If you are asking what an AVM in real estate is, the simple answer is this: an AVM is an Automated Valuation Model. It is a computer-based tool that estimates a property’s value using data such as recent sales, property details, and market trends.

People use AVMs because they are fast, convenient, and easy to access. Homeowners use them to check home value, buyers use them to compare properties, sellers use them for pricing ideas, and investors use them to screen deals.

Still, an AVM is only an estimate. It is helpful, but it is not always the final word on a home’s value. That is why understanding how it works matters.

What Is AVM in Real Estate?

Definition of AVM

An AVM means Automated Valuation Model. In real estate, it is a digital system that estimates a home’s market value.

It works by studying data and comparing the property with similar homes. The goal is to give a quick value estimate without needing a person to visit the house first.

How AVMs Estimate Property Value

AVMs look at several things, including:

- Public records

- Comparable home sales

- Property characteristics

- Market trends

For example, a larger home in a popular neighborhood may get a higher estimate than a smaller home in a less active market. The model uses patterns from past sales to make a prediction.

How Does an AVM Work?

Data Sources Used

AVMs collect information from different sources, such as:

- Tax records

- MLS data

- Sales history

- Neighborhood data

The more complete the data, the better the estimate usually is.

Technology Behind AVMs

AVMs use algorithms, artificial intelligence, machine learning, and statistical analysis.

That sounds complex, but the idea is simple: the system learns from extensive property data and then predicts value based on those patterns.

Why AVMs Are Important in Real Estate

Benefits for Home Buyers

If you are buying a home, an AVM can give you a quick idea of whether the asking price looks fair. It can help you compare homes faster.

Benefits for Home Sellers

If you are selling, an AVM can give you a starting point for pricing. That can help you avoid setting the price too high or too low.

Benefits for Investors

Investors use AVMs to spot potential deals quickly. This saves time when reviewing many properties.

Benefits for Mortgage Lenders

Lenders use AVMs to help assess risk and support lending decisions, especially when they need a fast value estimate.

What Factors Affect an AVM Estimate?

Property Size

Larger homes usually have higher estimated values, especially when the layout and lot size are strong as well.

Home Age and Condition

A newer home or a well-maintained home may get a better estimate than an older one that needs repairs.

Recent Comparable Sales

AVMs rely heavily on recent sales of similar homes nearby. These sales help the system understand the local market.

Market Conditions

If home prices are rising, the AVM may show a higher estimate. If the market is slowing down, the value may be lower.

Property Location

Location matters a lot. A home in a strong school district or a desirable area may be worth more than a similar home elsewhere.

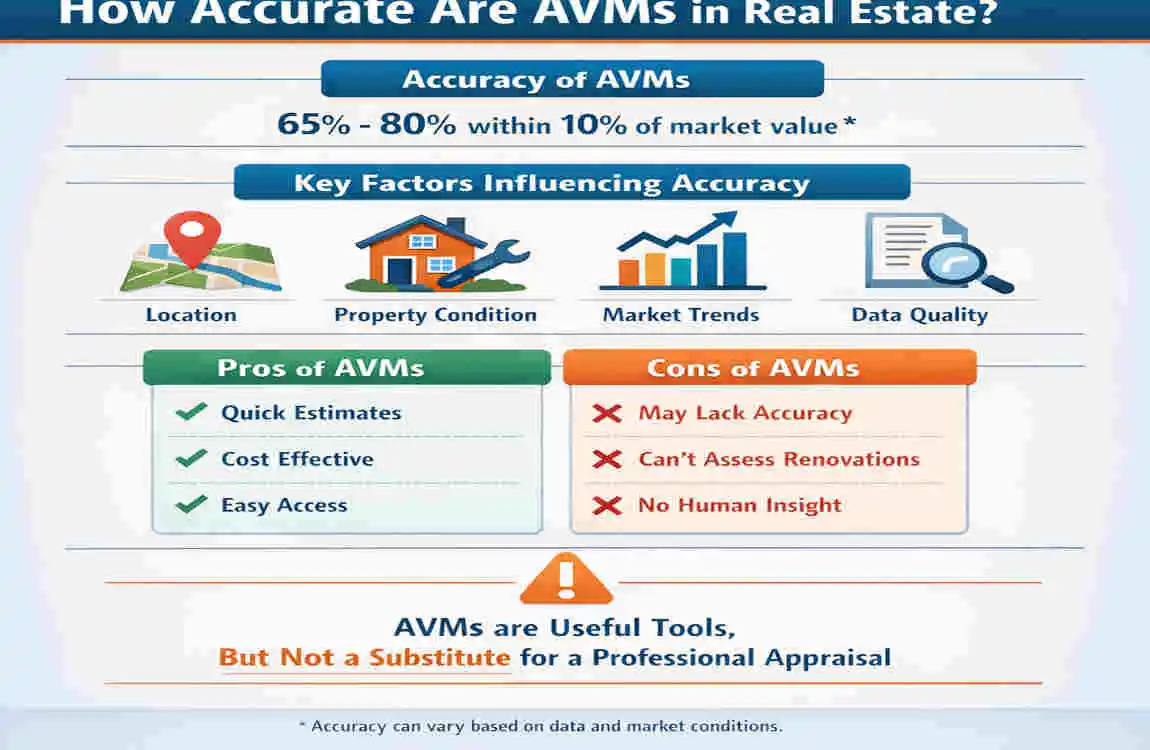

How Accurate Are AVMs?

When AVMs Are Most Accurate

AVMs work best in areas with many recent sales and standard home types. In those markets, the data is rich and easy to compare.

Situations Where AVMs May Be Less Reliable

AVMs may be less accurate for:

- Unique homes

- Rural properties

- Homes with major upgrades

- Properties with poor data records

Why Estimates Can Differ

Different websites may show different values because they use different data sources, update schedules, and formulas. That is why you may see more than one home value online.

Advantages and Disadvantages of AVMs

Table: AVM Pros and Cons

AdvantagesDisadvantages

Fast results Cannot inspect property condition

Free on many websites May miss renovations

Data-driven Accuracy varies by market

Easy to compare homes Limited in rural areas

AVM vs Professional Home Appraisal

Key Differences

An AVM and a home appraisal are not the same.

AVM vs. Home Appraisal

Automated Performed by a licensed appraiser

Instant estimate Physical inspection

Lower cost More accurate

Good for research Used for lending decisions

A home appraisal is usually more reliable because the appraiser looks at the property in person. An AVM is better for quick research.

Common Uses of AVMs

Buying a Home

Buyers use AVMs to understand if a listing price feels reasonable.

Selling a Property

Sellers use AVMs to set a starting price before speaking with an agent.

Mortgage Refinancing

Lenders and homeowners may use AVMs during refinancing research.

Investment Analysis

Investors use them to compare many properties in a short time.

Portfolio Management

Property owners with multiple homes can use AVMs to track value changes over time.

Tips for Using AVMs Wisely

- Compare multiple AVM estimates

- Review recent comparable sales

- Consider home upgrades

- Talk to a local real estate professional

- Get a professional appraisal for major decisions

Helpful Tip

Use AVMs as a starting point, not the final answer. They are useful for quick checks, but they should not replace deeper research.

Common Myths About AVMs

AVMs Are Always Accurate

Not true. AVMs can be helpful, but they are not perfect.

AVMs Replace Appraisers

Also not true. Appraisers still matter, especially for loans and major financial choices.

Every Website Gives the Same Estimate

No. Different platforms use different data and models.

AVMs Consider Interior Condition

Usually not very well. An AVM may not know about a remodeled kitchen, water damage, or other interior issues.

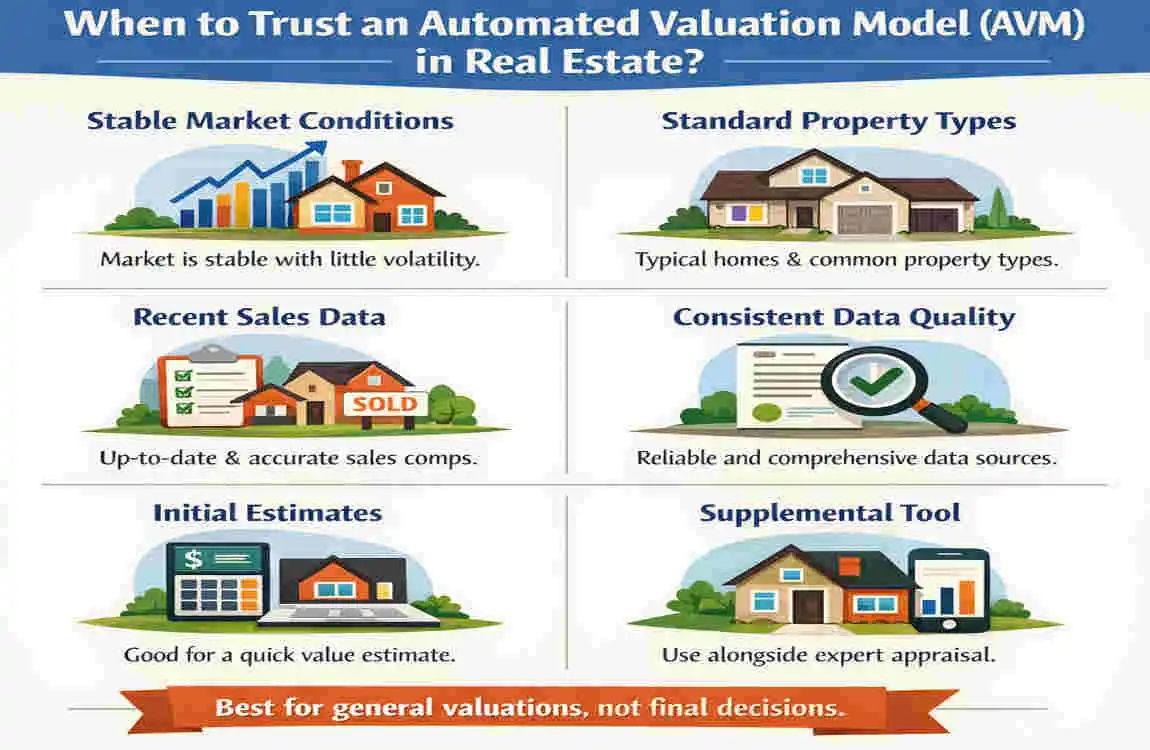

When Should You Trust an AVM?

You can trust an AVM for:

- Initial pricing research

- Market comparisons

- Investment screening

- Quick online home value checks

But for big decisions, like selling a home or refinancing a mortgage, a professional appraisal is usually the smarter choice.

Frequently Asked Questions

What is an AVM in real estate?

An AVM is a computer system that estimates a property’s value using data and recent sales.

How accurate is an AVM?

It can be fairly accurate in active markets, but less reliable for unique or rural homes.

Is an AVM the same as a home appraisal?

No. An AVM is automated, while an appraisal is done by a licensed professional who inspects the property.

What information does an AVM use?

It uses public records, sales history, tax data, property details, and neighborhood information.

Can I rely on an AVM before selling my house?

Yes, for early research. But for final pricing, a real estate professional or appraisal is better.

Why do different AVM websites show different values?

Because each one uses different data sources, formulas, and update timing.

| Topic | Information |

|---|---|

| What Is AVM? | AVM (Automated Valuation Model) is a technology-based tool that estimates a property’s market value using data and algorithms. |

| How It Works | It analyzes recent home sales, property features, location, market trends, tax records, and public data. |

| Main Purpose | To provide a fast estimate of a home’s current market value without a physical inspection. |

| Common Users | Homebuyers, sellers, real estate agents, lenders, investors, and online real estate platforms. |

| Advantages | Quick results, low cost, easy access, and useful for initial property research. |