If you are thinking about buying a house in the UK, one of the first questions that comes up is simple: how much uk real estate house prices really cost once you look at the full picture?

The answer is not as simple as a single number. UK property costs vary by city, property type, mortgage rates, taxes, and legal fees. A home in London can cost several times as much as a similar home in Wales or parts of northern England. Even within the same city, prices can vary widely from one area to another.

Understanding the UK Real Estate Market

What Is Considered UK Real Estate?

UK real estate includes many different types of homes. When people talk about property prices, they may mean:

- Detached houses

- Semi-detached houses

- Terraced homes

- Flats and apartments

- Luxury estates

- New-build homes

Each type comes with a different price range. A flat in a city centre may cost less than a detached family home in the suburbs, but the location can change that quickly.

Factors Affecting UK Property Prices

Several big factors shape UK property prices. The most important ones are:

- Economic conditions

- Interest rates

- Population growth

- Jobs and wages

- Supply and demand

- Foreign investment

When more people want to buy than there are homes available, prices usually rise. That is one of the main reasons the UK property market has stayed strong in many areas.

Why UK Housing Prices Continue to Rise

There are a few main reasons house prices keep moving up over time:

- Not enough homes are being built.

- More people are moving to major cities for work.

- Inflation raises the cost of land, labour, and materials.

- Popular areas continue to attract buyers, pushing prices higher.

For many buyers, acting sooner rather than later can make sense, especially if you are looking for affordable UK property in a growing area.

Average UK House Prices in 2026

Current National Average House Price

The average house price UK buyers are seeing in 2026 still varies by source and area. National averages are useful, but they do not tell the full story.

A typical home in England will usually cost more than similar homes in Wales or parts of Scotland. That is why many buyers should focus on local data rather than just the national number.

Average Prices by Property Type

Different homes cost different amounts. Here is a simple guide:

Detached Houses

Detached houses are usually the most expensive standard home type because they offer the most space and privacy. They are popular with families and buyers seeking more space.

Semi-Detached Houses

Semi-detached houses often sit in the middle of the market. They are a common choice for families because they balance space and price reasonably well.

Terraced Homes

Terraced homes are usually more affordable than detached or semi-detached houses. They are often a smart option for first-time buyers who want a lower entry point.

Flats and Apartments

Flats and apartments are often the cheapest way to get into the UK housing market, especially in city areas. However, service charges and leasehold rules can add extra costs.

Cost Per Square Foot in the UK

The cost per square foot varies widely across the country. In central London, it can be very high. In smaller towns or suburban areas, it is usually much lower.

This is why a smaller house in a prime location can cost more than a larger home in a less popular region. In property, location matters a lot.

Monthly Mortgage Expectations

Your monthly payment depends on the home price, your deposit, and your mortgage rate. Even a small change in interest rates can make a big difference.

Most buyers will need to think about:

- Deposit size

- Mortgage term

- Interest rate

- Monthly repayments

If you are buying a house in the UK, it is wise to calculate not just the house price, but also the long-term cost of borrowing.

UK Real Estate Prices by Region

London Property Prices

London remains the most expensive part of the UK housing market. This is true whether you are looking in central areas or Greater London.

In central London, buyers often pay a premium for location, transport, and access to jobs. Greater London is usually more affordable, but it is still well above the national average.

If you are comparing London property prices with other cities, the difference can be striking. London may offer strong long-term value, but it requires a much bigger budget.

Manchester Real Estate Costs

Manchester has become one of the most talked-about markets in the UK. It is still much more affordable than London, but prices have risen due to strong demand.

Why do buyers like Manchester?

- Good transport links

- Strong rental demand

- A growing job market

- Regeneration in many neighbourhoods

For investors, Manchester often looks attractive because it offers a balance between price and growth potential.

Birmingham Housing Prices

Birmingham sits in a middle range for many buyers. It is often seen as a solid choice for families, first-time buyers, and investors who want value without going too far out of major-city life.

The city has good schools, business growth, and a broad mix of homes. That makes it one of the more practical places to look when searching for UK property market opportunities.

Scotland Property Market

Scotland has its own property market patterns. Edinburgh is usually far more expensive than many other parts of Scotland. At the same time, Glasgow can offer better value depending on the neighbourhood.

There are also some differences in how property sales work in Scotland compared with England and Wales. That is why buyers should always learn the local process before moving ahead.

Wales and Northern Ireland

Wales and Northern Ireland often have lower average house prices than London or parts of southern England. That makes them appealing to buyers looking for affordable UK property.

These areas can be especially good for:

- First-time buyers

- Families wanting more space

- Buyers with smaller deposits

- People looking for long-term value

Region Comparison Table

RegionAverage House PriceCost Trend

London High Increasing

Manchester Medium Growing

Birmingham Medium Stable

Scotland Medium Moderate

Wales Lower Affordable

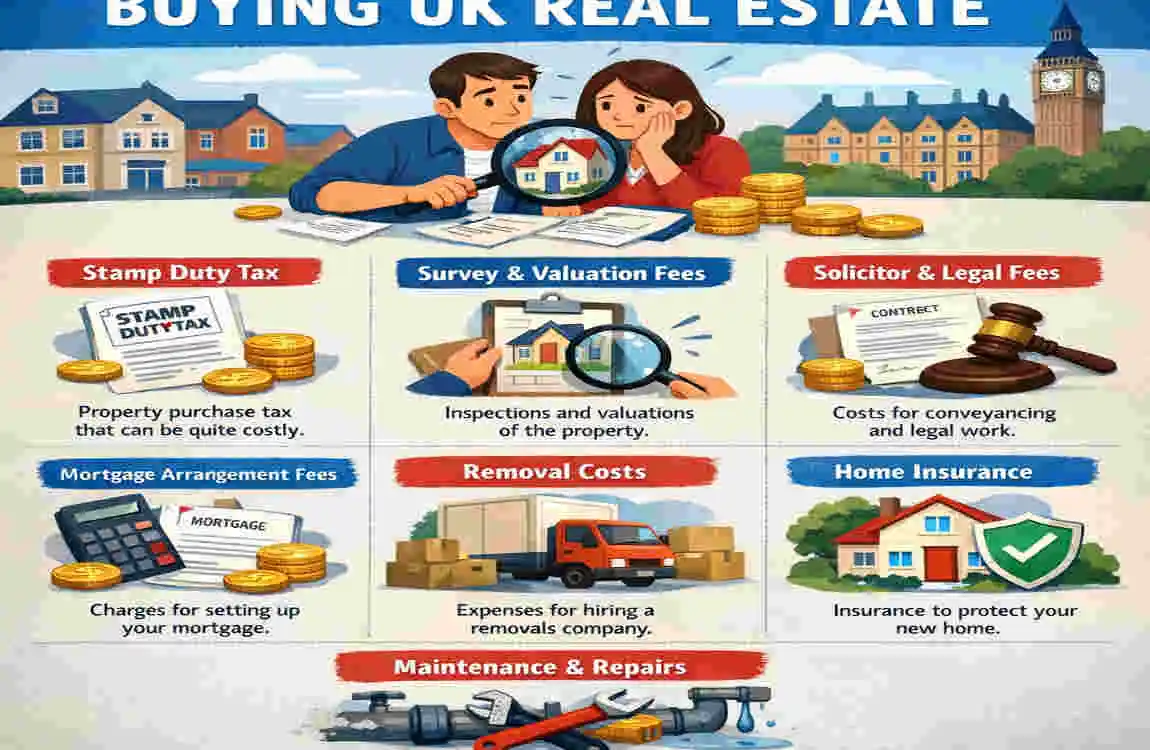

Hidden Costs of Buying UK Real Estate

Many buyers only plan for the purchase price. That is a mistake. The hidden costs can add up fast.

Stamp Duty Land Tax

Stamp Duty Land Tax is one of the biggest extra costs in England and Northern Ireland. The amount you pay depends on the home’s price and whether you are a first-time buyer.

This tax can make a big difference to your budget, so it should be included from the start.

Legal and Conveyancing Fees

You will also need to pay for legal work. This includes the solicitor or conveyancer who handles the paperwork, searches, and transfer of ownership.

These fees may not feel huge compared with the house price, but they still matter.

Survey and Inspection Costs

A survey helps you understand the condition of the home. It can spot issues such as roof damage, damp, and structural problems.

Skipping this step can be risky. If you are buying an older property, a survey becomes even more important.

Mortgage Arrangement Fees

Some lenders charge fees for setting up the mortgage. You may also pay broker fees if you use one.

This is why UK mortgage costs should always be checked carefully before you commit.

Moving and Furnishing Costs

Once you buy the house, the spending does not stop. You may need to pay for:

- Removal services

- Furniture

- Curtains and blinds

- Paint and basic decorating

- Small repairs

As someone who works with property, you already know that a home often needs a little personal touch after purchase. That is where home decor can also become part of the true budget.

Renting vs Buying in the UK

Average Rental Costs

Rent varies a lot by city. London is usually the most expensive, while smaller towns can be much cheaper. In some areas, rents rise quickly because demand is high and supply is low.

Advantages of Buying

Buying gives you:

- Long-term stability

- Potential property growth

- More control over the home

- A possible asset for the future

For many people, owning a home feels more secure than renting.

Advantages of Renting

Renting has its own benefits:

- Lower upfront cost

- More flexibility

- Less responsibility for repairs

- Easier to move for work or lifestyle reasons

Which Option Saves More Money?

There is no single answer. Buying can be cheaper over time if you stay in the same place long enough. Renting may be better if you need flexibility or are not ready for the upfront cost of buying.

Your choice depends on your income, plans, and local market conditions.

Is UK Real Estate a Good Investment?

Historical Property Appreciation

Over the long term, UK property has often increased in value. That does not mean every home goes up every year. Still, the general trend has usually been positive in strong locations.

Rental Yield Opportunities

Some buyers purchase homes to rent them out. This is often called UK property investment or buy-to-let investing.

Areas with students, workers, and growing populations often offer better rental demand.

Best UK Cities for Investors

Some of the more popular cities for property investors include:

- Manchester

- Liverpool

- Birmingham

- Leeds

These places often offer better entry prices than London and can still deliver solid rental demand.

Risks to Consider

Property investment is not risk-free. You should think about:

- Interest rate changes

- Falling demand

- Maintenance costs

- Vacancies between tenants

A smart investor always checks both the upside and the risks.

Tips for Saving Money When Buying a UK House

Compare Mortgage Rates

Do not take the first mortgage offer you see. Compare lenders and focus on the total cost, not just the headline rate.

Buy in Emerging Areas

Some areas are cheaper today because they are still growing. These can be good choices if you want value and future upside.

Improve Credit Score

A stronger credit score can help you get better borrowing terms. That may lower your monthly cost and make buying easier.

Negotiate Property Prices

Always do your research before making an offer. If the home has been on the market for a while, there may be room to negotiate.

Understand Government Schemes

Some buyers may benefit from support schemes such as:

- First Homes Scheme

- Shared Ownership

- Help for first-time buyers

These options can make buying a house in the UK more realistic if your budget is tight.

Common Mistakes Buyers Make

Ignoring Hidden Costs

Many buyers focus solely on the asking price and forget about the additional fees. That can create a budget problem later.

Buying Beyond Budget

It is tempting to stretch for a bigger home, but that can lead to stress if monthly repayments become too high.

Skipping Property Surveys

A survey may seem like an extra cost, but it can save you money in the long run by spotting major problems early.

Not Researching Neighborhoods

A house is more than the building. The area matters for schools, transport, safety, and future resale value.

Overlooking Future Resale Value

Think ahead. If you need to sell later, will the home still attract buyers? That question matters a lot.

Future Trends in UK Real Estate Prices

Market Predictions for 2026 and Beyond

The UK property market is expected to stay active, but price growth may differ by region. Some areas may rise faster than others, especially where jobs and demand are strong.

Impact of Interest Rates

Mortgage costs have a big effect on affordability. If interest rates stay high, many buyers will need to plan carefully. If rates ease, more people may be able to enter the market.

Growing Demand Outside London

Remote work has changed how people choose homes. More buyers are now looking outside London for better value, more space, and a better quality of life.

This shift could continue to support regional cities and towns.

FAQ

How much does a house cost in the UK on average?

The average depends on the region and property type. London is far above the national average, while Wales and some northern areas are usually more affordable.

Is UK real estate expensive compared to other countries?

In many parts of the UK, yes, especially in London and the South East. However, some regional areas still offer good value compared with other major global markets.

What is the cheapest area to buy property in the UK?

Cheapest areas change over time, but many buyers look to parts of Wales, Northern Ireland, and northern England for lower prices.

How much deposit do I need to buy a UK house?

Many buyers aim for at least 5% to 20% of the home price, depending on the mortgage product and lender rules.

Are UK property prices expected to rise?

They may rise in some areas and stay flat in others. Local demand, interest rates, and supply all play a role.

Is buying property in London worth it?

It can be, but only if your budget is strong and your goal matches the market. London offers high demand and strong long-term interest, but the entry cost is very high.