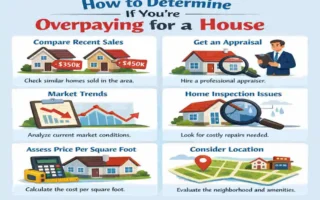

It sounds simple, but the answer is not the same for everyone. In some places, a building gives you more value. In other places, buying is the smarter choice. That is because home prices, land costs, labor, and loan rules can all change the final number.

| Option | Typical cost signal | What it means |

|---|---|---|

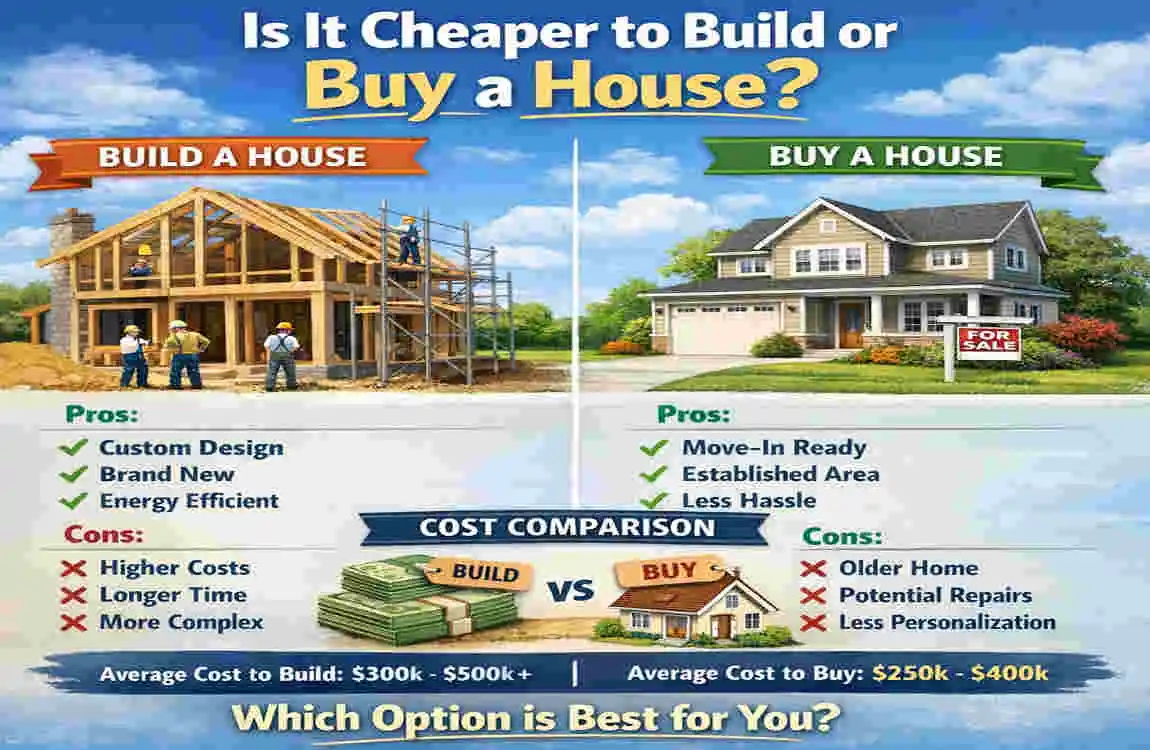

| Build | About $644,750 average new-home cost in 2022; often more now | Usually costs more upfront, especially after land, permits, and delays are added. |

| Buy | About $535,500 average existing-home cost in 2022 | Usually cheaper and faster, with less financing and waiting risk. |

| Exception | In places like Hawaii, building can save about $494,000 vs. buying | Building may be the better value in very expensive housing markets. |

Many buyers only look at the sticker price. That is a mistake. A house can seem cheap at first, but it still costs a lot later due to repairs, permits, or hidden fees. On the other hand, building a home may look expensive up front. Still, it can save money over time if you choose a simple design and efficient materials.

Understanding the Core Question: Is Cheaper to Build or Buy a House?

Quick Answer

The short answer is it depends.

Building home can be cheaper in areas where land is affordable and labor is stable. Buying can be cheaper when homes are already available at fair prices, and you want to move in quickly.

Several factors shape the final cost:

- Land prices

- Material costs

- Labor rates

- Taxes and permits

- Location

- Financing terms

Why There Is No One-Size-Fits-All Answer

A home in a city usually costs more than a home in a rural area. A custom home also costs more than a simple standard build. Even an older house can become expensive if it needs major repairs.

So the real question is not just which costs less today, but which gives you better value over time.

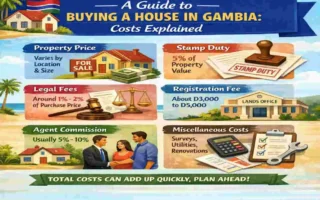

Cost Breakdown: Building a House From Scratch

Land Purchase Costs

Before you build, you need land. This is often the biggest first expense.

You may also pay for:

- Survey fees

- Legal checks

- Soil testing

A cheap plot can still become costly if the ground is unstable or if utilities are far away.

Construction Material Costs

Materials can quickly shift a project budget. Common items include:

- Cement

- Bricks

- Steel

- Lumber

- Roofing

- Electrical supplies

If prices rise during your build, your total cost may grow even if your plan stays the same.

Labor Costs

You will need skilled workers for different parts of the job, such as:

- Contractors

- Electricians

- Plumbers

- Carpenters

- Painters

Labor costs often rise in busy markets, especially when many homes are being built at once.

Design and Permit Costs

A custom home usually needs more planning. You may pay for:

- House plans

- Structural engineering

- Interior design

- Construction permits

- Inspection fees

These costs are easy to miss, but they matter a lot in the final budget.

Utility and Exterior Costs

Once the house is built, you still need to connect the property and finish it. That may include:

- Water and sewer

- Electricity

- Gas

- Internet setup

- Driveways

- Fencing

- Landscaping

These final steps can add a surprising amount to the total.

Cost Breakdown: Buying an Existing House

Purchase Price

Buying is often easier to understand because the price is clear from the start. Still, the final price depends on the market and your negotiation power.

If demand is high, you may pay more than expected. If the market is slower, you may get a better deal.

Closing Costs

The sale price is not the full story. You also need to budget for:

- Registration fees

- Taxes

- Legal fees

- Loan processing charges

These costs can add up fast, especially for first-time buyers.

Repair and Renovation Costs

An older home may need updates right away. Common repairs include:

- Roof replacement

- Plumbing fixes

- Electrical rewiring

- Paint and flooring changes

Even a home that looks move-in ready may need more work than you expect.

Inspection and HOA Fees

A home inspection helps uncover serious problems before you buy. You may also face homeowners’ association fees in some neighborhoods.

These fees can be manageable, but they still affect your monthly cost.

Quick Comparison Table

Cost Area: Building a House, Buying a House

Upfront Cost Often higher and less predictable Usually clearer and faster

Hidden Costs : Permits, land prep, delays , repairs, inspections, closing fees

Move-In Time Slower Faster

Customization Very high Limited

Long-Term Maintenance Often lower at first Often higher for older homes

Hidden Costs Most People Ignore

When Building a Home

Building a house can go over budget for simple reasons. For example:

- Material prices can rise

- The weather can delay work

- Contractors may charge more for changes

- Design edits can increase labor costs

- Waste removal can cost extra

Even small changes can affect the final price.

When Buying a Home

Buying also comes with hidden costs. You may discover:

- Mold problems

- Foundation damage

- Old appliances

- Higher insurance rates

- Outdated heating or cooling systems

This is why inspections matter so much.

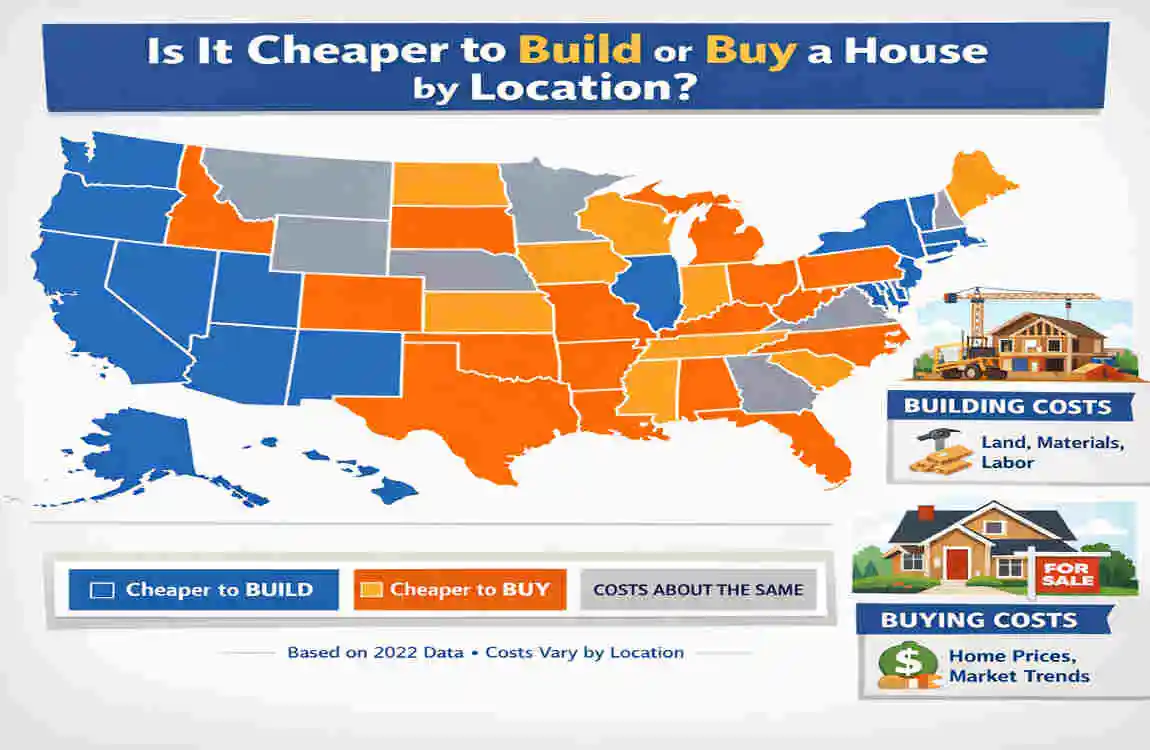

Is It Cheaper to Build or Buy a House by Location?

Urban Areas

In cities, land is usually expensive. That makes building harder to afford. In many cases, buying an existing home is the cheaper and faster choice.

Suburban Areas

Suburbs often offer a mix of both options. You may find new developments with buildable land, but you may also find older homes that need updates.

Rural Areas

Rural land may cost less, making building more attractive. But you should also check utility access. If water, power, or sewer lines are far away, setup costs can rise.

High-Demand Markets

In hot housing markets, both buying and building can become expensive. Homes sell quickly, and construction costs can remain high as demand remains strong.

Time Comparison: Which Option Takes Longer?

Buying a Home

Buying is usually faster. You still need mortgage approval, inspections, and closing, but the timeline is much shorter than building.

Building a Home

Building takes longer because you must handle planning, permits, construction, and finishing work. Delays are common.

Time Equals Money

If you need temporary housing while waiting, your total cost goes up. Rent, storage, and travel can all add pressure to your budget.

Financing Differences Between Building and Buying

Construction Loans

A construction loan is not the same as a normal mortgage. It may have:

- Higher interest rates

- Strict lender requirements

- Stage-based payouts

That means the bank releases funds in stages as the home is built.

Traditional Mortgages

Buying a home usually involves a standard mortgage. This process is often simpler and may come with better rate options.

Down Payments and Credit Scores

In many cases, building requires more cash up front. Lenders may also expect stronger credit because construction loans feel riskier to them.

Maintenance Costs Over Time

Newly Built Homes

New homes often need less repair in the early years. They may also be more energy efficient, which can lower monthly bills.

Older Homes

Older homes may need more maintenance. Systems age, materials wear out, and remodeling can become expensive.

Over time, this can make buying look cheaper at first but more costly later.

Pros and Cons of Building a House

Advantages

- Full customization

- Modern layout

- Better insulation

- Smart home features

- Possible energy savings

Disadvantages

- Longer timeline

- Budget uncertainty

- Permit issues

- More stress during the process

Building is great if you want control, but it demands patience.

Pros and Cons of Buying a House

Advantages

- Faster move-in

- More predictable process

- Established neighborhoods

- Easier financing in many cases

Disadvantages

- Limited customization

- Possible repairs

- Older systems

- Competition from other buyers

Buying works well if speed and simplicity matter most.

Real-Life Scenarios: When Building Is Cheaper

Building may be cheaper when:

- Land is affordable

- The house design is simple

- Labor costs are stable

- You do some finishing work yourself

- You want a small, energy-efficient home

In these cases, building can offer strong long-term value.

Real-Life Scenarios: When Buying Is Cheaper

Buying may be cheaper when:

- You find a foreclosure or fixer-upper

- The market favors buyers

- Construction costs are very high

- You need to move soon

- You want to avoid project risk

If time matters more than customization, buying often wins.

How to Decide What Is Best for Your Budget

Ask Yourself These Questions

- Do I need a home quickly?

- Can I handle delays and surprises?

- Is custom design important to me?

- Can I afford land and utility setup?

- Do I want lower maintenance in the first few years?

Build vs Buy Budget Checklist

Before you decide, review:

- Your total budget

- Emergency savings

- Loan approval

- Repair reserve

- Utility setup costs

This simple checklist can help you avoid a costly mistake.

Expert Tips to Save Money

If you want to keep costs low, try these simple steps:

- Compare at least 3 contractors

- Get a full home inspection

- Avoid over-customizing

- Negotiate every fee you can

- Track hidden expenses early

- Choose energy-efficient materials

- Shop during slower seasons

Small savings can make a big difference.

FAQs

Is it cheaper to build or buy a house in 2026?

It depends on local land prices, labor costs, and the home market in your area.

What is the biggest hidden cost when building a house?

Permit fees, utility setup, and delays often cause the biggest budget surprises.

Is buying an older house cheaper than building?

Usually, yes at first, but repair and maintenance costs can be much higher later.

Can building a home increase resale value?

Yes, especially if the home has modern features, good energy efficiency, and a smart layout.

Which is faster: building or buying a home?

Buying is almost always faster than building.