Buying a home through a traditional mortgage is not always easy. Banks often require strong credit, steady income, extensive paperwork, and a lengthy approval process. For many people, that becomes a major roadblock.

That is where in-house financing real estate comes in. If you have ever wondered what house financing in real estate is, the simple answer is that it is a way to buy property without going through a bank. Instead, the seller, developer, or property owner finances the purchase directly.

| Term / Concept | What It Means | Key Feature in No‑Bank Buying |

|---|---|---|

| In‑house (owner) financing | The home seller acts as the lender and finances part or all of the purchase. | No traditional bank mortgage is used. |

| Buyer–seller agreement | Buyer and seller sign a contract where the buyer repays the seller in installments plus interest or a fixed premium. | More flexible terms than a bank. |

| No‑bank home buying | Buying a home without a mortgage from a bank or standard lender. | Often uses seller financing, cash, or private loans. |

| Typical structure (installments) | Buyer pays a down payment to the seller, then monthly payments until the balance is paid off. | Similar to a mortgage, but the seller is the lender. |

| Pros for buyer | Easier approval, faster closing, and often negotiable interest or down payment. | Helpful if credit or bank financing is hard to get. |

| Risks for buyer | If you default, the seller can foreclose or reclaim the property. | Terms depend entirely on the seller’s contract. |

This option can help first-time buyers, people with low credit scores, self-employed buyers, foreign buyers, and real estate investors. It can also make home buying faster and more flexible.

What Is In-House Financing Real Estate?

Simple Definition of In-House Financing

In-house financing means the seller or developer acts like the lender. Instead of borrowing money from a bank, the buyer makes payments directly to the seller.

This is also known in many cases as seller financing real estate or owner financing homes. The setup is usually more flexible than a bank loan, but the terms can vary a lot from one deal to another.

How It Works in Real Estate Transactions

The process usually starts when you choose a property that offers this option. Then you and the seller agree on the price, down payment, interest rate, and monthly payment plan.

After that, you sign a legal agreement. This may include a promissory note and a purchase contract. Once the deal is active, you make monthly payments directly to the seller.

In many cases, the title may transfer right away, or it may transfer after the full balance is paid. That depends on the type of agreement used.

Difference Between Traditional Mortgages and In-House Financing

A traditional mortgage goes through a bank, credit union, or lender. In-house financing skips that step.

Here is the main difference:

- Bank loan: stricter approval, more paperwork, longer wait

- In-house financing: more flexible approval, faster closing, less paperwork

Traditional loans usually have lower interest rates, but they can be harder to qualify for. In-house financing can be easier to access, but it may cost more over time.

How In-House Financing Works Step by Step

Find Properties That Offer It

You may find these deals through real estate developers, private sellers, land sales companies, or owner-financed listings. Some buyers search specifically for no bank home buying options to find these properties faster.

Step 2: Negotiate the Terms

This is where the deal becomes personal. The seller may let you negotiate:

- Down payment amount

- Interest rate

- Loan length

- Balloon payment terms

The more flexible the seller is, the easier it may be to build a payment plan that fits your budget.

Sign the Agreement

You should always get everything in writing. A proper deal usually includes a purchase contract, a promissory note, and any required legal disclosures.

Never rely on a verbal promise. If something is not written down, it can be hard to prove later.

Make Monthly Payments

Once the deal is active, you send payments to the seller instead of a bank. Some sellers accept automatic transfers, checks, or online payments.

Be sure to ask about late fees, payment due dates, and who handles taxes and insurance.

Complete the Ownership Transfer

When the balance is fully paid, the property title is usually transferred to you if it was not already in your name. In some cases, buyers later refinance into a traditional mortgage once their credit improves.

Types of In-House Financing in Real Estate

Seller Financing

This is one of the most common forms. The home’s owner becomes the lender and receives monthly payments from the buyer.

It is often used in residential deals where the seller wants to move quickly and avoid a long bank process.

Rent-to-Own Agreements

With rent-to-own homes, part of your rent may go toward the future purchase price. This can help buyers build a path to ownership while living in the home first.

This option is useful if you need time to improve credit or save for a larger down payment.

Lease Purchase Agreements

A lease purchase is similar to rent-to-own, but it usually includes a stronger commitment to buy the home later.

You lease the property now, but the agreement sets a future purchase date or price.

Developer Financing

Some builders offer developer financing homes directly, especially in new communities. This can make it easier to buy a newly built home without using a bank.

Land Contracts

Under a land contract, the seller retains legal title until the buyer completes payment. The buyer may gain equitable ownership during the payment period.

This can be a useful option, but it also requires careful contract review.

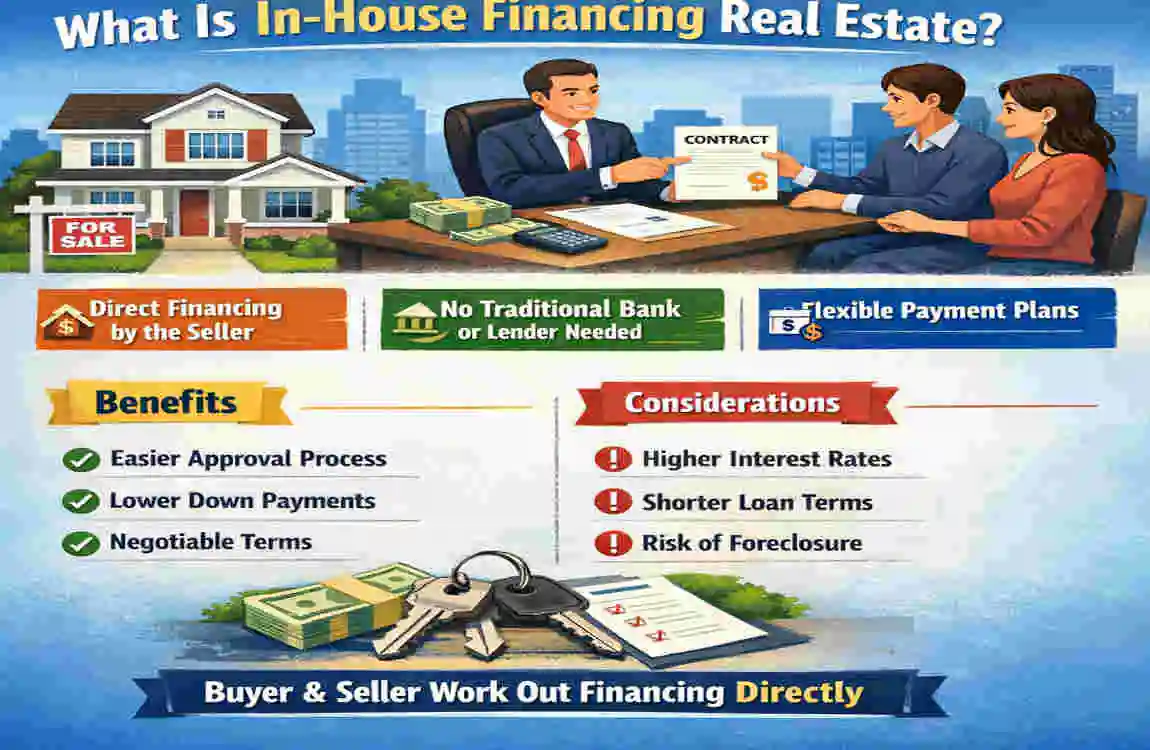

Benefits of In-House Financing Real Estate

Easier Approval Process

One of the biggest benefits is flexibility. Sellers may care less about strict credit scores and more about your ability to make payments.

This helps buyers who may not fit the usual bank rules.

Faster Closing Times

Because there is less paperwork and fewer outside parties involved, deals can close quickly. That makes in-house financing useful when speed matters.

Flexible Terms

The buyer and seller can often agree on terms that suit both sides. That may include custom payment schedules or a negotiated interest rate.

This flexibility is one reason many people look at alternative mortgage options.

Helpful for Buyers with Poor Credit

If your credit history is not strong, in-house financing may give you a second chance. It can also help you build a better financial record over time.

Lower Upfront Costs

In some cases, the closing costs are lower because bank fees are reduced or removed. That can make it easier to get started.

Useful for Self-Employed Buyers

Self-employed people often have irregular income or tax returns that do not fully reflect their earnings. In-house financing may be easier for them because the review process is more personal.

Risks and Disadvantages of In-House Financing

Higher Interest Rates

Because the seller assumes more risk, the interest rate may be higher than that of a traditional mortgage. That means you may pay more over the life of the loan.

Balloon Payment Risk

Some agreements include a balloon payment, which is a large final payment due at the end of the term. This can be hard if you are not prepared.

Limited Consumer Protection

Bank loans are highly regulated. In-house deals may have fewer protections, so you need to read every detail carefully.

Property May Be Overpriced

Some sellers raise the property’s price to offset financing costs. That is why comparing the home value is important.

Risk of Default

If you miss payments, you may face penalties, loss of the property, or eviction depending on the agreement. This makes payment planning essential.

Shorter Loan Terms

Many in-house deals have shorter repayment periods than standard mortgages. That can lead to higher monthly payments.

Who Should Consider In-House Financing?

First-Time Homebuyers

If you are struggling to qualify for a bank loan, this can be a helpful starting point.

Buyers with Bad Credit

It can pave the way to homeownership while you rebuild your credit.

Real Estate Investors

Investors may use it to buy properties quickly without waiting for bank approval.

Self-Employed Individuals

If your income is difficult to document, this option may be a better fit than traditional lending.

Foreign Buyers

Some foreign buyers use in-house financing because they lack a U.S. credit history.

Requirements for In-House Financing Real Estate

Basic Documents You May Need

Most sellers still want proof that you can pay. Common documents include:

- Pay stubs

- Bank statements

- Tax returns

- Government ID

Down Payment Expectations

The down payment is often negotiable, but it is usually required. It may be lower than a bank down payment in some cases, but not always.

Credit Checks and Employment Verification

Some sellers do light credit checks. Others focus more on income history and job stability. Self-employed buyers may be asked for alternative proof, such as bank records or business income statements.

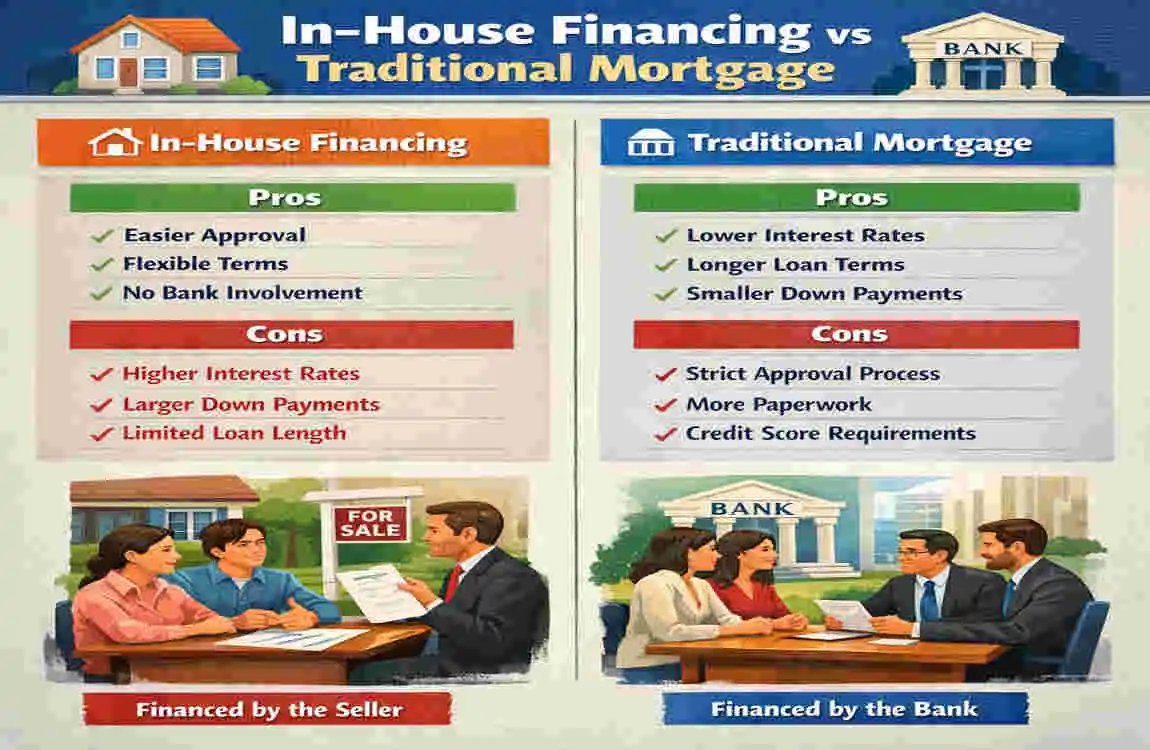

In-House Financing vs Traditional Mortgage

Feature In-House Financing Traditional Mortgage

Approval Speed Faster Slower

Credit Requirements Flexible Strict

Interest Rates Higher Lower

Down Payment Negotiable More standard

Loan Terms Flexible Fixed

Paperwork Minimal Extensive

Regulation Less regulated Highly regulated

Which Option Is Better?

It depends on your goals.

If you want lower long-term cost, a traditional mortgage is often better. If you need faster approval and more flexibility, in-house financing may be the better choice.

Important Questions to Ask Before Signing

Before you agree to any deal, ask these questions:

- What is the interest rate?

- Is there a balloon payment?

- Who pays property taxes and insurance?

- What happens if I miss a payment?

- Are there prepayment penalties?

- Has a lawyer reviewed the agreement?

These questions can help you avoid surprises later.

Legal Considerations and Buyer Protection

Always Use Written Contracts

Never trust a handshake deal. A written contract protects both parties and clarifies the agreement.

Hire a Real Estate Attorney

A lawyer can review the deal and point out hidden risks. This step is especially helpful if the contract language feels confusing.

Verify Property Ownership

Make sure the seller truly owns the property and has the legal right to offer financing.

Understand Local Laws

Rules for in-house financing can differ by state or region. Local law may affect your rights and responsibilities.

Tips for Using In-House Financing Successfully

Improve Your Credit While Paying

If you plan to refinance later, keep improving your credit score throughout the loan term.

Keep Good Records

Save every receipt, payment confirmation, and contract copy. This makes it easier to prove your payment history.

Negotiate Before You Sign

Try to get the best deal possible upfront. Small changes in interest rate or payment length can make a big difference.

Stay Alert for Bad Deals

If something feels too easy or too expensive, slow down and check the details. Good deals should still make sense.

Common Myths About In-House Financing Real Estate

“It Is Only for People with Bad Credit”

Not true. Many buyers use it because they want flexibility, speed, or a simpler process.

“It Is Illegal or Unsafe”

It is not illegal when done properly. It only becomes risky when people skip contracts or ignore legal advice.

“You Do Not Need a Contract”

You absolutely do. A contract is one of the most important parts of the deal.

“All Seller Financing Is Expensive”

Not always. Some deals are fair and workable, especially when both sides want a smooth sale.

Frequently Asked Questions

Is in-house financing the same as seller financing?

They are closely related. In many cases, yes, they mean the same thing.

Can I buy a house with no bank loan?

Yes. That is one of the main benefits of in-house financing and other no-bank home-buying methods.

Do I need good credit?

Not always. Many sellers are more flexible than banks.

Is in-house financing safe?

It can be safe if the contract is clear, the property is verified, and a lawyer reviews the deal.

Can I refinance later?

Yes, many buyers do this after improving credit or income stability.

What happens if I miss payments?

You may face late fees, default, or loss of the property depending on the agreement.

Are interest rates higher?

Often yes, but not always. It depends on the seller and the risk involved.