Buying a home is already a big decision. When you are married in Texas, it can feel even more confusing because Texas community property law changes how ownership works.

| Topic | Quick Explanation |

|---|---|

| Can a spouse buy a house alone in Texas? | Yes, under certain circumstances, a spouse can purchase a house without the other spouse being on the mortgage or title. |

| Texas Community Property Law | Texas is a community property state, meaning assets acquired during marriage may belong to both spouses. |

| Separate Property Exception | A house bought with separate property funds (owned before marriage, inheritance, or gifts) may remain separate property. |

| Mortgage vs Title | A spouse can be on the title without being on the mortgage, or vice versa. |

| Homestead Rules | If the property is a marital homestead, Texas law usually requires both spouses to consent to selling or refinancing. |

Many people ask: Can a spouse buy a house without the other in Texas? The short answer is yes, sometimes. But that does not always mean the other spouse has no rights. Texas law considers factors such as where the money came from, how the property is titled, whether the home is a homestead, and what the lender requires.

Understanding Texas Community Property Laws

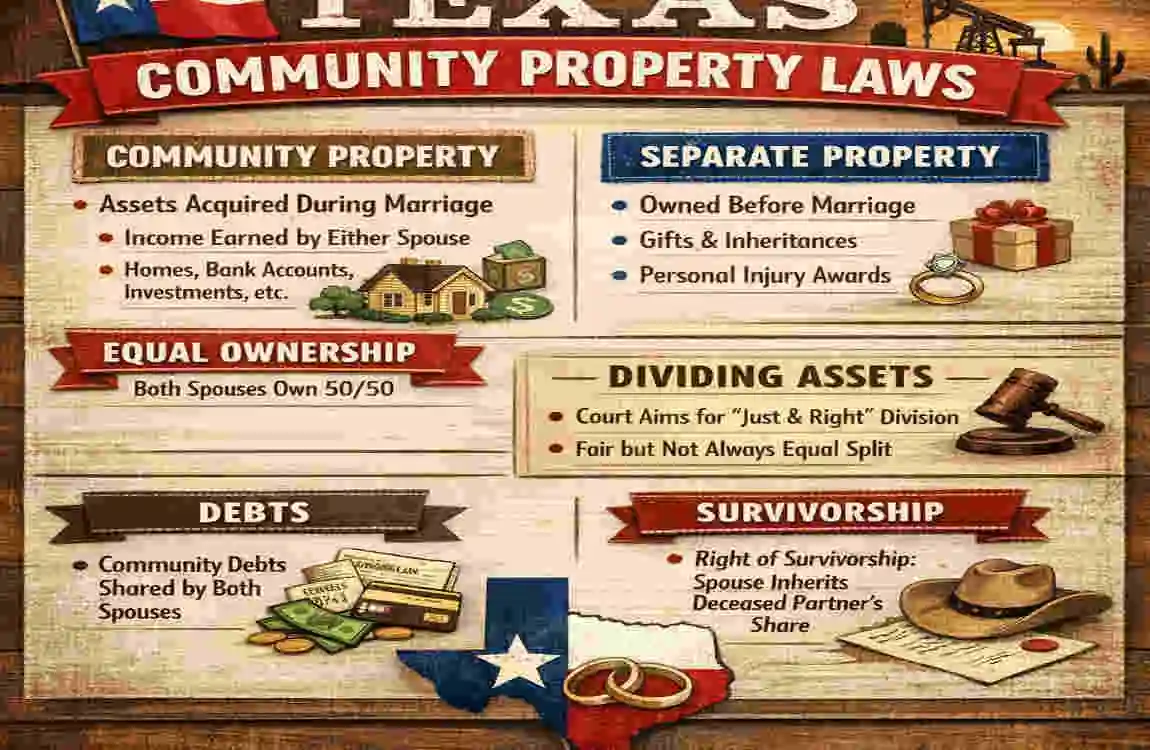

What Is Community Property in Texas?

Texas is a community property state. That means most property acquired during marriage is usually treated as belonging to both spouses.

In simple terms, if a married couple buys something during the marriage, Texas often treats it as part of the marriage property unless there is proof that it is separate property. That includes real estate in many cases.

So even if only one spouse signs the paperwork, the other spouse may still have a legal interest depending on the facts.

Separate Property vs Community Property

Not all property is shared property. Texas also recognizes separate property.

Separate property usually includes:

- Property owned before marriage

- Inheritance

- Gifts received by one spouse only

This matters because if one spouse uses separate property funds to buy a house, that home may be easier to treat as separate property too. But the money must usually be traced clearly. If funds get mixed with joint money, the line becomes blurry.

That is why records matter so much.

Why Texas Real Estate Laws Matter for Married Couples

Texas real estate law affects more than just buying a house. It can affect:

- Divorce

- Taxes

- Inheritance

- Debt collection

- Liability

- Future refinancing

If you are married and buying property, you should not assume the title alone tells the whole story. In Texas, ownership rights can be more complicated than they look on paper.

Can a Spouse Buy a House Without the Other in Texas?

The Short Answer

Yes, a spouse can sometimes buy a house alone in Texas.

But there is an important difference between:

- Being on the mortgage

- Being on the title or deed

A spouse may buy property in only their name. However, the other spouse may still have certain rights depending on the type of property, the source of funds, and whether the home is protected as a homestead.

So, if you are asking, “Can a married person buy a house alone in Texas?” the answer is yes, but with limits.

When a Spouse Can Buy Alone

A spouse may be able to buy alone when:

- The purchase uses separate property funds

- Only one spouse qualifies for the mortgage

- The property is an investment property

- The spouses have a valid agreement saying the home is separate

This can happen when one spouse wants to keep the purchase in their own name for financial or legal reasons.

Situations Where Consent May Still Be Required

Even if one spouse wants to buy alone, consent may still matter in some cases.

For example:

- Homestead property rules may require both spouses to sign certain documents

- Selling or refinancing the marital home may need both signatures

- A lender may ask for spouse’s consent under Texas real estate rules or disclosures

So while one spouse may buy, the process is not always fully independent.

Can One Spouse Be Left Off the Mortgage?

Yes, one spouse can sometimes be left off the mortgage. That means only one spouse is responsible for the loan payments.

Lenders usually look at:

- Income

- Credit score

- Existing debt

- Debt-to-income ratio

This can help if one spouse has stronger finances. But it can also create risk. If only one spouse is on the mortgage, that person carries the loan burden, even if both spouses live in the home.

Understanding Homestead Laws in Texas

What Is a Homestead Property?

A homestead is the home a family uses as its main residence. Texas gives strong legal protection to homestead property.

This protection is one reason people often ask about Texas homestead law spouse consent. The law is designed to protect the family home from being taken too easily or sold without proper approval.

Why Homestead Rights Are Important

Homestead rights matter because they can protect the home from some creditors. They can also protect a spouse from losing housing rights without warning.

In other words, even if one spouse tries to handle everything alone, Texas law may still protect the other spouse in a homestead situation.

Can One Spouse Sell or Mortgage a Homestead Alone?

Usually, no.

For a homestead, both spouses often need to sign important documents, especially for:

- Selling the home

- Taking out a mortgage

- Refinancing the property

- Creating certain liens

If one spouse tries to do this alone, the action may be challenged later. That is why homestead rules are such a big issue in Texas property deed laws.

Mortgage vs Property Title: Important Differences

Being on the Mortgage

Being on the mortgage means being responsible for the loan. If payments are missed, the lender can pursue the borrower.

Being on the Deed

Being on the deed means having ownership rights in the property. This is about legal title, not loan duty.

Can a Spouse Be on Title But Not Mortgage?

Yes, this happens often.

For example, one spouse may qualify for the loan, but both spouses may be named on the deed. That means one spouse is responsible for paying, but both may own the home.

Risks of Excluding a Spouse

Leaving a spouse off the deed or mortgage can lead to problems like:

- Ownership disputes

- Credit issues

- Divorce complications

Here is a simple look at the difference:

Situation Mortgage Title/Deed Ownership Rights

One spouse only, One spouse, Limited/shared depending on law

Both spouses Both spouses Both spouses Shared ownership

The table shows why title and mortgage should never be confused. They do different jobs.

How to Buy a House Alone Legally in Texas

Use Separate Property Funds

If you want to keep the purchase separate, start with clear money records. Show where the funds came from and avoid mixing them with joint money.

Consider a Prenuptial or Postnuptial Agreement

A valid agreement can clearly explain what belongs to whom. This can reduce future conflict and make ownership easier to prove.

Work With a Real Estate Attorney

This is one of the smartest steps you can take. A lawyer can explain your rights and help you avoid mistakes.

Talk to Your Mortgage Lender

Ask the lender whether your spouse must sign anything. Rules can change based on the type of loan and how the property will be used.

Keep Financial Records Organized

Save all records related to the purchase.

Documents you may need:

- Proof of separate funds

- Marriage agreements

- Mortgage approval letter

- Property deed paperwork

These documents can help show how the home should be classified later.

Scenarios Where Buying Alone Makes Sense

One Spouse Has Better Credit

This is one of the most common reasons.

If one spouse has a stronger credit score, the loan may be easier to approve. It may also lead to a lower interest rate. That can save money over time.

Protecting Property From Debt Issues

Sometimes one spouse wants to keep a purchase separate because of debt concerns. This may involve:

- Student loans

- Credit card debt

- Business liabilities

If done correctly, separate ownership may help reduce exposure. But it must be handled carefully.

Real Estate Investment Purchases

A spouse may want to buy a rental property or second home as an investment. In that case, keeping the property in one name may be part of a business plan.

Some couples also use an LLC or other ownership structure. This can help with business and legal planning, but it should be reviewed carefully.

Separation or Marital Problems

If a couple is separated or heading toward divorce, one spouse may try to buy alone. That can be legal, but it may later be reviewed under Texas divorce property laws.

Estate Planning Reasons

Some people buy alone for inheritance planning or asset control. This can make sense, but it should be matched with a proper estate plan.

Legal Risks of Buying a House Without Your Spouse in Texas

Community Property Claims

Even if one spouse buys the home, the other spouse may still claim an interest if the property was bought during the marriage with marital funds.

That is why spouse property rights in Texas matter so much.

Divorce Complications

If the marriage ends later, the home may be included in the divorce property division. The court may look at:

- Who paid for it

- When it was bought

- What money was used

- Whether it became community property

This can lead to reimbursement claims or ownership disputes.

Inheritance and Probate Problems

If one spouse dies, ownership questions can become even harder. Without proper estate planning, the surviving spouse or heirs may face probate issues.

Mortgage and Debt Liability Risks

If only one spouse signs the mortgage, that spouse is legally responsible for the debt. But if the home is community property, the other spouse may still be affected.

Fraud or Hidden Purchases

Trying to hide a home purchase from a spouse can create serious legal problems. Courts may closely examine hidden assets in a Texas marriage, especially if money was used without disclosure.

Expert Tips Before Buying Property Alone in Texas

Communicate With Your Spouse

Even if the law may allow a solo purchase, talking openly can prevent conflict later.

Understand Long-Term Financial Impact

Think about taxes, credit, and estate planning. A house is not just a purchase. It is a long-term legal and financial commitment.

Consult Professionals

Before moving forward, speak with:

- A realtor

- A mortgage advisor

- A real estate attorney

- A CPA

These professionals can help you avoid costly mistakes.

Frequently Asked Questions

Can my husband buy a house in Texas without me?

Yes, he may be able to. But whether the home becomes community property depends on the funds used, the title, and Texas marital property laws.

Can my wife be on the deed but not the mortgage?

Yes. That is common. She may own part of the home without being legally responsible for the loan.

Does Texas require both spouses on a mortgage?

Not always. Lenders may allow one spouse to borrow on their own. However, they may still ask for information about the other spouse or require disclosures.

Can a spouse secretly buy property in Texas?

It is possible, but doing so can lead to disputes later. A hidden purchase may still be subject to ownership claims if marital funds were used.

What happens if we divorce after one spouse buys a house?

The court may treat the house as community property if it was purchased during the marriage with shared funds. That can affect the division in a divorce.

Can separate property become marital property in Texas?

Yes, it can happen through commingling. If separate money is mixed with marital money, it may become harder to prove what is separate.

Does a non-buying spouse still own part of the house?

Maybe. It depends on the source of funds, the title, and whether Texas community property rules apply.