, they often expect a single fixed number. But the truth is that different providers structure their fees differently.

Some charge a small percentage of the contract value. Others use a minimum premium. A few may be better for contractors who work on regular residential projects. In contrast, others are more useful for larger structural jobs.

2026 provider comparison

Provider% of ValueMin PremiumBest For

2-10 HBW Under 0.5% $500 New construction

PWSC 0.25%–0.5% Per $1K Structural coverage

HIA (NSW) 0.09%+ $200 Contractors

IGI Pakistan Custom Varies Local homes

What this table really shows

The cheapest-looking premium is not always the best deal. A provider with a slightly higher price may offer easier claims support, smoother paperwork, or better alignment with local rules.

For example, a builder working on a custom home may prefer a provider with stronger structural coverage. A contractor doing multiple small jobs may prefer a model with low admin costs and predictable renewal terms.

Why it matters for your budget

The average annual cost for a small construction business can land around $1,259. Still, that figure can move up or down depending on project size, risk, and provider type.

This is where careful comparison becomes important. The right provider can reduce both your home builders warranty cost and your stress.

Hidden Costs and Smart Savings Tips

Hidden costs can surprise you

The premium itself is only part of the story. Some contractors discover that additional costs surface later, raising the final bill.

These may include:

- Legal or compliance fees

- Document preparation charges

- Inspection or administration costs

- Extra premiums for high-risk projects

- Fees tied to policy changes or extensions

If you are not careful, these extras can increase the total by 10% to 20%.

How to keep the cost under control

You do not have to accept the first quote you receive. In fact, that is usually a bad idea.

Here are smart ways to save money:

- Compare at least three quotes

- Ask about bundle discounts

- Keep your project records organized

- Use the correct project value

- Avoid paying for unnecessary extras

Why bundling can help

If you already have other business insurance, you may be able to combine policies and reduce your overall premium. This can work especially well for contractors who also need liability or property coverage.

A simple rule to remember

The lowest premium is not always the best value. Look at the coverage terms, claim process, and deductible, not just the number on the quote.

That approach will help you understand the true structural warranty pricing rather than just the advertised rate.

Claims Process and Payouts

What happens when something goes wrong?

A warranty policy only matters if the claim process works when you need it. Fortunately, the steps are usually straightforward if you act on time.

Typical claim steps

- Notify the builder or provider as soon as you spot the problem

- Submit photos, records, and basic details

- Allow an assessment or inspection

- Wait for the decision

- Receive repair support or payout if the claim is approved

The most important part is timing. Many policies expect the problem to be reported within a specific time after you become aware of it.

Why timing matters

If you wait too long, the insurer may reject the claim or reduce the payout. That is why homeowners should keep an eye on the property during the early years after handover.

Example of a large payout

Some policies can cover major structural claims up to $340,000, depending on the terms and the nature of the damage. That level of support can be life-changing if a foundation or major frame problem appears.

Best practice for homeowners

If you think something is wrong, do not delay. Write it down, take photos, and contact the correct party quickly. A prompt response often makes the difference between a smooth claim and a long dispute.

Alternatives to Traditional Warranties

When a standard policy is not the best fit

Not every project needs the same setup. In some cases, builders and homeowners use other forms of protection.

Common alternatives

- Self-insurance for very small jobs

- Builder risk insurance

- Local bond arrangements

- Project-specific guarantees

- Direct reserve funds for minor work

When self-insurance may work

If the job is very small, the cost of full warranty coverage may feel too high compared with the risk. In those situations, a contractor might set aside funds for repairs rather than purchase a more formal policy.

Builder risk insurance is different

Builder risk coverage is usually about damage during construction, not long-term structural defects after handover. It protects the project during construction, which is useful but not the same as a home warranty.

Pakistan and local arrangements

In Pakistan, some developers may use local bond-style arrangements or insurer-backed home plans that align with the project’s scale. These options can be helpful, but homeowners should still read the terms carefully to understand what is actually covered.

Home Builder Warranty Cost in Practice: A Realistic Budget View

Planning from the start

When you budget for a build, do not treat warranty insurance as an afterthought. Add it early, right alongside labor, materials, approvals, and site overhead.

That gives you a more realistic view of the full project cost.

A sample budget mindset

For example, if a house costs $300,000, a warranty premium of 0.25% to 1% could mean a cost of roughly:

- $750 at the low end

- $1,500 at a middle estimate

- $3,000 at the higher end

That range may seem small compared with the total project, but it still matters to your margin. For a contractor, every extra charge affects pricing strategy. For a homeowner, every added cost affects affordability.

Why this is worth planning for

A small upfront premium can prevent a very large future loss. That is the core value of the policy. You pay a manageable amount now so you do not face a much bigger financial shock later.

This is why home builders warranty cost should be included in every serious project estimate.

Common Mistakes People Make

Buying too late

Some builders wait until the last minute. That can cause delays, compliance problems, or missed deadlines.

Choosing price over coverage

A cheap policy may not be the right policy. Always check the claim terms and exclusions.

Not confirming who pays

Homeowners sometimes assume the builder has arranged everything. Builders sometimes assume homeowners know the price is included. That confusion can lead to frustration.

Forgetting to keep records

Photos, contracts, inspection notes, and handover documents can all matter later during a claim.

Not checking local rules

A policy that works in one country may not satisfy the rules in another. If your project is in Pakistan or another market, ensure the coverage aligns with the local legal environment.

FAQ: How Much Is Home Builders Warranty Insurance?

How much is home builders warranty insurance for a $300,000 home?

For a $300,000 home, the cost is often around $750 to $3,000, depending on the provider and risk level. That works out to roughly 0.25% to 1% of the contract value.

Who usually pays for home builders warranty insurance?

In many cases, the builder pays first, but the cost is often built into the total contract price. So the homeowner may end up covering it indirectly through the project cost.

Is home builders warranty insurance the same as builder risk insurance?

No, they are different. Home builders warranty insurance usually protects against defects and builder failure after the project is finished. Builder risk insurance is usually for damage during construction.

Do homeowners need to buy it themselves?

Usually, no. The contractor or builder arranges it in many markets. But homeowners should still ask for proof before paying a deposit or finalizing the contract.

Is this kind of insurance available in Pakistan?

Yes, similar home-related protection may be available through local insurers and property insurance products. The exact structure can vary, so buyers should check the policy wording carefully.

What affects structural warranty pricing the most?

The biggest pricing factors are:

- Project value

- Location

- Builder experience

- Coverage limit

- Deductible

- Provider rules

Can I save money on home builders warranty cost?

Yes. You can save by comparing quotes, keeping a strong builder record, avoiding unnecessary add-ons, and choosing the right coverage for the project size.

How fast should a defect be reported?

You should report it as soon as you notice it. Many policies require the issue to be reported within a specific time after discovery, so waiting can hurt your claim.

What if the builder goes out of business?

That is one of the main reasons this insurance exists. If the builder becomes insolvent, disappears, or is unable to complete the work, the policy may help cover qualifying claims.

What is the best way to estimate home builders warranty insurance?

The easiest method is to use the project value and apply the common range of 0.25% to 1%. Then adjust for location, builder history, and the insurer’s minimum fee.