If you have land but not enough cash to build, you may be asking: Can I use my land as collateral to build a house? The short answer is yes, in many cases you can. This is one of the most common ways people turn land into a useful financial asset.

Building a home is expensive. Costs keep rising, and many people do not want to sell their land to start construction. That is where land as collateral comes in. In simple terms, collateral is something of value you pledge to a lender to make them feel safer about giving you a loan.

| Step | What to do | Why it matters |

|---|---|---|

| 1. Confirm clear title | Verify you own the land free of liens and that title is marketable. | Lenders require an unencumbered title before accepting land as collateral. |

| 2. Get a professional appraisal | Order a land appraisal (and a future built-home valuation plan). | Lender uses value to set loan-to-value and decide loan size. |

| 3. Choose loan type | Compare one-time-close construction-to-permanent loans, separate construction loans, or land equity loans. | Different structures affect closing costs, draw schedule, and conversion to a mortgage. |

| 4. Prepare financial documents | Gather income proof, credit report, tax returns, and budget/contractor estimates. | Lenders assess creditworthiness and construction budget before approval. |

| 5. Provide down payment / equity | Be ready to supply required down payment or use land equity toward the required margin. | Most lenders require 10–30% (varies by loan program); some government programs have different rules. |

If the land meets the lender’s rules, it can help you get a construction loan, a land equity loan, or another type of property-backed loan. This can open the door to building the home you want without giving up ownership of your land.

Understanding Land as Collateral

What Does Collateral Mean?

Collateral is a valuable asset used to secure a loan. If you do not repay the loan, the lender may have the legal right property take the asset and recover the money.

This does not mean you lose the asset right away. It simply means the lender has protection. That protection reduces their risk and makes them more willing to lend.

In many cases, land is a strong form of collateral because it has clear value and can be checked through official records. For lenders, that makes the loan safer than lending without a backup.

How Land Becomes Collateral

Not every piece of land can be used the same way. A lender first checks the land’s value, ownership status, and legal condition.

Here are the main things they review:

- Clear title: The land must belong to you.

- Legal documents: The title deed and registry records should be valid.

- Market value: The land must be worth enough to support the loan.

- Land use type: Residential, commercial, rural, or agricultural land may all be treated differently.

A bank usually sends a valuer to inspect the property. The valuer looks at location, size, access roads, nearby development, and future growth potential. All of this helps the lender decide how much the land is worth.

Why Banks Accept Land as Security

Banks accept land because it lowers their risk. If the borrower defaults, the lender has a real asset tied to the loan.

This makes land-backed lending attractive for both sides:

- For the bank, the loan is safer.

- For you, the loan may come with better terms.

- For the project, it creates a path to start building sooner.

This is why land collateral is often used in construction financing and home building loans.

Can I Use My Land as Collateral to Build a House?

Direct Answer

Yes, in most cases, you can use your land as collateral to build a house.

However, approval depends on the lender’s rules and the condition of the land. Some lenders are flexible, while others have strict requirements. The land must usually be valuable, legally clear, and suitable for residential use.

So the real answer is: yes, but only if the land qualifies.

Key Conditions You Must Meet

Before a lender agrees, they will usually want the following:

-

- Clear ownership: Your name should be on the title deed or legal records.

- Approved land use. In many cases, the land should be zoned for residential construction.

- Proper valuation: The land must have enough market value to support the loan amount.

- No disputes or claims. The land should not be involved in court cases, family disputes, or unpaid taxes.

If even one of these points is missing, your application may be delayed or denied.

Loan Types That Allow It

Several loan types can use land as security:

- Construction loans

- Land equity loans

- Mortgage loans secured by land

- Bridge loans

- Special housing finance schemes

Each one works a little differently, but the idea is the same: the land helps reduce the lender’s risk.

Real-World Example

Imagine you own a residential plot, but you do not have enough savings to build property. You apply for a construction loan using the land as collateral. The bank checks the title, values the plot, reviews your income, and approves the loan in stages.

The money is released in stages as the house is built. In this way, your land becomes the key that helps you turn an empty plot into a real home.

Types of Loans You Can Get Using Land as Collateral

Construction Loans

A construction loan is one of the most common choices. It is designed specifically for building a house.

This type of loan is usually short-term. The lender does not give all the money at once. Instead, funds are released in stages as the build progresses.

For example, money may be released for:

- Foundation work

- Wall construction

- Roofing

- Finishing and final inspection

During the construction period, you may only pay interest on the amount already used. This can help reduce monthly pressure while the house is still unfinished.

Land Equity Loans

A land equity loan lets you borrow against the current value of your land.

This can be useful if you already own the land outright or have paid off most of it. Since the land has value, the lender may allow you to use that value to support your building plans.

This type of loan can be more flexible than a standard construction loan, but the lender still wants proof that the project is realistic and safe.

Mortgage Loan Against Land

In some cases, you can use the land to secure a mortgage-type loan.

This works well when the lender wants to move from land financing into a full home loan after construction is complete. Once the house is finished, the loan structure may change into a regular mortgage.

This option is often used by people who want a long-term repayment plan after the home is built.

Bridge Loans

A bridge loan is a short-term loan meant to cover a temporary gap.

For example, you may be waiting for another loan, waiting to sell another property, or waiting for permanent financing. A bridge loan helps you move forward without delay.

It is useful, but usually more expensive than other loans, so it should be used carefully.

Government or Bank Housing Schemes

Some banks and governments offer special housing programs to support home construction.

These programs may offer lower interest rates, more flexible payment plans, or easier eligibility requirements for certain applicants. But they often come with strict eligibility checks.

You may need to show:

- Income proof

- Land documents

- Approved house plans

- Compliance with local housing rules

Loan Comparison Table

Loan Type Main Use Best For Key Feature

Construction Loan Building a house in stages New home construction Funds released step by step

Land Equity Loan Borrowing against land value Landowners with paid-off land Flexible use of funds.

Mortgage Loan Against Land Long-term home financing Buyers planning full repayment later Can turn into a regular mortgage.

Bridge Loan Temporary financing Short-term funding gaps Fast but often costly

Housing Scheme Affordable home support Eligible applicants May offer lower rates or support

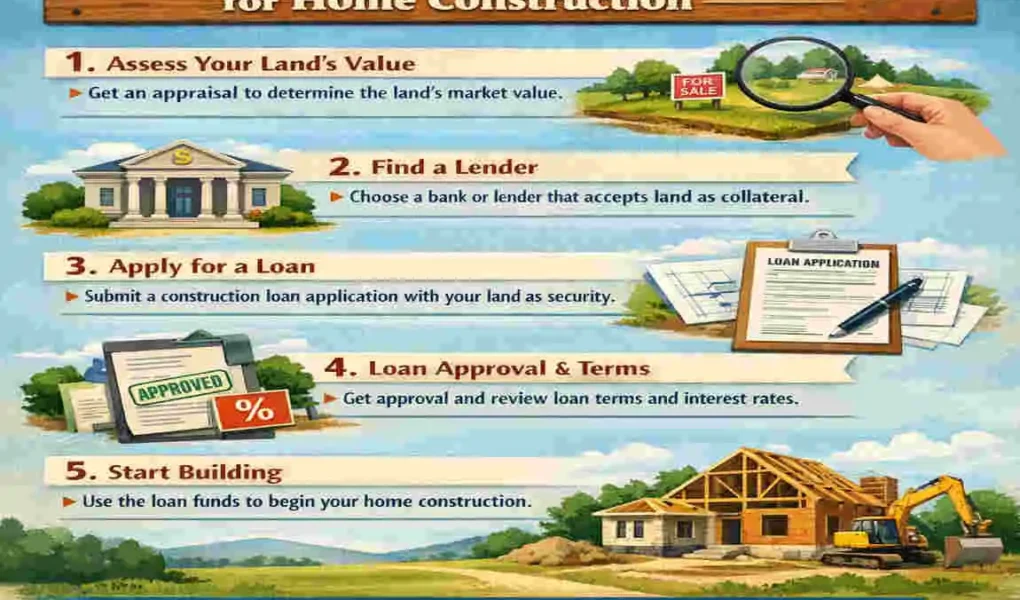

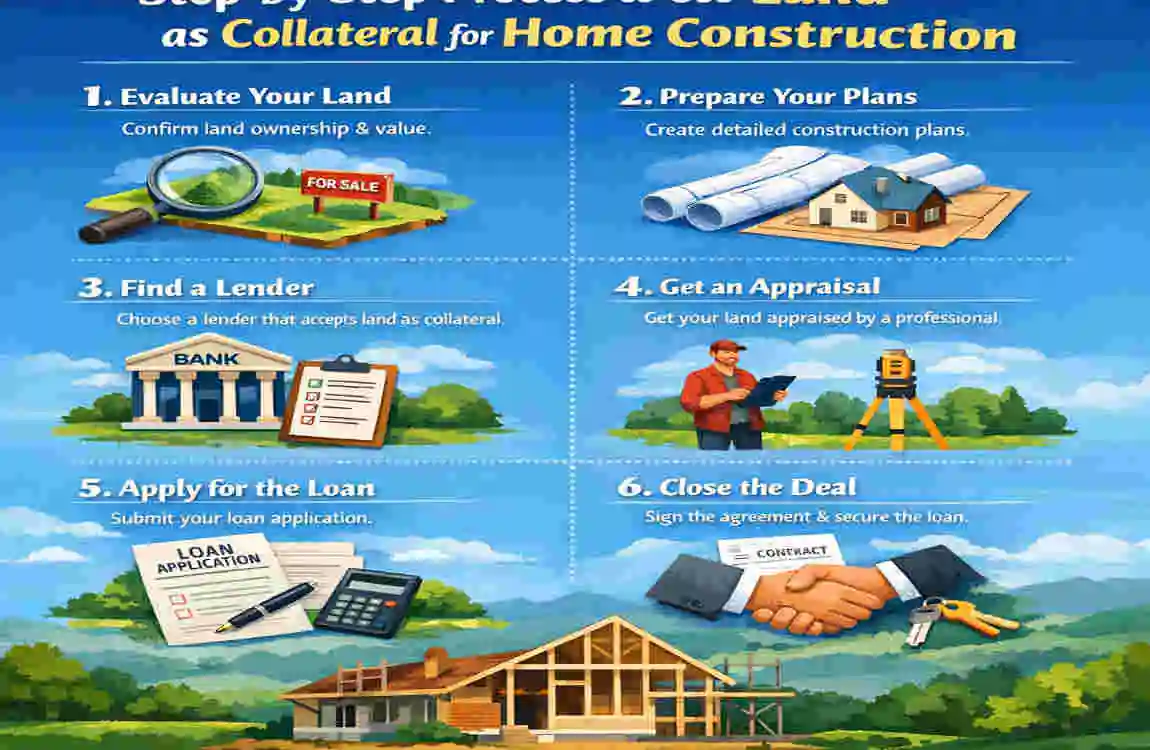

Step-by-Step Process to Use Land as Collateral for Home Construction

Verify Land Ownership

Start by checking your title deed and land records. Make sure your name is listed correctly and the documents are up to date.

If there are family claims, unpaid taxes, or unclear records, fix them first. A clean title makes the rest of the process much easier.

Get the Land Valued

Next, the land must be professionally appraised.

A bank-approved valuer usually checks:

- Location

- Size

- Access to roads

- Nearby services

- Current market demand

This valuation helps the lender decide how much money they can safely offer.

Prepare Your Construction Plan

Before applying, you should have a basic construction plan ready.

This usually includes:

- Architectural drawings

- Building permits

- Estimated project cost

- Timeline for the work

The more prepared you are, the more confidence the lender will have in your project.

Apply for the Loan

Now you can submit your application to the lender.

You will likely need to provide:

- Land title documents

- Identity documents

- Income proof

- Building plan

- Valuation report

- Bank statements

The lender will check both your land and your financial profile.

Review the Loan Terms

If the lender approves your application, read the loan terms carefully.

Pay close attention to:

- Interest rate

- Repayment period

- Disbursement schedule

- Late payment rules

- Penalties or fees

Do not rush this step. A small detail can affect your budget later.

Receive the Funds

In most construction loans, the full amount is not given at once.

Instead, the money is released in stages as work progresses. The lender may inspect the site before each new payment.

This protects both you and the lender by making sure the project stays on track.

Begin Construction

Once the funds are released, construction can begin.

Hire trusted professionals, follow the approved plan, and keep all receipts and records. Good communication with your contractor is important because delays can quickly raise costs.

Simple Checklist for the Process

- Confirm ownership

- Appraise the land

- Prepare construction plans

- Apply for the right loan

- Review the terms carefully

- Follow the disbursement process

- Start building with proper oversight

Eligibility Criteria and Requirements

Financial Requirements

Lenders want to know that you can repay the loan. That is why they review your income, savings, and credit history.

They may check:

- Stable monthly income

- Good credit score

- Healthy debt-to-income ratio

- Evidence of repayment ability

If your income is irregular, you may still qualify, but the lender may ask for extra proof or a co-borrower.

Legal Requirements

Your land documents must be valid and complete.

This usually means:

- Registered title deed

- No legal disputes

- No hidden claims

- Up-to-date tax records

If the property has legal problems, the lender may pause the process until they are solved.

Technical Requirements

The lender also wants to know that the house can actually be built.

This is why they may ask for:

- Approved house plan

- Building permit

- Construction feasibility report

- Cost estimate from a contractor

These documents show that the project is practical and well planned.

Advantages of Using Land as Collateral

Using land as collateral can offer several strong benefits.

- Easier approval than many unsecured loans

- Lower interest rates in some cases

- Higher borrowing limits

- Better use of idle land

- A chance to build long-term wealth

If the land has been sitting unused, this approach can turn it into something productive. Instead of staying empty, it becomes the base for a home and a future asset.

Risks and Challenges to Consider

Risk of Loan Default

The biggest risk is defaulting on the loan.

If that happens, the lender may have the right to take the land. That is why you should borrow only what you can realistically handle.

Market Value Fluctuations

Land values can rise or fall. If the market changes, it may affect how much the lender is willing to offer.

A strong location usually helps, but no asset is completely free from market risk.

Construction Delays

Delays can increase costs fast. Materials may become more expensive, labor costs maycosts may rise, and your budget may get stretched.

If you do not plan for delays, the loan may not be enough to finish the home.

Legal and Documentation Issues

Paperwork property problems are common. A missing title record, zoning issue, or unpaid tax can slow everything down.

This is why legal review matters before you apply.

Common Mistakes to Avoid

Many people make avoidable mistakes when trying to use land for financing.

- Not checking the title status

- Underestimating construction costs

- Choosing the wrong lender

- Ignoring interest terms

- Skipping permits and approvals

A little preparation can save you a lot of stress later.

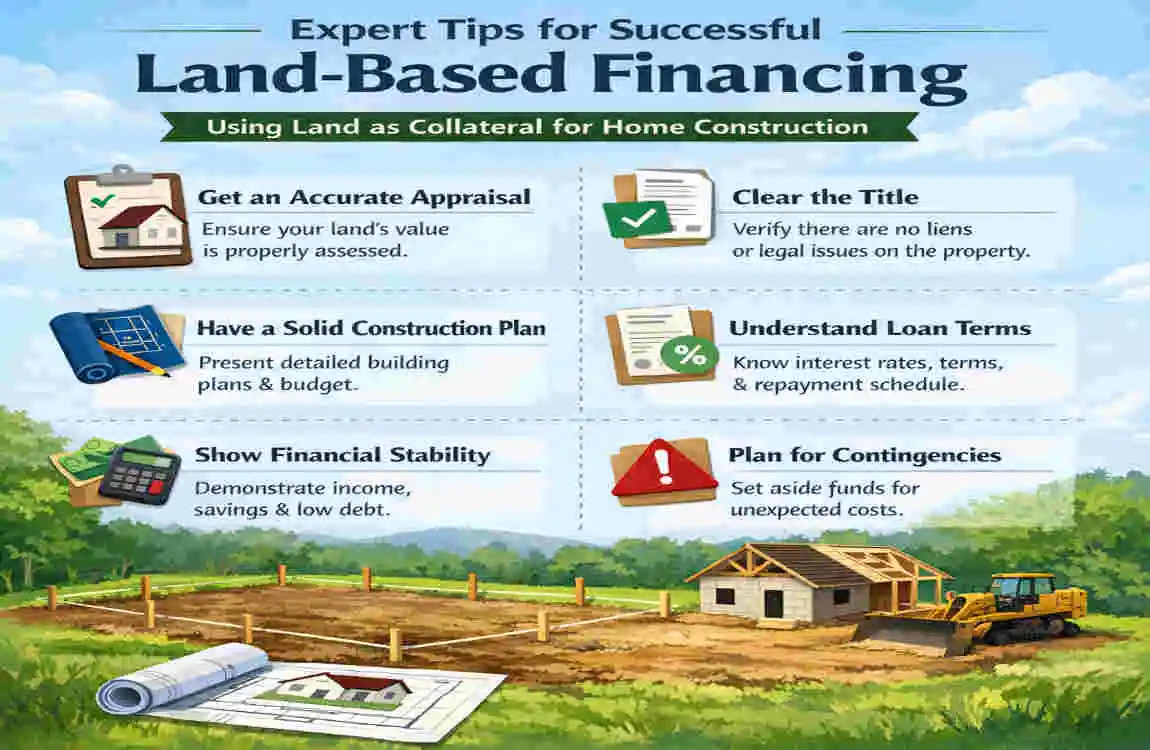

Expert Tips for Successful Land-Based Financing

If you want better results, keep these tips in mind:

- Compare multiple lenders before choosing one.

- Get a professional appraisal to determine the land’s true value.

- Keep your credit in good shape to improve approval chances.

- Work with licensed architects and contractors.

- Set aside a contingency budget of about 10–15% for surprises.

These small steps can make the loan process smoother and help your project stay on budget.

Alternatives If You Can’t Use Land as Collateral

If your land does not qualify, do not panic. You still have options.

- Personal loans

- Joint financing with family

- Government housing programs

- Builder financing plans

- Saving-based construction over time

These alternatives may take longer or offer smaller amounts, but they can still help you move forward.

Frequently Asked Questions

Can I use my land as collateral to build a house without income proof?

Usually, lenders want some proof of income. If you cannot show regular income, approval may be harder. Some lenders may accept other proof, but it depends on their policy.

How much loan can I get against my land?

That depends on the land’s value, location, and the lender’s rules. In many cases, the loan amount is a percentage of the appraised value, not the full value.

Do banks accept agricultural land as collateral?

Some banks do, but not all. Agricultural land may face additional checks due to zoning, use restrictions, and resale value.

What happens if I fail to repay the construction loan?

If you default, the lender may begin legal recovery steps and may take the land under the loan agreement.

Is it better to sell land or use it as collateral?

It depends on your goals. If you want to keep the land and build a home, using it as collateral may be a better option. If you need full cash and do not plan to build, selling could make more sense.