If you are running a plumbing business, you may be asking Do I need plumber insurance. The simple answer is yes, in most cases, you do.

Plumbing work comes with real risks. You may damage a pipe, flood a room, injure yourself on a job site, or face a customer claim. Even a small mistake can become a big expense.

What Is Plumber Insurance?

Definition of plumber insurance

Plumber insurance is a group of business policies that help cover the risks plumbers face on the job.

It can protect you if you accidentally damage property, cause an injury, lose tools, or face a lawsuit. Think of it as a safety net for your plumbing business.

Why plumbers face unique risks

Plumbers work in homes, offices, and construction sites. That means you deal with water, tools, pipes, fixtures, and sometimes heavy equipment.

A small mistake can lead to a big problem. For example, a burst pipe can damage walls, floors, and furniture. A dropped tool can injure someone. A service van can also be part of the risk if it is used for business travel.

Who needs plumber insurance?

Most plumbing professionals should have insurance, including:

- Self-employed plumbers

- Plumbing contractors

- Small plumbing companies

- Commercial plumbing businesses

- Apprentice plumbers working under a business

If you work in plumbing and get paid for it, insurance is worth serious consideration.

Do I Need Plumber Insurance?

Legal requirements

In some places, plumber insurance is required by law or by licensing rules. In other areas, it may not be legally required but is still strongly expected.

The rules can change by location, so it is smart to check local requirements before taking jobs.

Client and contractor requirements

Many customers want proof of insurance before they hire you. Bigger clients, builders, and contractors often require it too.

If you do not have insurance, you may lose jobs even if your work is excellent. Insurance can make your business look more professional and trustworthy.

Protection against costly claims

Accidents happen. A small leak can turn into water damage. A simple repair can lead to a claim if something goes wrong.

Insurance helps cover those unexpected costs so one mistake does not drain your business savings.

Peace of mind for business owners

When you know your business is protected, you can focus better on the job. That peace of mind is one of the biggest benefits of insurance.

Who Should Have Plumber Insurance?

Self-employed plumbers

Even if you work alone, you still face risk. A customer may claim damage, or your tools may get stolen from your van.

Plumbing contractors

Contractors often manage bigger jobs, which means bigger risks. Insurance can help protect you against claims arising from work you supervise or perform.

Small plumbing companies

If you have employees, vehicles, or several job sites, insurance becomes even more important.

Apprentice plumbers

Apprentices may work under a licensed business, but they still need protection through the company’s policy or their own coverage, depending on the arrangement.

Commercial plumbing businesses

Large plumbing companies usually need more coverage because they handle bigger contracts, more workers, and more expensive equipment.

Types of Plumber Insurance Coverage

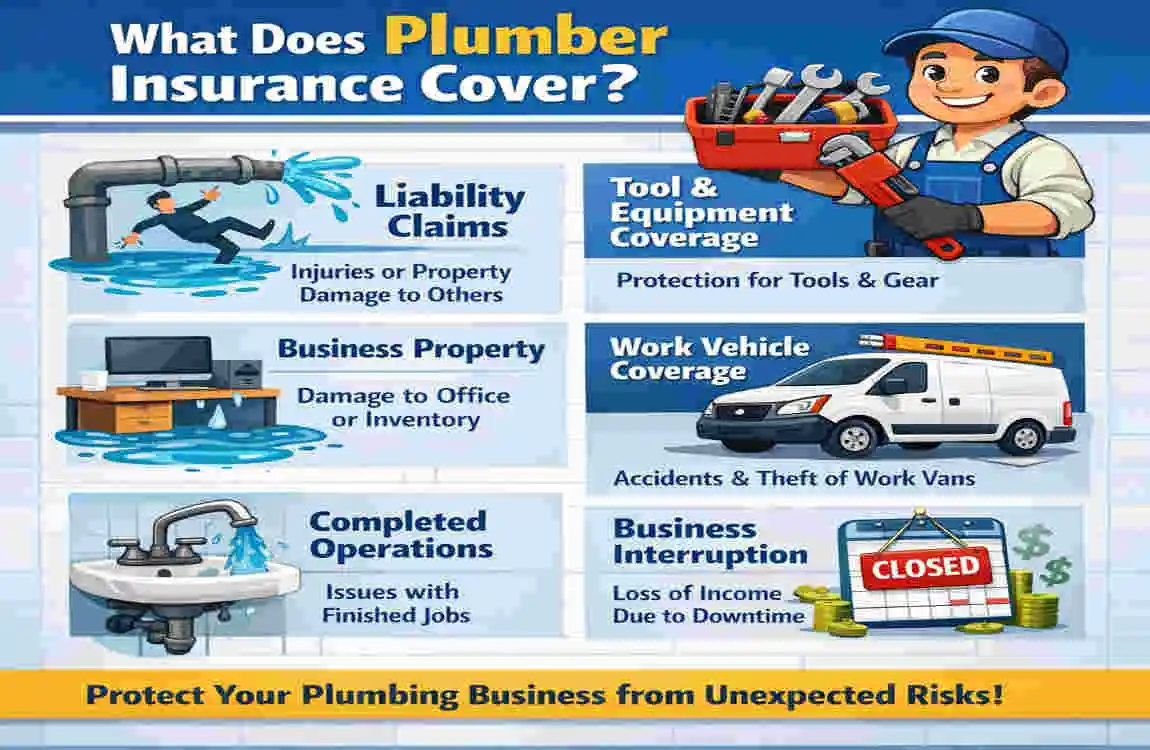

General liability insurance

This is one of the most important types of coverage. It helps pay for accidental property damage, bodily injury, and legal defense costs.

Professional liability insurance

This can help if a client says your advice, design, or work caused a problem.

Workers’ compensation insurance

If you have employees, this can help cover medical costs and lost wages after a work-related injury.

Commercial auto insurance

If you use a van, truck, or other vehicle for work, this type of coverage helps protect your business vehicles.

Tools and equipment insurance

Plumbing tools are expensive. This coverage can help replace stolen, damaged, or lost tools.

Property insurance

If you own an office, shop, or storage space, property insurance can help protect that location and its contents.

Business interruption insurance

If your business has to stop after a covered event, this can help replace some lost income.

Umbrella liability insurance

This adds extra protection on top of your main policies. It is useful for larger businesses or bigger contracts.

What Does Plumber Insurance Cover?

Table: What It Usually Covers and What It Usually Does Not

Covered Usually Not Covered

Property damage Intentional damage

Bodily injury Criminal acts

Legal defense costs Wear and tear

Stolen tools (if included) Personal vehicles without commercial coverage

Job-site accidents Contract disputes

Insurance policies vary, so always read the details. Do not assume every policy covers the same things.

Benefits of Having Plumber Insurance

Financial protection

A single claim can cost thousands of dollars. Insurance helps protect your money and keeps your business stable.

Builds customer trust

Customers feel more comfortable hiring an insured plumber. It shows that you take your work seriously.

Meets licensing requirements

Some licenses, permits, or contracts may require proof of insurance. Having coverage can help you stay compliant.

Protects business assets

Your tools, vehicle, and equipment are part of your business. Insurance helps protect those assets from loss or damage.

Helps win larger contracts

Many commercial clients only hire insured contractors. If you want bigger jobs, insurance can help you qualify.

How Much Does Plumber Insurance Cost?

Average annual costs

The cost of plumber insurance can vary a lot. Small businesses may pay less, while larger companies with more workers and higher risk may pay more.

Factors affecting premiums

Your price depends on several things:

- Business size

- Revenue

- Number of employees

- Coverage limits

- Claims history

- Location

A business with many employees and expensive equipment usually pays more than a one-person operation.

How to Choose the Right Plumber Insurance

Assess your risks

Start by thinking about what could go wrong in your business. Do you use a vehicle every day? Do you work on large commercial jobs? Do you have employees?

Compare multiple quotes

Do not buy the first policy you see. Get several quotes so you can compare coverage and price.

Review coverage limits

Make sure the policy limit is high enough for the kind of work you do. A cheap policy with low limits may leave you exposed.

Check deductibles

A deductible is the amount you pay before insurance helps. Higher deductibles can lower your premium, but they also raise your out-of-pocket cost.

Read policy exclusions

Every policy has limits. Some things are not covered, so read the fine print carefully.

Work with reputable insurers.

Choose a company that understands trades and small businesses. A good insurer can help you find the right fit.

Common Mistakes to Avoid

- Buying the cheapest policy

- Being underinsured

- Ignoring exclusions

- Forgetting tool coverage

- Not updating policies

- Skipping workers’ compensation

These mistakes can leave your business exposed when something goes wrong.

Tips to Lower Insurance Costs

Here are a few simple ways to keep costs under control:

- Bundle insurance policies

- Improve workplace safety

- Train employees well

- Increase deductibles if it makes sense

- Keep a clean claims record

- Compare quotes every year

A safer business often leads to better insurance pricing.

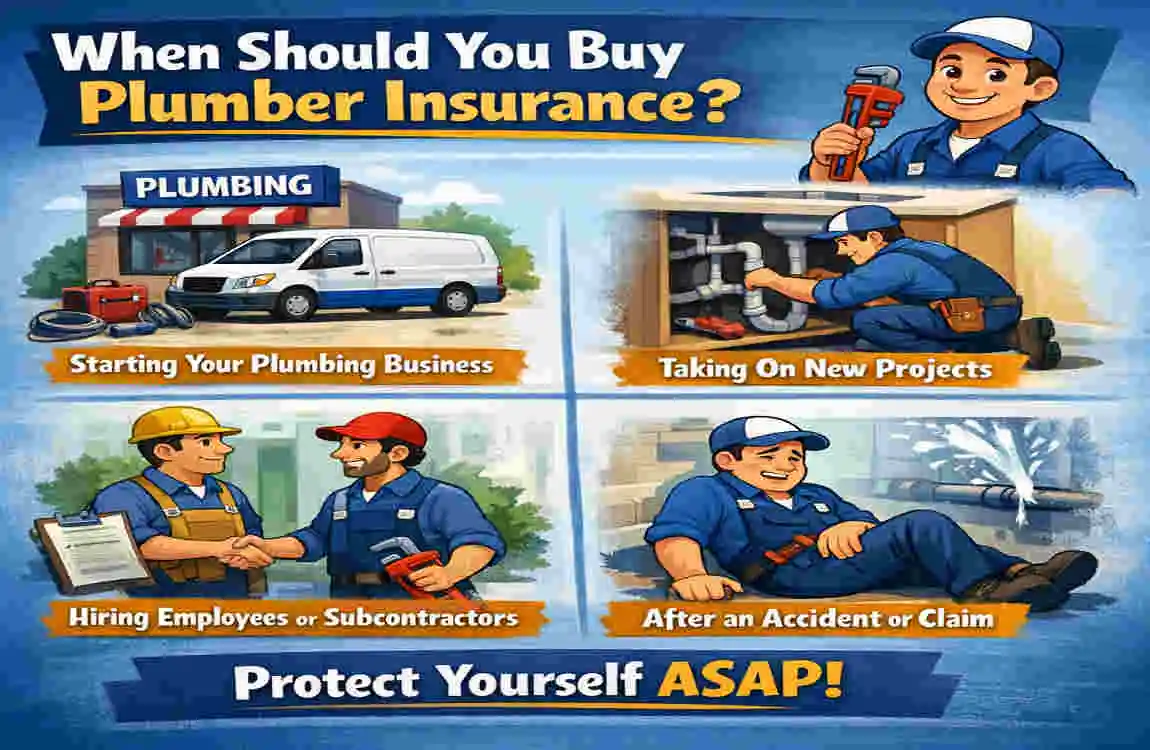

When Should You Buy Plumber Insurance?

Before starting your business

It is best to get coverage before you begin taking jobs. That way, you are protected from day one.

Before signing contracts

Many contracts require proof of insurance. Have your policy ready before you bid or sign.

Before hiring employees

If you bring on workers, your risks grow. Insurance becomes even more important.

Before purchasing expensive equipment

If you invest in tools, vehicles, or equipment, make sure they are protected.

Signs You Need More Coverage

You may need to increase your insurance if:

- Your business is growing

- You hire more staff

- You buy service vehicles

- You take on commercial projects

- You expand to multiple locations

As your business grows, your risk usually increases too.

Frequently Asked Questions

Do I need plumber insurance if I work alone?

Yes. Even solo plumbers can face property damage, injuries, or legal claims.

Is plumber insurance legally required?

It depends on your location and type of work. Some clients and licensing bodies require it.

How much does plumber insurance cost?

The cost depends on your business size, location, employees, coverage limits, and claims history.

Does plumber insurance cover damaged customer property?

General liability insurance usually covers accidental property damage.

Does plumber insurance cover stolen tools?

Yes, if your policy includes tools and equipment coverage.

Can I get plumber insurance as a self-employed contractor?

Yes. Many insurers offer plans for independent plumbers.

What is the most important insurance for plumbers?

General liability insurance is usually the most essential, but many businesses also need commercial auto and workers’ compensation.

Can plumber insurance help win more jobs?

Yes. Many clients prefer insured plumbers, and some require it before awarding work.

| Topic | Information |

|---|---|

| What Is Plumber Insurance? | A type of business insurance that protects plumbers from financial losses caused by accidents, property damage, injuries, and legal claims. |

| Who Needs It? | Self-employed plumbers, plumbing contractors, apprentices with their own business, and plumbing companies. |

| Why Is It Important? | It helps cover unexpected costs, protects your business assets, and meets many client or licensing requirements. |

| Common Coverage | General liability, professional liability, workers’ compensation, commercial auto, tools and equipment, and property insurance. |

| Benefits | Reduces financial risk, builds customer trust, covers legal expenses, and protects expensive plumbing equipment. |

| Is It Required by Law? | Requirements vary by state or country. Workers’ compensation and commercial auto insurance are often legally required in certain situations. |

| Average Cost | Typically ranges from $40–$150 per month, depending on your business size, location, and coverage limits. |

| Factors Affecting Cost | Number of employees, annual revenue, claim history, services offered, and coverage amount. |

| When You May Not Need It | Hobbyists or employees covered under an employer’s insurance may not need their own policy, though additional coverage can still be beneficial. |

| Bottom Line | If you run or own a plumbing business, plumber insurance is a smart investment that protects your finances and reputation from unexpected risks. |